Page 1 :

CBSE Quick Revision Notes and Chapter Summary, Class-12 Accountancy, Part – B – Financial Statement Analysis, , Introduction, Financial Statements are helpful to know the financial position of the business. A financial, statement is an organized collection of data according to logical and consistent accounting, procedure. Financial statements, essentially, are interim reports, presented annually and, reflect a division of the life of an enterprise into more or less arbitrary accounting period –, frequently a year., MEANING OF FINANCIAL STATEMENTS, Financial statements are mainly prepared for decision making purposes. Financial Statements, are the end product of financial accounting. Financial Statements are prepared to know the, profitability and financial position of the business. Financial Statements provide detailed, information and are thus a form of analysis. Financial Statements are also known as Financial, Reports., Some Important definitions of Financial Statements:, 1., , In the words of John N. Myer, “ The Financial Statements provide a Summary of the, accounts of a business enterprise,”, , 2., , “ Financial Statements are prepared for the purpose of presenting a periodical review or, report on progress made by the management and deal with the status of investment in, the business and the results achieved during the period under review.”, ----- American Institute of Certified Public Accountant (AICPA), “At every annual general meeting of the company, the Board of directors shall lay before, the company (a) Balance Sheet as at the end of the period (b) Statement ofvProfit and, Loss for period; in case of a company not carrying on business for profit, an Income and, expenditure account shall be laid before the company at its Annual General Meeting, instead of Profit and Loss Account.”, ----- Under Section – 211 of Indian Companies Act 1956, , 3., , OBJECTIVES OF FINANCIAL STATEMENTS, 1. To provide the True and fair picture of the business., 2. To provide the financial information of the business., 3. To provide useful information’s for making economic decisions.

Page 2 :

4. To provide useful information to investors and creditors., 5. To provide the useful information’s to the users for predicting, comparing, and evaluating, enterprise earning power., Balance sheet, Balance sheet is a statement of assets and liabilities and a part of financial statements, which, is prepared to find out the financial position of his business as on a particular date. This, statement is prepared from the trial balance after the trading and Statement of profit and loss, are prepared. All the nominal account get closed through the trading and Statement of profit, and loss, but this statement (balance sheet) contains the balances of only those ledgers, which remain open and carried forward, whether they are personal accounts or real, accounts. These accounts which are carried forward to the next year are either assets or, liabilities. On the right hand side of statement are shown assets (which will be given on the, debit side of trial balance) and on the left hand side liabilities (which have credit balance), The profit as ascertained from the Statement of profit and loss is added to the capital account, on the liability side and if there is net loss from profit and loss account this will be deducted, from the capital account., “ Balance sheet is a list of assets and liabilities accounts. This list depicts the position of assets, and liabilities of a specific business at a specific point of time.”, ---- American Institute of Certified Public Accountants (AICPA), , Users of Financial Statements, Internal Users, (1) Proprietors: The proprietors or owners of the business need to know the Profit or Loss, of the business and Financial Position of the business. Because the Capital is contributed, by the owners and they take risk of this capital. Financial Statements helps the owners to, estimate the trading results of the business, its financial position towards the end of the, accounting period and future prospects of the business., (2) Management : Management requires Financial Statements for planning and controlling, purposes. By proper use of the Financial Statements, management can help to improve, efficiency and thereby increase profits of the enterprise., (3) Employees : Accounting information provided by the Financial Statements help to, maintain cordial relations between employees and employers. Moreover good results of, the business activities as revealed by financial records provide a great satisfaction to, employees as their bread and butter depends on these results. In those business concerns, in which profit sharing schemes are introduced, employees become very much interested, in knowing how the profit has been ascertained.

Page 3 :

External Users, (1) Creditors: The persons to whom business owes money are the creditors of the business., Since they have advanced some money or money’s worth to the business, their fate is, tagged to the prosperity or the concern. Sound financial position of the business will win, their faith for further credit and this they can know from accounting information., (2) Potential investors : It is only after getting a detailed information about the profitability, of the concern that investors take decisions regarding investment to be made in that, particular business. Accounting information is of great use to them in this connection., (3) Consumers : Since price of a product is fixed after considering cost of production plus, some reasonable margin of profit. Consumers are always interested in accounting, information to have an idea of the price of a product and the profit margin. If exorbitant, prices are charged to increase profit margin, consumer may compel that business to, reduce its profit margin., (4) Government : Financial Statements are required by the government for fixing sales tax,, assessing the profitability of the concern computing national income and determining the, growth rate of industry., (5) Researchers : Financial Statements of various enterprises is of great use to research, scholars to complete their research work., (6) Competitors : Those persons who want to compete with a particular business are, interested to know its profitability. This is made available from accounting records of the, concern., (7) Taxation Authorities : Taxation authorities also need accounting information for tax, purposes., (8) Stock Exchanges : Stock exchanges also require Financial Statements for listing of, securities and other matter connected with stock dealings., (9) Trade Associations : Various trade associations like chambers of commerce use the, Financial Statements to determine the working results of their member units so that if, need be, they may negotiate with the govt. for various concessions., (10) Newspapers: Various dailies or weekly magazines especially related to, economic matters need Financial Statements of various business units for bringing them, to the knowledge of general public., Limitations of Financial Statements, (a), No record of important non–monetary information: Financial Statements, takes into consideration only monetary transactions. A transaction, however important,, will not be shown in the Financial Statements, if it cannot be expressed in the monetary, terms. For example; the extent of competition faced by the business is an important, matter in which the management is highly interested, but accounting is not tailored to, consider such events. Hence greatest limitation of Financial Statements is the, consideration of only monetary transactions.

Page 4 :

(b), Window Dressing:, Sometimes Financial Statements prepared by the, accountants is not true and faithful or may be manipulated by the accountants. When, accounts are manipulated and present the Financial Statements to show the better, position of the business than the actual position, it is known as window dressing. In such, a situation results provided by the Financial Statements are not true and fair and does, not show the actual financial position of the business., (c) No consideration of price level changes: The most serious limitation of Financial, Statements is adoption of historic cost concept for recording various assets irrespective, of subsequent change in their prices., (d), Lack of uniformity in recording methods: Though some generally accepted, accounting principles are followed for recording purposes still more than one principle, is used for treating the same item. For example; some concerns value their stock on LIFO, (last in first out) method while others follow FIFO (first in first out) method. The uses of, different accounting methods render the financial statements incomparable., (e), Subjective approach: Financial Statements of a business unit are framed by the, accountant according to his own personal judgment and ability. Hence the Financial, Statements based on personal judgment make the records only ‘approximations’ and not, ‘authoritative’., (f), Conservative approach: Due to application of concept of ‘conservation’ all, losses are provided for but no provision is made in the books for prospective profits., Hence conservative approach is another limitation of Financial Statements., (g), ‘Post–mortem’ analysis of past records: Financial Statements provide, information at the end of the accounting period in the form of annual accounts. Financial, Statements at the best is only of historical nature and cannot be used to take corrective, action. The business requires timely information at frequent intervals to help, management to make plans and take corrective measures. But the Financial Statements, is not supposed to supply such information at shorter intervals than one year., Balance Sheet as per the Revised Schedule VI, The main purpose of Revised Schedule –VI is to maintain the transparency in financial, statements., Only two parts- Part I(Balance Sheet) and Part II (Statement of Profit and Loss) Part III, (Interpretation) and Part IV (Balance sheet Abstract of company’s general business profile), omitted., Net working capital will not be appearing on Balance sheet.

Page 5 :

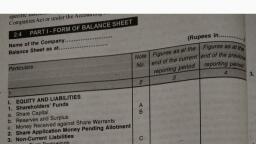

Fixed assets should be categorized as (a) Fixed Tangible Assets (b) Fixed Intangible Assets., Long term borrowings to be shown under non-current liabilities and short term, borrowings to be shown under current liabilities., Current maturities of long term debt to be disclosed under other current liabilities., Proforma of Balance Sheet, Name of the Company …………………………………….., Balance Sheet as at…………………………………….., (in Rs.………..), Note, No., , Particulars, , A. EQUITY AND LIABILITIES, (1) Shareholders’ Funds, (a) Share capital, (b) Reserves and surplus, (c) Money received against share Warrants, (2) Share application money pending, Allotment, (3) Non – current liabilities, (a) Long term borrowings, (b) Deferred tax liabilities (net), (c) Other long term liabilities, (d) Long term provisions, (4) Current liabilities, (a) Short term borrowings, (b) Trade payables, (c) Other current liabilities, (d) Short term provisions, Total, , Figures as, at, the end of, current, reporting, period, , Figures as, at, the end of, previous, reporting, period

Page 6 :

B. Assets, 1) Non-Current Assets, (a) Fixed assets, (i) Tangible assets, (ii) Intangible assets, (iii) Capital work in progress, (iv) Intangible assets under, development, (b) Non-current investments, (c) Deferred tax assets (net), (d) Long term loans and advances, (e) Other non-current assets, (2) Current Assets, (a) Current investments, (b) Inventories, (c) Trade receivables, (d) Cash and cash equivalents, (e) Short term loans and advances, (f) Other current assets, Total, Hence we see that there are only four major headings under equity and liability side whereas, Asset side consist of only two majour heading, Subheading under various major heading, Equity and Liability, (1) Shareholder's Fund, (a) Share Capital, (b) Reserves and Surplus, (c) Money received against share warrants, (2) Non Current Liabilities, (a) Long term borrowings - Bonds, Debenture, loans from Banks etc are included., (b) Deferred tax liabilities., (c) Other long term liabilities - It include trade payable which outstanding for more than 12, months.

Page 7 :

(3) Current Liabilities, (a) Short term borrowings, (b) Trade Payables (Creditors and Bils Payable), (c) Other Current Liabilities - Include current maturities of long-term debt., Interest, accrued but not due & interest acerued and due on borrowings, outstanding expenses, calls, in advance, unclaimed dividends etc., ASSETS, (1) Non Current Assets, (a) Fixed Assets :- This subheading is divided into tangible, Intangible Assets and, Capital- work-in-progress., (b) Non-Current Investments., (c) Deferred Tax Assets, (d) Long term Loans and Advances, (e) Other Non-Current Assets, (2) Current Assets, (a) Current Investment (i.e. upto one year), (b) Inventories - Raw material, stock in trade work in progress, stores and, spares and loose tools etc. are also included alongwith the finished goods, (c) Trade Receivables - Sundry Debtors, Bills Receivable, (d) Cash and Cash Equivalents, (e) Short term loan and advances, (f) Other current Assets - It include prepaid expenses, interest ocerued on investments etc., Note1. Miscelaneous Expenditure and the Negative Balance of Statement of Profit & Loss are, not shown separately., 2. Statement of Profit & Loss - Negative Balance is shown as a minus item under Reserve and, Surplus.

Page 8 :

3. Miscelaneous Expenditure items are Deducted from the Reserves and Surplus and liability, heading and in the absence of such a reserve these are shown as a other Non- Current Assets or, other current Assets as per instructions., Contingent Liabilities :- These are the liabilities which are not liabilities on the date but may, arise upon the happening, of a certain event. These are not added in the Amount of liabilities and are shown only, as footnotes. Remember some examples :- Disputed claims not as knowledge as debts on that date, - Uncaled liability on partly paid shares, - Arrears of dividends on cumulative preference shares., - Bils discounted but not matured, - Guarantee for loans, I. ITEMS APPEARING UNDER THE HEAD EQUITY AND LIABILITIES IN THE BALANCE SHEET, (1) Shareholders Funds, (a) Share Capital: Under the head, ‘Share Capital’, some of the important items to be shown are as, under :, (i), , Number and amount of shares authorized., , (ii), , Number of shares issued. Subscribed and fully paid up and subscribed but not fully, paid up., , (iii), (iv), , Par value per share., A reconciliation of the number of shares outstanding at the beginning and at the end of, the reporting period., , (v), , Shares in the company held by each share holder holding more than 5% shares, specifying the number of shares held., , (vi), , Aggregate number and class of shares allotted as fully paid up for consideration other, than cash., , (vii) Aggregate number and class of shares allotted as fully paid up by way of bonus shares, (viii) Calls unpaid (showing aggregate value of calls unpaid by directors and officers.), (ix), , Forfeited shares (amount originally paid up)., , (b) Reserve and Surplus: Under this head the following items are shown:

Page 9 :

(i) Capital Reserves ;, (ii) Capital Redemption Reserve;, (iii) Securities Premium Reserve;, (iv) Debenture Redemption Reserve;, (v) Revaluation Reserve (Accounting Treatment not to be Evaluated);, (vi) Share options Outstanding Account (Accounting Treatment not to be evaluated);, (vii) Others reserve (restricted to General Reserve only);, (viii) Surplus i.e. balance in Statement of Profit & Loss., (c) Money received against share warrants (Accounting Treatment not to be evaluated):, A share warrant is a financial instrument which gives holder the right to acquire equity shares., A disclosure of the money received against share warrants is to be made since shares are yet to, be allotted against the share warrants. These are not shown as part of share capital but to be, shown as a separate line items., (2) Share application money pending allotment (Accounting Treatment not to be, evaluated): If company has issued shares but date of allotment falls after the balance sheet date,, such application money pending allotment will be shown in the following manner:, (i) Share application money not exceeding the issued capital and to extent not refundable is to, be disclosed under this line-item., (ii) Share application money to the extent refundable or where minimum subscription is not, met, such amount shall be shown separately under ‘Other Current liabilities’, (3) Non-current liabilities: A non-current Liability is a liability which is not classified as currentliability. A liability is classified as current when it satisfies any one of the following conditions:, (i), , It is expected to be settled in the company’s normal operating cycle. Operating cycle, means the time between the acquisition of assets for processing and their realization in, cash or cash equivalents. It may vary from few days to few years. Where the operating, cycle cannot be identified, it is assumed to have a duration of 12 months., , (ii) It is held for the purpose of being traded., (iii) It is due to be settled within 12 months after the reporting date., (iv) The company does not have an unconditional right to defer settlement of the liability, for at least 12 months after the reporting date., Hence, the liabilities which are not classified as current shall be classified as ‘Non-current’.

Page 10 :

(a) Long Term borrowing (Debentures / Bonds, Long Term Loans etc.), (b) Deferred Tax Liabilities (Net)., (c) Other Long Term Liabilities, 1. Non-Current Assets:, (a) Fixed Assets: Assets which are required for purpose of reuse in the business but not for, purpose of resale., (i) Tangible Assets: Tangible assets are assets which can be physically seen and touched. (Land,, Building, Plant and Equipment, Furniture & Fixture, Vehicles, Office Equipments, Others)., (ii) Intangible Assets: Intangible Assets are those which are not tangible., (a) Goodwill, (b) Brand / Trademarks, (c) Computer Software & Mining rights, (d) Masthead and Publishing titles., (e) Copyrights, and patents and other intellectual property rights, services and, operating rights., (f) Recipes, formulae, models, designs and prototypes, (g) Licenses and franchise, (iii) Capital work in Progress., (iv) Intangible Assets under Development – like patents, intellectual property rights, etc. which are, being developed by the company., (b) Non-Current Investments: Non-current Investments are investments which are held not, with the purpose to resell but to retain them. Non-current Investments are further classified into ‘, Trade Investments’ and ‘ Other Investments’., Trade Investments are investments made by a company in share or debentures of another, company, not being its subsidiary, to promote its own trade and business. Other Investments are, those investments which are not trade investments., (c) Deferred Tax Assets (Net)., (d) Long-term Loans and Advances – only Capital Advances and Security Deposits., (e) Other non-current assets., 2. Current Assets, (a) Current Investments – Investment which are held to be converted into cash within a short, period i.e., within 12 months (Investments in Equity Instrument, Preference shares, Government, Securities, Debentures, Mutual Funds etc.), (b) Inventories : Inventories include the following:, (i) Raw Material, (ii) Work-in-progress, (iii) Finished Goods, (iv) Goods acquired for trading, (v) Stores and Spares

Page 11 :

(vi) Loose tools., (c) Trade Receivables: Trade receivables refer to the amount due on account of goods sold or, services rendered in the normal course of business. It includes both Debtors and Bills receivables., (d) Cash and cash equivalents – as discussed in the salient features of Schedule-VI in General, Instructions., (e) Short-term Loans and Advances, (f) Other Current Assets (Restricted to Prepaid expenses, accrued incomes and advance tax, only), Preparation of Statement of Profit and Loss or Income Statement as per Revised Schedule, VI, As per the Revised Schedule VI of the Companies Act, 1956 Statement of Profit and Loss or income, statement is to be prepared according to the new guidelines., Proforma of Statement of Profit & Loss or Income Statement, Particulars, Note, No., I. Revenue from operations, II. Other Income, III. Total Revenue (I + II), IV. Expenses, Cost of Material Consumed, Purchases of Stock-in-Trade, Changes in Inventories of finished, goods,, Work-in-progress and Stock-in-Trade, Employee benefits expense, Finance Costs, Depreciation and Amortisation, expenses, Other expenses, Total expenses, V. Profit before exceptional and extraordinary, items and tax (III –IV), VI. Exceptional items, VII. Profit before extraordinary items and tax, (V –VI), VIII. Extraordinary items, IX. Profit Before Tax (VII – VIII), X. Tax Expense:, (1) Current Tax, (2) Deferred Tax, , Figures for, the current, reporting, period, xxxx, xxxx, xxxx, , Figures for the, previous, reporting, period, xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, xxxx, xxxx, , xxxx, , xxxx, , xxxx, xxxx, , xxxx, xxxx, , xxxx, xxxx, , xxxx, xxxx, , xxxx, xxxx, , xxxx, xxxx

Page 12 :

XI. Profit (Loss) for the period from continuing, operations (VII –VIII), XII. Profit (Loss) from discounting operations, XIII. Tax expense of discontinuing operations, XIV. Profit (Loss) from discounting operations, (after Tax) (XII –XIII), XV. Profit (Loss) for the period (XI – XIV), XVI. Earnings per Equity Share :, (i) Basic, (ii) Diluted, , xxxx, , xxxx, , xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, , xxxx, , xxxx, , xxxx, xxxx, , xxxx, xxxx, , Tool of Financial Analysis, Comparative Statement :- Financial Statement of two years is compared. Absolute change, and then the percentage change in figure are calculated. It is a form of Horizontal Analysis., Common Size Statement : Various figure of single year financial Statement are converted in to, percentage with resepect to some common base. In Income Statement sales in take as base, (i.e.100) where as in Balance Shettotal assets are taken as base., Trend Analysis :- Here trend percentage are calculted for a number of years taking one year, as a base year. This helps is assessing the trend of increase or decrease in various items., Accounting Ratios :- Study of relationship between various items is known as Ratio analysis., Cash Flow Statement :- It shows the inflow and outflow of cash and cash equivalents during, a particular period which helps in finding out the causes of changes in cash between the two, dates., Fund Flow Statement :- It indicates the reasons of changing in working capital during a, particular time period. It shows sources (inflow) and Applications (Outflow) of funds., Break - even Analysis :- It is a point where total of sales is exactly equal to the total of cost to, the total of cost of sales i.e. the firm has neither any profit nor any loss. It is also known as no, profit no loss point., Comparative Balance Sheet, Comparative Balance Sheet is prepared to show financial differences between several accounting, periods. The main purpose of Comparative Balance Sheet is to compare the assets, liabilities and, capital and to show the increase and decrease in these items., According to Prof. Foulkey, “Comparative Balance Sheet analysis is the study of the trend of the, same items, group of items and computed items in two or more balance sheets of the same, business enterprise on different dates.”

Page 13 :

Steps Involved, Step 1. All Assets and Liabilities are shown in the first Column (Particulars Column), Step 2. All Assets and Liabilities of previous year’s are shown in the second column, Step 3. All Assets and Liabilities of Current year’s are shown in the third column, Step 4. Previous year’s Assets and Liabilities are compared with the current year’s Assets and, liabilities, to know the absolute change (increase of decrease), Step 5. Percentage Change is calculated by using the following formula:, Percentage Change = Absolute Change, x 100, Previous year’s Figure, , Proforma of Comparative Balance Sheet, , Particulars, , I. EQUITY AND, LIABILITIES, , Note, No., , Current, Year, (Rs.), , Previous Absolute Change, % Change, Year, (increase/decrease) (%, (Rs.), increase, OR %, decrease)

Page 16 :

- To compare the firm performance with the performance of other firm in the same business, Steps involved in preparation of Comparative Income Statement, Step 1. Record ‘Revenue from Operation’ i.e. Net Sales, Revenue from Services etc., Step 2. Record ‘Other Incomes’ i.e. Dividend Received, Rent Received & Interest etc., Step 3. Record Expenses i.e. Cost of material purchased, Purchases of Stock in trade, Change in, inventories, Employees benefit expenses, Depreciation and Amortization, and other expenses etc., Step 4. Find out the profit before tax (Revenue from operation + other incomes – Expenses), Step 5. Deduct Income Tax from Profit before tax to find out the ‘Profit After Tax’., Step 6. Find out Absolute Change (Increase or decrease), Step 7. Find out Percentage Change by using the following formula:, Percentage Change = Absolute Change, Previous year’s Figure, , x 100, , Proforma of Comparative Income Statement, , Comparative Income Statement, Particulars, , Note, No., , Current, Year’s, Figures, , Previous, Year’s, Figures, , Absolute, %, Change, Change, , I. Revenue from Operations, , xxxx, , xxxx, , xxxx, , xxxx, , II. Other Income, , xxxx, , xxxx, , xxxx, , xxxx, , III. Total Revenue (I + II), , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, , xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, xxxx, , IV. Expenses :, Cost of Material Consumed, Purchase of Stock-in-Trade, Changes in Inventories of, Finished Goods, Work-in-Progress and Stock-inTrade, Employee Benefits Expenses

Page 17 :

Finance Costs, Depreciation and Amortisation, Expenses, Other Expenses, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , Total Expenses, V. Profit Before Tax (III – IV), Less : Income Tax, VI. Profit After Tax, xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , xxxx, , Common Size Statement Preparation, STEPS, 1. Put the absolute amounts of two years side by side. Previous year's amount in the, first column and current year in the 2nd column., 2. Calculate the percentage of each items w.r.t the common base by using the, formula Percentage of the item =, Absolute figure of the item of the year x 100/Base figure of that year, 3. Base figure for the Income statement is taken as total sales whereas for Balance Sheet it is, total assets., 4. 3rd column is for Previous, year's percentage., , year's Percentage and 4th column is for current, , Importance of Common Size Statements, - Provides common base for comparison irrespective of the size of individual item., - It presents the change in various items in relation is net sales, total assets or total liabilities., - It establish the trend in various items of financial statements., Proforma of Common Size Statements