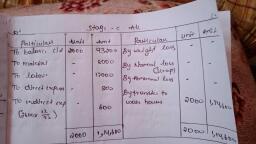

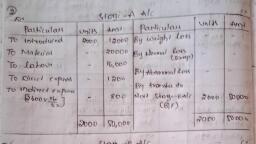

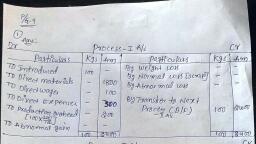

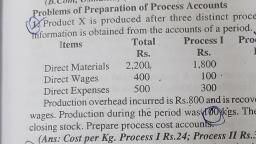

Page 1 :

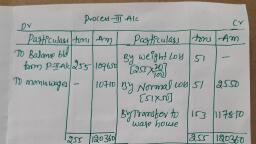

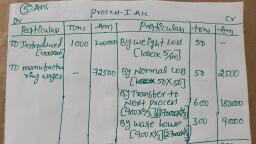

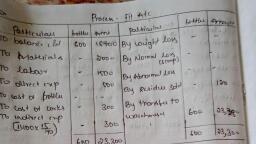

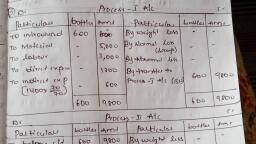

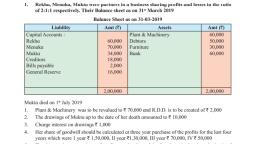

PRACTICAL PROBLEMS, When Goodwill is Created / Raised, 1. X, Y and Z are partners sharing profits and losses equally. Their balance, sheet as on 31st March 2015 was as under :, Liabilities, Amount, Assets, Amount, Trade Creditors, 25,000, Cash, 10,000, Bills payable, 17,000, Debtors, 30,000, General Reserve a/c, 18,000, Stock, 35,000, Capital :, Machinery, 50,000, 40,000, Land, 25,000, Y, 30,000, 20,000, 1,50,000, 1,50,000, On the above date, Z retires from the business on the following conditions:, a) Stock and Machinery to be depreciated by 10%., b) Provided for bad debts @ 5% on debtors., c) Land revalued at 35,000., d) Goodwill of the firm valued at 60,000., Give necessary journal entries, ledger accounts and opening balance sheet of X and Y, (Ans. Revaluation profit : Nil: Capital : X 66,000, Y 56,000,, Z's loan a/c 46,000; Balance sheet total 2,10,000), 1

Page 2 :

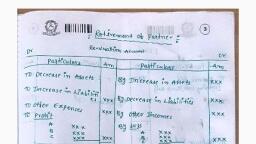

Revaluation A/c, Cr., Dr., Particulars, JF, Amount Date, Particulars, JF Amount, Date, To Stock a/c, By Land a/c, 35,00,0 x, 10, 10.Ø, 3,500, (35000 – 25000), 10,000, To Machinery a/c, 50,00,0 x, 10, 10 Ø, 5,000, To Provision for bad, debts a/c-, 30,000 x, 100, 1,500, 10,000, 10,000, Dr., Goodwill Account, Cr., Date, Particulars, JF, Amount Date, Particulars, JF, Amount, 20,000, By Balance c/d., 60,000, To X Capital a/c, To Y Capital a/c, To Z Capital a/c, 20,000, 20,000, 60,000, 60,000, To Balance b/d, 60,000, Dr., Capital Accounts, Cr., Particulars JF, Y, Particulars, JF, Y, To Z loan a/c, 46,000 By Balance b/d, 40,000 30,000 20,000, To Balance c/d, 66,000 56,000, By General, Reserve a/c, 6,000, 6,000, 6,000, By Goodwill a/c, 20,000 20,000 20,000, 66,000 56,000 46,000, 66,000 56,000 46,000, By Balance b/d, 66,000 56,000, 2

Page 3 :

Balance Sheet of X and Y as on 1-4-2015, Amount, Assets, Liabilities, Amount, 10,000, Trade creditors, 25,000, Cash, Debtors 30000-1500, 28,500, Bills payable, 17,000, 31,500, Z Loan, 46,000, Stock 35000 – 3500, 45,000, Capitals, Machinery 50000 – 5000, 35,000, 66,000, Land 25000 + 10000, 56,000, Goodwill, 60,000, Y, 2,10,000, 2,10,000, 2. X and Y are partners sharing profits and losses in the ratio of 3: 2. Their, balance sheet as on 31st March 2015 was as follows :, Liabilities, Amount, Assets, Amount, Capitals, Buildings, 30,000, 30,000, Machinery, 25,000, Y, 20,000, Investments, 15,000, General Reserve, 15,000, Stock, 28,000, P & L a/c, 10,000, Debtors, 20,000, Creditors, 25,000, Cash, 2,000, Bank overdraft, 20,000, 1,20,000, 1,20,000, X retires from the business on the following terms:, a) Goodwill is valued at 20,000., b) Depreciate stock and machinery by 10%., c) Provide for bad debts at 6%., d) Buildings are valued at ? 35,000., Give journal entries, necessary Ledger accounts and the Balance sheet., (Ans. Revaluation loss : 1,500; Capital Y - 37,400, X's Loan a/c- 56,100; Balance sheet total 1,38,500, 3

Page 4 :

Dr., Revaluation Account, Cr., Date, Particulars, JF Amount Date, Particulars, JF Amount, To Machinery (-) 2500, 2,500, By Buildings, 5,000, By X's capital a/c 900, By Y's capital a/c 600, To Stock (-) 2800, 2,800, To Debtors (-) 120, 1,200, 1,500, 6,500, 6,500, Dr., Goodwill Account, Cr., Date, Particulars, JF, Amount Date, Particulars, JF Amount, To X Capital a/c, To Y Capital a/c, 12,000, By Balance c/d, 20,000, 8,000, 20,000, 20,000, To Balance b/d, 20,000, Dr., Capital A/cs, Cr., Particulars, LF, Y, Particulars, LF, Y, To Revaluation a/c, 900, 600 By Balance b/d, 30,000, 20,000, To X Loan a/c, 56,100, By General, To Balance b/d, 37,400, Reserve a/c, 9,000, 6,000, By Goodwill a/c, 12,000, 8,000, By P & L a/c, 6,000, 4,000, 57,000 38,000, 57,000, 38,000, Y Balance Sheet as on 31-3-2015, Liabilities, Amount, Assets, Amount, Creditors, 25,000, Buildings, 30,000, Bank overdraft, 20,000, (+), 5,000, 35,000, X Loan a/c, 56,100, Machinery, 25,000, Y Capital, 37,400, (-) 2,500, 22,500, 4

Page 5 :

e O a Parlner, Liabilities, Amount, Assets, Amount, Investments, 15,000, Stock, 28,000, (-) 2,800, 25,200, Debtors, 20,000, (-) 1,200, 18,800, Cash, 2,000, Goodwill, 20,000, 1,38,500, 1,38,500, 3. S, P andG were partners sharing profits and losses in the ratio of 4: 3: 3., Their balance sheet as on 31st March 2015 was as under:, Liabilities, Amount, Assets, Amount, Capitals :, Buildings, 1,20,000, 1,20,000, Furniture, 4,000, 60,000, Machinery, 60,000, G, 40,000, Stock, 20,000, General Reserve a/c, 24,000, Debtors, 21,600, Creditors, 36,000, Cash, 54,400, 2,80,000, 2,80,000, G retires from the business on the following terms:, a) Buildings valued at 1,30,000., b) Depreciate Furniture and Machinery by 10%., c) Provide for bad debts at 1,600., d) Creditors ? 6,000 need not be paid., e) Goodwill valued at ? 27,000., f). G will be paid 17,700 immediately and the balance is transferred to his loan, account,, Give journal entries, ledger accounts and balance sheet of S and P, (Ans. Revaluation profit 8,000, Capitals : S1,43,600, P 77,700,, G's loan a/c ? 40,000 ; Balance sheet total 2,91,300)