Page 1 :

Ranker’s Academy, (A Leading Institute of Accountancy, Business Studies and Economics for XI & XII), Chapter – 11, , ACCOUNTS FROM INCOMPLETE RECORDS, Meaning – An accounting system which is not based on double entry is known as incomplete, records. Under this system personal accounts and cash account are only maintained. All, other impersonal accounts are avoided. So information relating to assets, liabilities, expenses, and revenues are incomplete. Many people describe it as single entry system. However,, single entry system is a misnomer (wrong usage) because there is no such a system of, maintaining accounting records., There is a misconception that under this system only one aspect of each transaction is, recorded, but it may be stated that both aspects are recorded in some transactions and in, other cases, only one aspect is recorded while some other transactions are not recorded at all., It is a mixture of double entry, one entry and no entry. In short, this system is incomplete,, inaccurate, unscientific and unsystematic style of accounting., Features of Incomplete Records, a. Unsystematic method of recording transactions., b. Generally records cash transactions and personal accounts are properly maintained,, but there is no information regarding revenue / gains and expenses / losses, assets and, liabilities., c. Personal transactions of owners may also be recorded in the cash book., d. Lack of uniformity, because different organizations are maintaining records according to, their needs., e. Very difficult to ascertain profit or loss., f. Less accuracy for accounting information., Why traders prefer Incomplete Records (Reasons for incompleteness), 1. It is suitable to small concerns which have mainly cash transactions and do not have, many assets and liabilities to be recorded in detail., 2. This system is economical since lesser number of books is maintained., 3. Lack of knowledge about double entry system., 4. Ignorance of businessman to the statutory requirements of keeping proper books of, accounts., 5. Intentional omission to take advantage of taxation., Limitations of Incomplete records, 1. Arithmetical accuracy cannot be ensured., 2. In the absence of nominal accounts, it is difficult to determine the exact profit or loss., 3. As real accounts are not maintained, the value of assets and liabilities stated in the, Balance Sheet is not reliable., 4. It increases the chances of errors and fraud., 5. It will not be accepted by the authorities like tax department, banks etc., , Add. 14-A, Anupam Nagar, Govindpuri-Gwl., , Accounting-11, , Chapter 11, , Page 1

Page 2 :

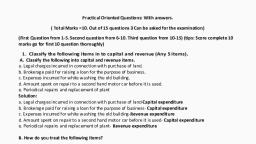

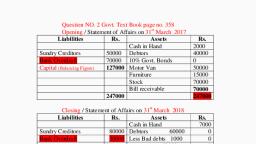

Ranker’s Academy, (A Leading Institute of Accountancy, Business Studies and Economics for XI & XII), Ascertainment of profit or loss – Even though the records are incomplete, the trader has to, ascertain the result of the business to assess its efficiency and he is also interested in, determining the financial position of the entity at the end of the year. Two methods are used, for this purpose:, 1. Ascertainment of profit or loss by preparing the Statement of Affairs – Under this, method, profit or loss can be ascertained by comparing the capital at the beginning and, at the end. For this purpose two statements are prepared., a. Statement of Affairs – It is a statement prepared by presenting the assets on one side, and liabilities on the other side as in the case of Balance Sheet. The differences, between the totals of the two sides represent owner’s equity or capital., i.e. Capital = Assets – Liabilities. Though it resembles (similar) to a balance sheet, it, differs on the ground that balances of various assets and liabilities are not derived from, ledger accounts and it is prepared to find out the owners equity but not to disclose the, financial position of the business., b. Statement of profit or loss – The statement prepared to ascertain the profit or loss, by comparing the opening capital with closing capital is called statement of profit or, loss. The following steps are to be taken to ascertain the profit or loss:, Format of a Statement of profit or loss, Particulars, Capital at the end of the year, Add: Drawings during the year, , Amount, xxx, xxx, xxx, xx, xxx, xxx, xxx, , Less: Additional Capital Invested, Less: Capital at the beginning, Profit or loss during the year, , Differences between statement of affairs and balance sheet Basis, Reliability, Objective, Omission, , Statement of affairs, It is less reliable as it is prepared, from incomplete records., To estimate the balance in capital, account., Omission of assets or liabilities, cannot be discovered easily., , Balance sheet, It is more reliable as it is prepared from, double entry records., To show the true financial position., Omission if any can be traced out easily, from accounting records., , 2. Preparation of Profit and Loss account and Balance Sheet under Conversion, Method To prepare trading and profit and loss account and the balance sheet, we need complete, information regarding expenses, incomes, assets and liabilities. In case of incomplete records,, details of some items like creditors, cash purchases, debtors, cash sales, other cash payments, and such receipts are easily available, but there are a number of items that are missing and, have to be worked out from various sources. They are as follows:, Add. 14-A, Anupam Nagar, Govindpuri-Gwl., , Accounting-11, , Chapter 11, , Page 2

Page 3 :

Ranker’s Academy, (A Leading Institute of Accountancy, Business Studies and Economics for XI & XII), 1. Opening Capital - It can be ascertained from the statement of affairs at the beginning, of the year., 2. Credit purchases – It is calculated by preparing the total creditors account. (See the, format in text book)., 3. Credit sales – It can be traced out with the help of a total debtors account. (See the, format in text book)., 4. Bills receivable – by preparing total bills receivable account. (See the format in text, book)., 5. Bills payable – by preparing total bills payable account. (See the format in text book)., 6. Other missing information through summary of cash – In case the amount paid to, creditors or the amount received from debtors or the opening or closing cash or bank, balance may be missing, we may prepare a cash book summary showing all receipts, and payments during the year and balancing figure is taken as the amount of missing, item., After the missing figures have been traced out, the final accounts may be prepared, straight away or after the preparation of trial balance., ******************, , Add. 14-A, Anupam Nagar, Govindpuri-Gwl., , Accounting-11, , Chapter 11, , Page 3