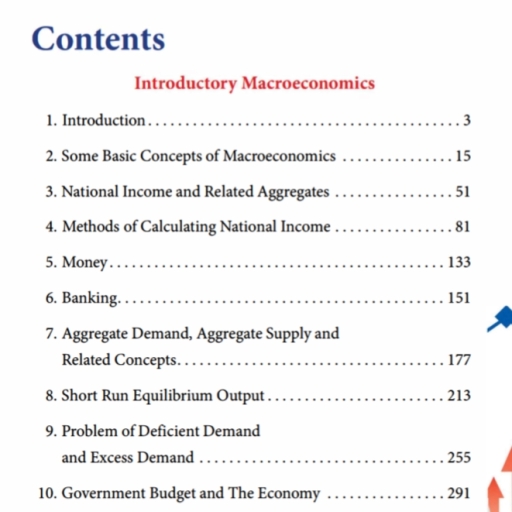

Page 1 :

PART-1, SECTION -A, Instructions: From question number 1 to 18, attempt any, 15 questions., , , , +, Ravi and Vimal are partners in a firm sharing profits in the ratio of 3:2. An, extract of their Balance Sheet is as follows:, , , , , , , , , , , , If half of the investments are taken over by Ravi and Vimal in their profit, sharing Ratio at book value, what amount of investment will be shown in the, revised Balance Sheet?, , (A) 275,000, (B) 235,000, (C) %95,000, (D) %20,000, , , , Reserve Capital is not a part of:, , (A) Authorised Capital, (B) Subscribed Capital, (C) Unsubscribed Capital, (D) Issued Share Capital, , , , Viral Ltd. forfeited a share of %50 issued at a premium of 20% for, non-payment of first call of 215 per share and final call of 25 per share. At, what minimum price it can be reissued:, , (A) %50, (B) %30, (C) %40, (D) 220, , , , , , +, , , , The Directors of Vina Ltd. forfeited 70,000 Equity Shares of 210 each, 210, called up, for non-payment of final call of 21 per share. Half of the forfeited, shares were reissued at 220 per share fully paid up. On reissue of forfeited, shares, the following amount will be transferred to the Capital Reserve, Account:, , (A) ®70,000, , (B) 21,40,000, , (C) %6,30,000, , (D) 23,15,000

Page 2 :

A Company invited applications for 1,00,000 shares and it received, applications for 1,50,000 shares. Applications for 30,000 shares were, rejected and the remaining shares were allotted on prorata basis., How many shares an applicant for 3,000 shares will be allotted:, , (A) 2,500 Shares, (B) 3,600 Shares, (C) 4,500 Shares, (D) 2,000 Shares, , , , Farha, Siya and Abhi share profits equally. They decide that in future Abhi, will get 1/5th share in profits. On the day of change Firm's goodwill is, valued at 730,000. What will be the effect of this change:, , (A) Abhi's loss %5,000; Gain of Siya and Farha %10,000 each., (B) Farha's gain 210,000; Loss of Siya and Abhi %5,000 each., (C) Abhi's loss %4,000; Gain of Farha and Siya ®2,000 each., (D) Farha’s gain 24,000; Loss of Siya and Abhi 22,000 each., , , , Veer is the manager in a partnership firm and is entitled to receive a salary, of 8,000 per month and a commission of 5% on Net Profit after charging, such commission. Profit for the year is €13,56,000 before charging salary and, commission, The commission of Veer is:, , (A) %67,800, (B) 264,571, (C) 263,000, (0) %60,000, , , , On admission of a partner, which of the following items the Balance Sheet is, transferred to the credit of Capital Accounts of old partners in the old profit, sharing ratio, if Capital Accounts are maintained following Fluctuating, Capital Accounts Method:, , (A) Deferred Revenue Expenditure, , (B) Profit and Loss Account (Debit Balance), (C) Profit and Loss Account (Credit Balance), (D) Balance in Drawings Account of Partners, , , , , , , , Pick the odd one out with respect to Fixed Capital Account:, , (A) Capital Introduced, (B) Interest on Capital, (C) Capital withdrawn, (D) None of these

Page 3 :

10., , r, , In case of Admission of a Partner, the entry for Unrecorded Investments is:, , (A) Debit Partners’ Capital A/cs and Credit Investments A/c., (B) Debit Revaluation A/c and Credit Investments A/c., , (C) Debit Investments A/c and Credit Revaluation A/c., , (D) None of the above., , , , 11,, , 12., , Which one of the following is NOT an essential feature of a partnership:, , (A) There must be an agreement, (B) There must be a business, , (C) The business must be carried on for profits, (D) The business must be carried on by all the partners., , Amount of old goodwill already appearing in the books will be written off:, , +, , (A) in old ratio, , (B) in new ratio, , (C) in sacrificing ratio, (D) in gaining ratio, , , , 13., , Capital employed in a business is ®2,00,000. The normal rate of return on, Capital employed is 15%. During 2021, the firm eared a profit of 248,000., The company calculates goodwill on basis of 3 year's purchase of super, profit. On the basis of information, match the following:, , , , , , , , , , , , Column | Column Il, a. Normal Profits (i) 54,000, b. Actual Profits (ii) 18,000, c. Super Profits (iti) 48,000, d. Goodwill tiv) 30,000, , , , (A) (a)—(i), (b)— (iti), (c)—fiv), (d)—{ii), (B) (a)—(i), (b)—(1), (c)—(ii), (d)—fiv), (C) (a)—(iv), (b)—(itt), (c)—-11), (d)—(1), (D) (a)—(iv), (b)—(iii), (c)—(i), (d)—ii), , , , , , 14,, , When a company has not called up the total nominal (face) value of the, share, it is known as:, , (A) Issued Capital, , (8) Unissued Capital, , (C) Subscribed and Fully paid up, , (D) Subscribed but not fully paid up