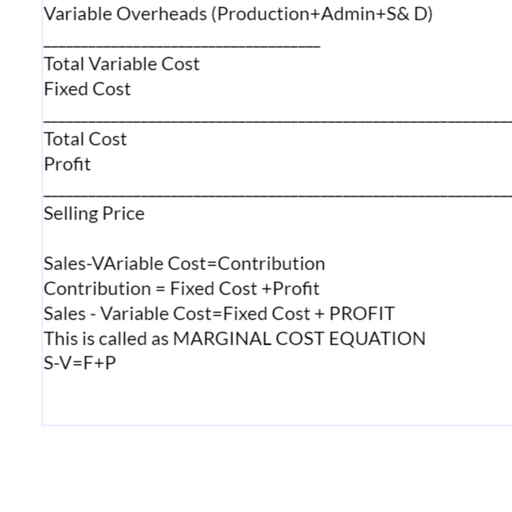

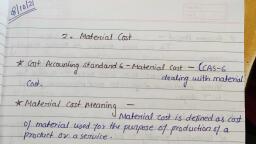

Page 2 :

Selection of Supplier, Depends upon, • Quantity, •Price, •Quality, •Terms of delivery, •Terms of payment, •Past performance, •Reputation of supplier

Page 3 :

Purchase Order, Purchase order is a request to the supplier made by purchaser, Prepare carefully, A legal obligation for accepting material and payment, On this basis, stores department receives material, On this basis Account department make payment, 5 copies= supplier, goods receiving department, accounts, department, indented department, Purchases department, • Follow up required about acceptance, promise of delivery,, delivery promise kept, •, •, •, •, •, •

Page 4 :

Contents of Purchase order, PO number,, Date, Code, Number of, Material, Name and, address of, supplier, , Price, Terms of, Payment, , Name and, address of, purchaser, , Full description, of materials, , Mode of, Transport,, estimated, delivery time, , Signatures of, authorised, persons

Page 6 :

Receipt of materials, Receiving department needs to, Take delivery, Open packages, Check quantity with order, Notify discrepancy, Prepare Goods Received Note (GRN) and send to, respective departments, • Signs duplicate copy of delivery memo of supplier., • Delivery memo is evidence of goods received and not, of goods accepted, •, •, •, •, •

Page 7 :

Inspection, • Inspection officer’s duty, • Check according to specifications, • Prepare Material Inspection Note with remark, of accepted or rejected, • Copy sent to supplier, receiving department,, office

Page 8 :

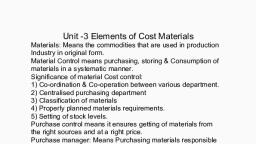

• After inspection Goods Received Note is prepared by, receiving official, • Accounts department verifies all documents and, makes payment to the supplier., • Material is issued to the production department on, the basis of material requisition., • Material requisition is a document used to authorise, and record the issue of materials from the stores., • Bill of Materials is prepared by planning department, in prescribed form.

Page 9 :

Bill of Materials : Planning department, Production department, Stores department, Entry in bin card, Issue material to production department, Costing department enters into store ledger

Page 10 :

MAIN TECHNIQUES OF INVENTORY, CONTROL, A), B), C), D), E), F), G), H), , Determination of stock levels., Economic order quantity., Ved analysis., Material turnover ratio., Abc analysis., Perpetual inventory system., Simplification and standardization., Classification and codification.

Page 11 :

Fixation of Stock levels, Funds, , Storage space, , Storage loss, , Cost of storage, , Regularity in availing, material, , Rate of consumption, of material, , Time lag, , Price fluctuations, , Economic order or, reorder quantity

Page 12 :

DETERMINATION OF STOCK LEVELS, REORDERING LEVEL, AVERAGE STOCK, LEVEL, Minimum stock level, Stock, levels, , DANGER LEVEL, , MAXIMUM STOCK LEVEL

Page 13 :

2) MINIMUM STOCK LEVEL:, Minimum Stock level = Reordering level +, (Normal Consumption × Normal Reorder, Period

Page 14 :

1) REORDERING LEVEL:, Reordering level= minimum level +( normal, consumption ×Normal Reorder Period), OR, , • maximum consumption × maximum, reorder period

Page 15 :

• 3) MAXIMUM STOCK LEVEL:, Maxi. Stock level = (Reorder level +, Reorder quantity) – (Minimum, consumption × Minimum reorder, period)

Page 16 :

• 4) DANGER LEVEL:, Danger level = (Normal consumption ×, Maximum reorder period for emergency, purchases)

Page 17 :

• 5) AVERAGE STOCK LEVEL:, Avg. stock level: ½ (Maximum stock, level + Minimum stock level), OR, Minimum stock level + ½ (Reorder Qty)

Page 18 :

B) ECONOMIC ORDER QUANTITY, EOQ, , CARRYING, COST, , ORDERING, COST

Page 19 :

E.O.Q = 2AO, C, Where, A = Annual consumption, O= Cost of placing an order, C= Inventory Carrying Cost, , •

Page 20 :

•Number of orders placed during the year, , = Annual Consumption, EOQ, •Total Cost of placing orders in a year, , = No. of orders × Cost of placing an order, •Annual Storage Cost = EOQ × Carrying cost per unit, 2

Page 21 :

MATERIAL TURNOVER RATIO, • M.T.R = Cost of material consumed, during the period, Cost of average stock held, during the period, Average stock = op. stock + cl. Stock, 2

Page 22 :

A.B.C Analysis, • Abc stands for always better control system. In, this technique basically important material is, controlled keenly and unimportant material is, left out.

Page 23 :

ADVANTAGES OF ABC ANALYSIS, •, •, •, •, •, , Reduction in purchase cost, Proper control, Best utilisation of resources, Minimum investment, Reduction in control cost

Page 24 :

PERPETUAL INVENTORY SYSTEM, It is a system of records maintained by the, controlling department, which reflects the, physical movement of stocks and their current, balance., Bincard and stores ledger are maintained which, show goods received, issued.

Page 25 :

CLASSIFICATION AND CODIFICATION:, • Classification and codification of materials are, essential for a good system of store keeping., • Codification is next stage of classification of, stores.

Page 26 :

INVENTORY RECORDS, • Two important records of material received &, issued are generally kept., , BINCARD, , STORES, LEDGER

Page 27 :

BINCARD: Bin means a place, rack, almirah or, that place where materials are stored. A, bincard is usually kept in bin. It provides, quantitative record of receipts, issues &, balances of stock., It is maintained by store keeper.

Page 28 :

STORES LEDGER: This ledger is kept in costing, dept. This ledger provides the information, for pricing if materials issued and the money, value at any time of each item of stores.