Page 1 :

T.Y.B.COM. - COST ACCOUNTING, Manan Prakashan, , 1, , CHAPTER - 1 : COST CONTROL ACCOUNTS, MULTIPLE CHOICE QUESTIONS, 1. Materials Requisition Note, (a) authorises and records the issue of materials for use, (b) records the return of unused materials, (c) records the transfer of materials from one store to another, (d) a classified record of materials, issues, returns and transfers, 2. Materials Transfer Note, (a) authorises and records the issue of materials for use, (b) records the return of unused materials, (c) records the shifting of materials from one store to another, (d) a classified record of materials, issues, returns and transfers, 3. A document which is a classified record of material issues, returns and transfers, (a) Materials Requisition Note, (b) Materials Return Note, (c) Materials Transfer Note, (d) Materials Issue Analysis Sheet, 4. This is essential to make the cost ledger 'self-balancing’., (a) General Ledger Adjustment Account, (b) Stores Ledger Control Account, (c) Work-in-Progress Ledger, (d) Finished Goods Control Account, 5. This is debited with all purchases of materials for the stores and credited with all issues of, materials, (a) General Ledger Adjustment Account, (b) Stores Ledger Control Account, (c) Work-in-Progress Ledger, (d) Finished Goods Control Account, 6. In this, cost of materials, wages and overheads of each job undertaken is posted., (a) General Ledger Adjustment Account, (b) Stores Ledger Control Account, (c) Work-in-Progress Ledger, (d) Finished Goods Control Account, 7. This represents the total value of finished goods in stock., (a) General Ledger Adjustment Account, (b) Stores Ledger Control Account, (c) Work-in-Progress Ledger, (d) Finished Goods Control Account, 8. Material amounting to ` 58,300 is purchased on credit., The entry in Cost Ledger under non-integrated System is, (a) Purchases A/c, Dr., 58,300, To Sundry Creditors, 58,300, (b) Stores Ledger Control A/c, Dr., 58,300, To General Ledger Adjustment A/c, 58,300, (c) Purchases A/c, Dr., 58,300, To Cost Ledger Control A/c, 58,300, (d) Work-in-Progress Control A/c, Dr., 58,300, To General Ledger Adjustment A/c, 58,300, 9. Salaries and wages amounting to ` 62,100 gross and earned by the employees, and deductions, of ` 5,400 as provident fund. ` 2,400 as ESIC and ` 4,300 as Income Tax are made from the, gross amount., The entry in Cost Ledger under non-integrated System is, (a) Salaries and Wages Control A/c, Dr., 62,100, To General Ledger Adjustment A/c, 62,100, (b) Salaries and Wages Control A/c, Dr., 50,000, To General Ledger Adjustment A/c, 50,000, (c) Salaries and Wages Control A/c, Dr., 62,100, To Cost Ledger Adjustment A/c, 62,100

Page 2 :

2, , Cost Accounting (T.Y.B.Com.: SEM-VI), , (d) Salaries and Wages Control A/c, Dr., 62,100, To Provident Fund A/c, 5,400, To E.S.I.C. A/c, 2,400, To Income-tax A/c, 4,300, To General Ledger Adjustment A/c, 50,000, 10. A concern has a non-integrated costing system. Salaries and wages analysis book indicates the, following breakup :, Direct wages, ` 38,600, Indirect factory wages, ` 9,500, Administrative salaries, ` 9,700, Selling and distribution salaries, ` 4,300, Which of the following statements is false(i) No additional entry is passed in financial books for break-up., (ii) Work-in-progress Ledger Control A/c will be debited with ` 38,600., (iii) Salaries and Wages Control A/c will be debited with ` 62,100., (a) only (i), (b) All, (c) only (iii), (d) None, 11. In a non-integrated system of accounting, the emphasis is on,, (a) Personal accounts, (b) Real accounts, (c) Nominal accounts, (d) All of these, 12. Cost and financial accounts are required to be reconciled under, (a) Integral system, (b) Cost control accounts system, (c) Under both (a) and (b), (d) None of these, 13. Which of the following accounts makes the cost ledger self-balancing ?, (a) Overhead adjustment account, (b) Costing P & L account, (c) Cost ledger control account, (d) None of the above, 14. Purchases for special jobs is debited under non-integrated system to, (a) Work-in-progress ledger control account (b) Cost ledger control account, (c) Stores ledger control account, (d) Purchases account, 15. Journal entry for absorption of production overheads in non-integrated accounts is, (a) Production Overhead Account, Dr., Cost Ledger Control Account, Cr., (b) Work-in-Progress Account, Dr., Production Overhead Control Account, Cr., (c) Overhead Adjustment Account, Dr., Production Overhead Account, Cr., 16. Journal entry for the absorption of Selling and Distribution overhead account in non-integrated, accounts is, (a) Cost of Sales Account, Dr., Selling and Distribution Overhead Control Account, Cr., (b) Finished Goods Ledger Control Account, Dr., Selling and Distribution Overhead Account, Cr., (c) Cost Ledger Control Account, Dr., Selling and Distribution Overhead Account, Cr., (d) None of these, 17. Journal entry for over-absorbed administrative overhead amount in non-integrated accounts is, (a) Costing Profit and Loss Account, Dr., Cost Ledger Control Account, Cr., (b) Overhead Adjustment or Suspense Account, Dr., Administration Overhead Control Account, Cr., (c) Administration Overhead Account, Dr., Overhead Adjustment or Suspense Account, Cr., (d) No entry is required

Page 3 :

Manan Prakashan, , 3, , 18. Journal entry for issuing materials to production in non-integrated accounts is, (a) Stores Ledger Control Account, Dr., Cost Ledger Control Account, Cr., (b) Cost Ledger Control Account, Dr., Stores Ledger Control Account, Cr., (c) Work-in-Progress Control Account, Dr., Stores Ledger Control Account, Cr., (d) No entry is required, 19. Journal entry for payment of wages in non-integrated accounts is, (a) Wages Control Account, Dr., Cash Account, Cr., (b) Wages Control Account, Dr., Cost Ledger Control Account, Cr., (c) Wages Account, Dr., Cash Account, Cr., 20. Payment to creditors for supplies made. Journal entry in non-integrated accounts will be, (a) Sundry Creditors Account, Dr., Cash A/c, Cr., (b) Sundry Creditors Account, Dr., Cost Ledger Control Account, Cr., (c) Sundry Creditors Account, Dr., Costing Profit and Loss Account, Cr., (d) No entry is required, 21. In a period ` 50,000 was incurred on indirect labour. In a Cost Ledger, the double entry will be:, (a) Wages Control Account, Dr., Overhead Control Account, Cr., (b) WIP Control Account, Dr., Wages Control Account, Cr., (c) Overhead Control Account, Dr., Wages Control Account, Cr., (d) Wages Control Account, Dr., WIP Control Account, Cr., 22. At the end of a financial period, accounting entries for under absorbed overheads would be, (a) WIP Control Account, Dr., Overhead Control Account, Cr., (b) Profit and Loss Account, Dr., WIP Control Account, Cr., (c) Profit and Loss Account, Dr., Overhead Control Account, Cr., (d) Overhead Control Account, Dr., Profit and Loss Account, Cr., 23. The double entry for factory cost of production in a cost ledger is, (a) Cost of Sales Account, Dr., Finished Goods Control Account, Cr., (b) Finished Goods Control Account, Dr., WIP Control Account, Cr., (c) Costing Profit and Loss Account, Dr., Finished Goods Control Account, Cr., (d) WIP Control Account, Dr., Finished Goods Control Account, Cr., 24. What is an interlocking bookkeeping system?, (a) A single, combined system containing both cost accounting and financial accounting records, (b) A system combining cost accounting and management accounting, (c) A system with high secured access, (d) A system where separate accounts are kept for cost accounting and for financial accounting

Page 4 :

4, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 25. The following documents are used in accounting for raw materials:, (i) Goods received note, (ii) Materials returned note, (iii) Materials requisition note, (iv) Delivery note, Which of the documents may be used to record raw materials sent back to stores from production?, (a) (i) and (ii), (b) (i) and (iv), (c) (ii) only, (d) (ii) and (iii), 26. When production has been completed what double-entry would be made in a cost accounting, system ?, Debit, Credit, (a) Cost of Sales, Finished Goods, (b) Finished Goods, Work-in-Progress, (c) Finished Goods, Cost of Sales, (d) Work-in-Progress, Finished Goods, 27. The raw materials issued to a job were overestimated and the excess is being sent back to the, materials store. What document is required?, (a) Stores credit note, (b) Stores debit note, (c) Materials returned note, (d) Materials transfer note, 28. When goods are sold, what double-entry would be made to record the transfer of costs?, Debit, Credit, (a) Finished Goods Account, Cost of Sales Account, (b) Sales Account, Cost of Sales Account, (c) Cost of Sales Account, Sales Account, (d) Cost of Sales Account, Finished Goods Account, 29. The stores ledger control account for a period contained the following summary information :, ` '000, Supplier deliveries into stores, 321, Indirect materials issued from stores, 13, Returns to suppliers, 8, Opening inventory in stores, 46, Closing inventory in stores, 59, There were no inventory discrepancies in the period., What accounting entry correctly records the issue of direct materials from stores ?, Debit, `, Credit, `, (a) Stores Ledger Account, 2,87,000, Work-in-Progress Account, 2,87,000, (b) Work-in-Progress Account, 2,87,000, Stores Ledger Account, 2,87,000, (c) Stores Ledger Account, 3,13,000, Work-in-Progress Account, 3,13,000, (d) Work-in-Progress Account, 3,13,000, Stores Ledger Account, 3,13,000, 30. What is a cost ledger control account?, (a) An account in the cost ledger to record financial accounting items, (b) An account in the financial ledger to record cost accounting items, (c) An account that summarises outstanding payables balances, (d) An account that summarises outstanding receivables balances, 31. The advantages of maintaining cost control accounts include the following:, (a) facilitate prompt preparation of costing profit and loss account, (b) help management in policy formulation, (c) facilitate internal check, (d) all of the above, 32. The Work-in-Progress Control Account is not debited with :, (a) direct materials and direct labour, (b) direct expenses, (c) production overheads (recovered), (d) selling and distribution overheads, 33. The application of factory overheads usually would be recorded as an increase in, (a) Cost of goods sold, (b) Work-in-progress control, (c) Factory overheads control, (d) Finished goods control

Page 5 :

Manan Prakashan, , 5, , 34. Production overheads incurred, ` 10,000, Production overheads recovered, ` 12,000, The entry for over-recovery of overheads is, (a) Production Overheads Control A/c, Dr., To Overheads Adjustment A/c, (b) Overheads Adjustment A/c, Dr., To Production Overheads A/c, (c) Work-in-Progress A/c, Dr., To Overheads Adjustment A/c, (d) Overheads Adjustment A/c, Dr., To Work-in-Progress A/c, 35. Loss of stores (normal) is recorded in cost accounts as, Stores Ledger, Production Overheads, Costing P/L A/c, (a) Debit, Credit, Nothing, (b) Credit, Debit, Nothing, (c) Nothing, Debit, Credit, (d) Credit, Nothing, Debit, 36. In a typical cost ledger, the double entry for indirect labour charges incurred during a period is, Debit, Credit, (a) Wages control account, Overheads control account, (b) WIP control account, Wages control account, (c) Overheads control account, Wages control account, (d) Wages control account, WIP control account, 37. In the cost ledger, the double entry for factory cost of finished production for a period is, Debit, Credit, (a) Cost of sales account, Finished goods control account, (b) Finished goods control account, Work-in-progress control account, (c) Costing profit and loss account, Finished goods control account, (d) Work-in-progress control account, Finished goods control account, 38. Stores issued to factory repair order is recorded as, (a) Stores Ledger A/c, Dr., To Production Overheads A/c, (b) Profit and Loss A/c, Dr., To Stores Ledger A/c, (c) Production Overheads Control A/c, Dr., To Stores Ledger A/c, (d) Stores Ledger A/c, Dr., To Profit and Loss A/c, 39. The debit balance of the overheads adjustment account may be transferred to, (a) Cost of sales account, (b) Profit and loss account, (c) Finished goods account, (d) Work-in-progress account, 40. Materials lost in stores due to fire is, (a) a part of normal loss and hence part of cost, (b) capitalized, (c) a part of abnormal loss and hence excluded from cost, (d) transferred to the next period, 41. A credit to Work in Process Inventory represents, (a) work still in process, (b) raw material put into production, (c) the application of overhead to production, (d) the transfer of completed items to Finished Goods Inventory

Page 6 :

6, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 42. A journal entry includes a debit to Work in Process Inventory and a credit to Raw Material Inventory., The explanation for this would be that, (a) indirect material was placed into production, (b) raw material was purchased on account, (c) direct material was placed into production, (d) direct labour was used for production, 43. The journal entry to apply overhead to production includes a credit to Manufacturing Overhead, control and a debit to, (a) Finished Goods Inventory, (b) Work in Process Inventory, (c) Cost of Goods Sold, (d) Raw Material Inventory, 44. The use of indirect material would usually be reflected as an increase in, (a) Stores control, (b) Work in process control, (c) Manufacturing overhead applied, (d) Manufacturing overhead control, 45. A credit to the Manufacturing overhead control account represents the, (a) actual cost of overhead incurred, (b) actual cost of overhead paid this period, (c) amount of overhead applied to production, (d) amount of indirect material and labour used during the period, 46. When employees assemble products, (a) Cost of goods manufactured decreases (b) Work in process inventory increases, (c) Work in process inventory decreases, (d) Manufacturing overhead decreases, 47. W Corporation’s production department used ` 64,000 of materials to manufacture products, during May. Which one of the following is one effect of recording this transaction?, (a) Raw materials increases by ` 64,000, (b) Manufacturing overhead increases by ` 64,000, (c) Cost of goods sold increases by ` 64,000, (d) Work in process increases by ` 64,000, 48. The Finished Goods account contains the cost of all units, (a) Unfinished at a given point in time, (b) Completed at a given point in time, (c) Produced during a particular period, (d) Produced and sold during a particular period, 49. The work in process account is credited when, (a) Production of product is completed, (b) Products are sold to customers, (c) Completed goods are shipped to buyers (d) Costs of production are incurred, 50. Which account balances will decrease as a result of completing products during the month?, (a) Only work-in-process inventory, (b) Only finished goods inventory, (c) Both work-in-process and finished goods ending balances will decrease, (d) Neither account ending balance would increase; both would increase, 51. T Company completed two jobs whose costs total to ` 1,20,000. Which one of the following is, one effect of this transaction?, (a) Manufacturing Overhead increases by ` 1,20,000, (b) Cost of Goods Sold increases by ` 1,20,000, (c) Work in Process decreases by ` 1,20,000, (d) Finished Goods decreases by ` 1,20,000, 52. N Corporation incurred ` 8,000 indirect labour and ` 42,000 direct labour. Which one of the, following is one effect of recording this transaction?, (a) Indirect labour increases by ` 8,000, (b) Work in process increases by ` 50,000, (c) Manufacturing costs increase by ` 42,000, (d) Manufacturing overhead increases by ` 8,000, 53. The balance of the Work in Process account is equal to, (a) The total costs of the jobs completed, (b) The total costs of the jobs completed and sold, (c) The total manufacturing costs incurred during the period, (d) The total costs of the incomplete jobs

Page 7 :

Manan Prakashan, , 7, , 54. What entry should be made when a job is completed?, (a) A debit to Finished Goods Inventory, and a credit to Work in Process Inventory, (b) A debit to Work in Process Inventory, and a credit to Direct Materials, Direct Labour and, Manufacturing Overhead, (c) A debit to Finished Goods Inventory and a credit to Direct Materials, Direct Labour, and, Manufacturing Overhead, (d) A debit to Cost of Goods Sold Inventory, and a credit to Work in Process Inventory, 55. When indirect materials are requisitioned the, account is increased., (a) Manufacturing Overhead Control, (b) Work-in-Process Control, (c) Materials Control, (d) Accounts Payable Control, 56. The Manufacturing Overhead Control account, (a) is increased by allocated manufacturing overhead, (b) is credited with amounts transferred to Work-in-Process, (c) is decreased by allocated manufacturing overhead, (d) is debited with actual overhead costs, 57. A company’s accounting system operates so that the cost accounts are independent of the, financial accounts. The two sets of accounts are reconciled on a regular basis to keep them, continuously in agreement. This type of accounting system is known as, (a) Independent accounts, (b) Interlocking accounts, (c) Reconciled accounts, (d) Integrated accounts, 58. In May, material requisitions were ` 44,000 (` 39,000 of these were direct materials), and raw, material purchases were ` 57,700. The end of month balance in raw materials inventory a/c was, ` 24,300. What was the beginning raw materials inventory a/c balance?, (a) ` 10,600, (b) ` 43,000, (c) ` 72,400, (d) ` 25,300, 59. Overallocated manufacturing overhead results when, (a) production is less than last year, (b) estimated overhead is less than actual overhead, (c) actual overhead is less than allocated overhead, (d) actual overhead is less than expected, 60. Determining how much manufacturing overhead is overallocated or underallocated, (a) is done before the period starts, (b) is done during the period, (c) can be done at any time, (d) is done at the end of the period, 61. The journal entry to record the use of direct materials on jobs is to debit work in process inventory, and credit, (a) raw materials inventory, (b) finished goods inventory, (c) manufacturing overhead, (d) wages payable, 62. Cost of goods sold is debited and finished goods inventory is credited for, (a) purchase of goods on account, (b) transfer of goods to the finished goods storeroom, (c) transfer of materials into work in process inventory, (d) the sale of goods to a customer, 63. Under which of the following situations is finished goods inventory debited and work in process, inventory credited?, (a) Transfer of goods to the finished goods storeroom, (b) Purchase of goods on account, (c) Transfer goods out of the factory, (d) Transfer of material to work in process inventory, 64. Under which of the following situations is raw materials inventory credited and work in process, inventory debited?, (a) We ship goods to the customer, (b) Material is transferred to the factory, (c) We transfer goods to the storeroom, (d) We purchase goods on account

Page 8 :

8, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 65. The cost of direct materials used in production is debited to, (a) either manufacturing overhead or work in process, (b) finished goods inventory, (c) work in process, (d) manufacturing overhead, 66. The cost of direct labour used in production is recorded as a, (a) debit to work in process, (b) debit to manufacturing overhead, (c) debit to wages expense, (d) debit to wages payable, 67. The cost of indirect labour used in the factory is recorded as a, (a) credit to work in process, (b) debit to manufacturing overhead, (c) credit to wages payable, (d) debit to wages expense, 68. The journal entry needed to record the completion of a job includes a, (a) credit to work in process, (b) credit to finished goods inventory, (c) debit to work in process inventory, (d) debit to cost of goods sold, 69. The journal entry needed to record the completion of a job includes a, (a) debit to cost of goods sold, (b) debit to work in process, (c) debit to finished goods inventory, (d) debit to raw materials inventory, 70. The journal entry to issue ` 600 of direct materials and ` 40 of indirect materials involves a debit, to, (a) manufacturing overhead for ` 640, (b) work in process for ` 640, (c) work in process for ` 600 and a credit to manufacturing overhead for ` 40, (d) work in process for ` 600 and a debit to manufacturing overhead for ` 40, 71. To record the costs of indirect labour, which of the following would be debited?, (a) Work in process, (b) Manufacturing overhead, (c) Finished goods inventory, (d) Wages payable, 72. To record direct labour costs incurred, which of the following would be debited?, (a) Finished goods inventory, (b) Manufacturing overhead, (c) Work in process, (d) Wages payable, 73. To record the requisition of direct materials, which of the following would be debited?, (a) Finished goods inventory, (b) Work in process, (c) Raw materials inventory, (d) Cost of goods manufactured, 74. The journal entry to record ` 300 of depreciation expense on factory equipment involves a, (a) debit to accumulated depreciation for ` 300, (b) debit to manufacturing overhead for ` 300, (c) debit to depreciation expense for ` 300, (d) credit to manufacturing overhead for ` 300, 75. Actual manufacturing overhead for the period is ` 20,000 while allocated manufacturing overhead, is ` 18,000. What entry will close the manufacturing overhead balance?, (a) Debit manufacturing overhead and credit work in process for ` 2,000, (b) Debit manufacturing overhead and credit cost of goods sold for ` 2,000, (c) Debit cost of goods sold and credit finished goods inventory for ` 2,000, (d) Debit cost of goods sold and credit manufacturing overhead for ` 2,000, 76. A company has overallocated manufacturing overhead by ` 1,500. The entry to close, manufacturing overhead account would be to, (a) debit manufacturing overhead and credit cost of goods sold for ` 1,500, (b) debit manufacturing overhead and credit work in process for ` 1,500, (c) debit cost of goods sold and credit manufacturing overhead for ` 1,500, (d) debit cost of goods sold and credit finished goods inventory for ` 15,000, 77. Manufacturing overhead has an underallocated balance of ` 6,200; raw materials inventory, balance is ` 50,000; work in process inventory is ` 30,000; finished goods inventory is ` 20,000;, and cost of goods sold is ` 1,00,000., Which of these accounts would have a closing credit balance?, (a) Raw materials inventory, (b) Finished goods inventory, (c) Work in process inventory, (d) None of the above

Page 9 :

Manan Prakashan, , 9, , 78. The entry to record cost of goods sold includes a credit to, (a) Cost of Goods Sold, (b) Finished Goods Inventory, (c) Sales, (d) Work in Process Inventory, , ANSWERS, 1., 2., 3., 4., 5., 6., 7., 8., 9., 10., 11., 12., , (a), (c), (d), (a), (b), (c), (d), (b), (a), (c), (c), (b), , 13., 14., 15., 16., 17., 18., 19., 20., 21., 22., 23., 24., , (c), (a), (b), (a), (c), (c), (b), (d), (c), (c), (b), (d), , 25., 26., 27., 28., 29., 30., 31., 32., 33., 34., 35., 36., , (c), (b), (c), (d), (b), (a), (d), (d), (b), (a), (b), (c), , 37., 38., 39., 40., 41., 42., 43., 44., 45., 46., 47., 48., , (b), (c), (b), (c), (d), (c), (b), (d), (c), (b), (d), (b), , Hints :, 58. [X + ` 57,700 – 44,000 = ` 24,300; X = ` 10,600], , 49., 50., 51., 52., 53., 54., 55., 56., 57., 58., 59., 60., , (a), (a), (c), (d), (d), (a), (a), (d), (b), (a), (c), (d), , 61., 62., 63., 64., 65., 66., 67., 68., 69., 70., 71., 72., , (a), (d), (a), (b), (c), (a), (b), (a), (c), (d), (b), (c), , 73., 74., 75., 76., 77., 78., , (b), (b), (d), (a), (d), (b)

Page 10 :

10, , Cost Accounting (T.Y.B.Com.: SEM-VI), , CHAPTER - 2 : CONTRACT COSTING, MULTIPLE CHOICE QUESTIONS, A., , Conceptual, , 1. Contract costing is a basic method of, (a) Historical costing, (b) Specific order costing, (c) Process costing, (d) Standard costing, Costing., 2. Contract costing is a variant of, (a) Job, (b) Process, (c) Unit, (d) Batch, 3. Contract costing usually applicable in, (a) Constructional Works, (b) Textile Mills, (c) Cement Industries, (d) Chemical Industries, 4., is the person for whom the Contract job is undertaken., (a) Contractor, (b) Contractee, (c) Sub-contractor, (d) Job-worker, 5. Which one of the following is not a contract cost ?, (a) Direct wages, (b) Depreciation of plant, (c) Sub-contractors’ fees, (d) Architects’ certificates, 6. The degree of completion of work is determined by comparing the work certified with, (a) Contract price, (b) Work in progress, (c) Cash received on contract, (d) Retention money, 7. In contract costing credit is taken only for a part of the profit on, (a) Completed contract, (b) Incomplete contract, (c) Work uncertified, (d) Work Certified, 8. In contract costing payment of cash to the contractor is made on the basis of, (a) Uncertified work, (b) Certified work, (c) Work in progress, (d) Retention Money, 9. The cost of any sub-contracted work is, (a) A direct expense of a contract and is debited to the contract account, (b) An indirect expense of a contract and is debited to the contract account, (c) A direct expense of a contract and is debited to the client account, (d) An indirect expense of a contract and is debited to the client account, 10. Progress payments received by the contractor from the client are, (a) Debited to the contract account, (b) Credited to the contract account, (c) Debited to the client account, (d) Credited to the client account, 11. Retention Money is equal to, (a) Work certified Less Work uncertified, (b) Contract price Less Work certified, (c) Work certified Less Payment received by contractor, (d) None of the above, 12. Material supplied by the Contractee, (a) is debited to the Contract Account, (b) is ignored in the Contract Account, (c) is credited to the Contract Account, (d) is debited to the Contractee’s Account, 13. Cost of material lost or destroyed, (a) is credited to the Contract Account, (b) is debited to the Contract Account, (c) is debited to the Costing Profit and Loss Account, (d) is credited to the Costing Profit and Loss Account

Page 11 :

Manan Prakashan, , 11, , 14. Work Certified is valued at, (a) Cost price, (b) Market price, (c) Cost or market price whichever is less, (d) Estimated price, 15. Value of Work Certified Less Profit =, (a) Work-in-progress, (b) Cost of Work Certified, (c) Retention Money, (d) Cost of uncertified work, 16. The Total Value of Work Completed during an accounting year is equal to, (a) Work Certified + Progress Payment Received, (b) Work Certified + Work Uncertified, (c) Work Certified + Retention Money, (d) None of the above, 17. Notional Profit is equal to, (a) Work certified Less Cost of work certified, (b) Work certified Less Cost of work completed, (c) Payment received Less Work certified, (d) None of the above, 18. Work-in-progress at year end is equal to, (a) only closing stock of materials, (b) only work certified, (c) only work uncertified, (d) the total of all the above, 19. Work certified is less than 25% of the contract price. The transfer to P & L A/c will be, (a) 1/3 rd of Notional profits, (b) NIL, (c) 2/3 rd of Notional profits, (d) 100% of Notional profits, 20. Work certified is between 25% and 50% of the contract price. The transfer to P & L A/c will be, (a) 1/3 rd of Notional profits, reduced in the ratio of cash received to work certified, (b) NIL, (c) 2/3 rd of Notional profits, reduced in the ratio of cash received to work certified, (d) 100% of Notional profits, 21. Work certified is between 50% and 90% of the contract price. The transfer to P & L A/c will be, (a) 1/3 rd of Notional profits, reduced in the ratio of cash received to work certified, (b) NIL, (c) 2/3 rd of Notional profits, reduced in the ratio of cash received to work certified, (d) 100% of Notional profits, 22. The entire contract is complete. The transfer to P & L A/c will be, (a) 1/3 rd of Notional profits, (b) NIL, (c) 2/3 rd of Notional profits, (d) Entire profit, 23. If a contract is 40% complete, credit taken to the profit and loss account is, (a) 40% of the notional profit, (b) 1/3 rd of Notional profits, reduced in the ratio of cash received to work certified, (c) NIL, (d) 2/3 rd of Notional profits, reduced in the ratio of cash received to work certified, , B., , Numerical, , 24. Value of work certified - ` 5,00,000, Cost of work to date - ` 4,00,000, Cost of work not yet certified - ` 1,00,000, Notional Profit is, (a) ` 1,00,000, (b) Nil, (c) Loss ` 1,00,000, (d) ` 2,00,000, 25. The total profit on a contract for ` 3,00,000 is ` 60,000 and the contract is 60% complete and has, been certified accordingly. The retention money is 20% of the certified value, then the amount of, profit that can be prudently credited to Profit and Loss Account, (a) ` 60,000, (b) ` 36,000, (c) ` 28,800, (d) ` 48,000

Page 12 :

12, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 26. Contract cost - ` 2,80,000, Contract value - ` 5,00,000, Cash received - ` 2,70,000, Uncertified work - ` 30,000, Deduction from bills by way of retention money is 10%., How much profit, if any, you would take to the profit and loss account?, (a) ` 50,000, (b) ` 33,333, (c) ` 30,000, (d) Nil, 27-28 : Total cost of contract to date - 3,83,000, Cost of contract not yet to certified - 23,000, Value of work certified - 4,20,000, Cash received to date - 3,78,000, 27. Value of work-in-progress is, (a) ` 65,000, (b) ` 41,000, (c) ` 23,000, (d) ` 14,000, 28. Reserve for contingencies is, (a) ` 60,000, (b) ` 24,000, (c) ` 36,000, (d) ` 1,000, , ANSWERS, 1., 2., 3., 4., , (b), (a), (a), (b), , 5., 6., 7., 8., , (d), (a), (b), (b), , 9., 10., 11., 12., , (a), (d), (c), (b), , 13., 14., 15., 16., , (a), (a), (b), (b), , 17., 18., 19., 20., , (a), (d), (b), (a), , 21., 22., 23., 24., , (c), (d), (b), (d), , 25., 26., 27., 28., , (c), (c), (b), (b), , Hints :, 24. [5,00,000 - (4,00,000 - 1,00,000)], 25. [60,000 x 80% x 1,80,000 x 3,00,000], 26. [Notional profit = [(2,70,000 x 100/90) + 30,000] - 2,80,000 = 50,000; Tfd. To P & L : 50,000 x 2/3, x 90 / 100], 27. [4,20,000 + 23,000 - 24,000 - 3,78,000], 28. [(4,20,000 + 23,000 - 3,83,000) x 2/3 x 3,78,000 / 4,20,000]

Page 13 :

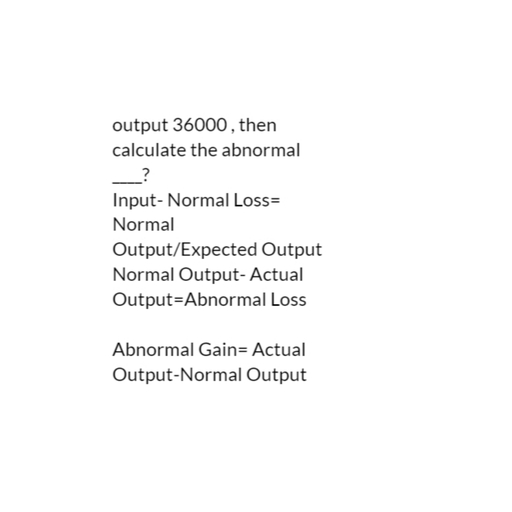

Manan Prakashan, , 13, , CHAPTER - 3 : PROCESS COSTING, MULTIPLE CHOICE QUESTIONS, I., , PROCESS COSTING - MAIN PRODUCT, , A., , Conceptual, , 1. Process costing is applied when, (a) small number of different products are manufactured, (b) large number of different products are manufactured, (c) large number of identical products are manufactured, (d) small numbers of customised made-to-order products are manufactured, 2. Which of the following does not use process costing ?, (a) Oil refining, (b) Distilleries, (c) Sugar, (d) Air-craft manufacturing, 3. Which cost accumulation procedure is most applicable in continuous mass-production, manufacturing environments?, (a) Standard, (b) Actual, (c) Process, (d) Job order, 4. Which of the following statements is false?, (a) In process costing, cost is accumulated according to processes or departments, (b) In job costing, the basis of cost accumulation is job order or batch size, (c) In process costing, cost is accumulated on time basis, (d) In job costing, cost is computed at the end of the cost period, 5. Process Cost is based on the concept of, (a) Average Cost, (b) Marginal Cost, (c) Standard Cost, (d) Differential Cost, 6. Normal Loss is equal to, (a) Normal Output - Actual Output, (b) Actual Output - Normal Output, (c) Input x % of Normal Loss, (d) None of the above, 7. Normal Output is equal to, (a) Input - Abnormal Loss, (b) Input - Normal Loss, (c) Input - Abnormal Gains, (d) None of the above, 8. Unit Cost is equal to, (a) Normal Cost ÷ Normal Output, (b) Total Cost ÷ Normal Output, (c) Normal Cost ÷ Total Output, (d) Total Cost ÷ Total Output, 9. Abnormal Loss is equal to, (a) Input - Actual Output, (b) Actual Output - Normal Output, (c) Normal Output - Actual Output, (d) Actual Output - Input, 10. Abnormal Gains are equal to, (a) Actual Output - Normal Output, (b) Normal Output - Actual Output, (c) Actual Output - Input, (d) Input - Actual Output, 11. Process cost is very much applicable in, (a) Construction Industry, (b) Pharmaceutical Industry, (c) Airline Company, (d) None of these, 12. In process costing, each producing department is a, (a) Cost unit, (b) Cost centre, (c) Investment centre, (d) Sales centre, 13. Which of the given units can never become part of first department of Cost of Production Report?, (a) Units received from preceding department, (b) Units transferred to subsequent department, (c) Lost units, (d) Units still in process

Page 14 :

14, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 14. When production is below standard specification or quality and cannot be rectified by incurring, additional cost, it is called, (a) Defective, (b) Spoilage, (c) Waste, (d) Scrap, 15. What will be the impact of normal loss on the overall per unit cost ?, (a) Per unit cost will increase, (b) Per unit cost will decrease, (c) Per unit cost remain unchanged, (d) Normal loss has no relation to unit cost, , B., , Numerical, , 16. 12,000 kg of a material were input to a process in a period. The normal loss is 10% of input., There is no opening or closing work-in-progress. Output in the period was 10,920 kg. What was, the abnormal gain/loss in the period ?, (a) Abnormal gain of 120 kg, (b) Abnormal loss of 120 kg, (c) Abnormal gain of 1,080 kg, (d) Abnormal loss of 1,080 kg, 17. Wastage of a raw material during a manufacturing process is 20% of input quantity. What input, quantity of raw material is required per kg of output?, (a) 0.8 kg, (b) 1.2 kg, (c) 1.25 kg, (d) 1.33 kg, 18. 400 litres of a chemical were manufactured in a period. There is a normal loss of 25% of the, material input into the process. An abnormal loss of 5% of material input occurred in the period., How many litres of material (to the nearest litre) were input into the process in the period?, (a) 500, (b) 520, (c) 560, (d) 571, 19. A company uses process costing to value its output. The following was recorded for the period:, Input materials 2,000 units at ` 4.50 per unit, Conversion costs ` 13,340, Normal loss 5% of input valued at ` 3 per unit, Actual loss 150 units, There were no opening or closing stocks., What was the valuation of one unit of output to one decimal place?, (a) ` 11.8, (b) ` 11.6, (c) ` 11.2, (d) ` 11.0, 20. A company uses process costing to value its output and all materials are input at the start of the, process., The following information relates to the process for one month:, Input 3,000 units, Opening stock 400 units, Losses 10% of input is expected to be lost, Closing stock 200 units, How many good units were output from the process if actual losses were 400 units?, (a) 2,800 units, (b) 2,900 units, (c) 3,000 units, (d) 3,200 units, 21. The cost of production of 40 units in Process I consisting of materials ` 1,500; Labour ` 1,300, and Overhead ` 164. The normal waste is 5% of input., (a) 40 units are transferred to next process @ ` 70 each, (b) 40 units are transferred to next process @ ` 74.10 each, (c) 38 units are transferred to next process @ ` 78 each, (d) 40 units are transferred to next process @ ` 78 each, 22. Particulars for Process A., Materials (200 Units) ` 4,000, Labour ` 3,000, Indirect Expenses ` 2,000, Normal wastage is 5% of the input. One unit of wastage is sold at ` 16.50 each., (a) 190 units are transferred to next process at ` 9,000, (b) 200 units are transferred to next process at ` 9,000

Page 15 :

Manan Prakashan, , 15, , (c) 190 units are transferred to next process at ` 7,000, (d) 190 units are transferred to next process at ` 8,835, 23. In process Y, 75 units of a commodity were transferred from process X at a cost of ` 1,310. The, labour and overhead expenses incurred by the process were ` 190. 20% of the units entered are, normally lost and sold @ ` 4 per unit. The output of the process was 70 units., (a) Process Account Credit Side showed Abnormal Gains of ` 240, (b) Process Account Debit Side showed Abnormal Loss of ` 240, (c) Process Account Credit Side showed Abnormal Loss of ` 240, (d) Process Account Debit Side showed Abnormal Gains of ` 240, 24. Input in a process is 4000 units and normal loss is 20%. When finished output in the process is, only 3,240 units, there is an, (a) Abnormal loss of 40 units, (b) Abnormal gain of 40 units, (c) Neither abnormal loss nor gain, (d) Abnormal loss of 60 units, 25. Details of the process for the last period are as follows :, Put into process, 5,000 kg, Materials, ` 2,500, Labour, ` 700, Production Overheads, 200% of labour, Normal losses are 10% of input in the process. The output for the period was 4,200 kg from the, process. There was no opening and closing work-in-process. What were the units of abnormal, loss ?, (a) 500 units, (b) 300 units, (c) 200 units, (d) 100 units, 26. You are required to identify how many good units were outputs from the process., Units, Units put in process, 4,000, Lost units, 500, Units in process, 200, (a) 3,300 units, (b) 4,000 units, (c) 4,200 units, (d) 4,500 units, 27. A chemical process has normal wastage of 10% of input. In a period, 2,500 kg of material were, input and there was abnormal loss of 75 kg. What quantity of good production was achieved ?, (a) 2,175 kg, (b) 2,250 kg, (c) 2,425 kg, (d) 2,500 kg, , II., , JOINT PRODUCTS / BY-PRODUCTS, , A., , Conceptual, , 28. Costs incurred prior to the point of separation of the joint or by-products are termed as, (a) Process cost, (b) Joint cost, (c) Main cost, (d) Separable cost, 29. When a single manufacturing process yields two products, one of which has a relatively high, sales value compared to the other, the two products are respectively known as, (a) joint products and byproducts, (b) joint products and scrap, (c) main products and byproducts, (d) main products and joint products, 30. A process gives rise, incidentally, to an item of low value, which is called, (a) a joint product, (b) a by-product, (c) scrap, (d) waste, 31. Byproducts and main products are differentiated by, (a) number of units per processing period, (b) weight or volume of outputs per period, (c) the amount of sales value per unit, (d) none of the above, 32. A Petroleum company assigns certain value based on the calorific value to each petroleum, product, and these values become the basis of apportionment of joint cost among petroleum, products. This is an example of (a) Average Unit Cost Method, (b) Physical Unit Method, (c) Survey method, (d) None of the above

Page 16 :

16, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 33. Under this method of allocation of joint costs, even high quality items may have a lower price, (a) Contribution Margin Method, (b) Survey method, (c) Average Unit Cost Method, (d) None of the above, 34. This is also known as ‘Weighted Average Cost Method’., (a) Contribution Margin Method, (b) Survey method, (c) Net Realizable Value Method, (d) None of the above, 35. Under this method of allocation of joint costs, higher-priced items are charged more costs (a) Contribution Margin Method, (b) Market Value Method, (c) Average Unit Cost Method, (d) None of the above, 36. This method of allocation of joint costs is useful when the products are not saleable at the spiltoff stage without further processing, (a) Market value at the point of separation, (b) Net Realizable Value, (c) Market value at finished stage, (d) None of the above, 37. For the purpose of allocating joint costs to joint products, the sale price at point of sale, reduced, by costs to complete after split-off, is assumed to be equal to (a) Joint Costs, (b) Total Costs, (c) Net Sales Value at split-off, (d) Sale price Less normal profit margin at point of sale, 38. Joint Costs are normally allocated on the basis of relative, (a) Profitability, (b) Sales Value, (c) Direct Labour Hours, (d) Direct Machine Hours, 39. Net Realizable Value is defined as, (a) Sales value at split-off point, (b) Sales price minus fixed costs, (c) Sales price minus joint costs, (d) Sales price minus costs to complete the product, 40. Joint Cost are allocated according to sales value of individual products under (a) Market Value Method, (b) Average Unit Cost Method, (c) Survey Method, (d) Physical Unit Method, of individual, 41. Under the Market Value Method, Joint Costs are allocated according to, products, (a) Cost Price, (b) Market price or cost price whichever is less, (c) Sales Value, (d) Cost and Demand Price, 42. Under the Average Unit Cost Method of apportionment of joint costs, the cost per unit of each, product is, (a) Constant, (b) Different, (c) Same, (d) Semi-Variable, 43. All costs incurred beyond the splitoff point that are assignable to one or more individual products, are called, (a) byproduct costs, (b) joint costs, (c) main costs, (d) separable costs, , B., , Numerical, , 44-45 : Three products A, B and C are obtained from a process. The following details are providedParticulars, A, B, C, Sales (kg.), 500, 400, 100, Selling price per kg., 25, 22, 37, Joint costs are ` 90,000, 44. The amount of joint costs allocated to product B on Sales Value method will be (a) ` 45,000, (b) ` 31,680, (c) ` 25,720, (d) ` 13,320, 45. The amount of joint costs allocated to product C on Physical Unit method will be (a) ` 45,000, (b) ` 36,000, (c) ` 18,000, (d) ` 9,000

Page 17 :

Manan Prakashan, , 17, , ANSWERS, 1., 2., 3., 4., 5., 6., 7., , (c), (d), (c), (d), (a), (c), (b), , 8., 9., 10., 11., 12., 13., 14., , (a), (c), (a), (b), (b), (a), (b), , 15., 16., 17., 18., 19., 20., 21., , (a), (a), (c), (d), (b), (a), (c), , 22., 23., 24., 25., 26., 27., 28., , (d), (d), (b), (b), (a), (a), (b), , 29., 30., 31., 32., 33., 34., 35., , (c), (b), (c), (b), (c), (b), (b), , Hints :, 16. [(12,000 x 0.9) - 10,920 = 120 (gain because actual > expected)], 17. [(1.0 x 0.8) = 1.25], 18. [(400 litres x 0.7) = 571.4 (571 litres)], 19. [22,040 / 1,900], 20. [400 + 3,400 - 400 - 200], 23. [1,440 / 60 x 10], 44. [90,000 x 8,800 / 25,000 = 31,680], 45. [90,000 x 100 / 1,000 = 9,000], , 36., 37., 38., 39., 40., 41., 42., , (c), (c), (b), (d), (a), (c), (c), , 43., 44., 45., , (d), (b), (d)

Page 18 :

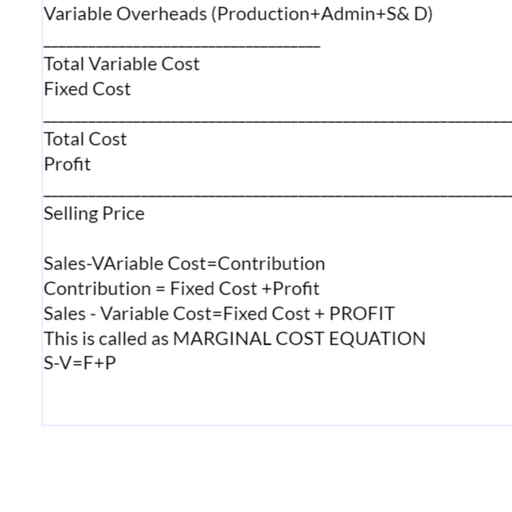

18, , Cost Accounting (T.Y.B.Com.: SEM-VI), , CHAPTER - 4 : INTRODUCTION TO MARGINAL COSTING, MULTIPLE CHOICE QUESTIONS, A., , Conceptual, , 1. What distinguishes absorption costing from marginal costing?, (a) Product costs include both prime cost and production overhead, (b) Product costs include both production and non-production costs, (c) Stock valuation includes a share of all production costs, (d) Stock valuation includes a share of all costs, 2. The Marginal Cost Statement, (a) shows the gross profit, (b) is sent to the shareholders, (c) shows classification of costs as direct and indirect, (d) can be used to predict future profits at different levels of activity, 3. CVP analysis requires costs to be categorized as, (a) fixed or variable, (b) direct or indirect, (c) product or period, (d) standard or actual, 4. Contribution equals :, (a) Sales minus cost of sales, (b) Sales minus cost of production, (c) Sales minus variable costs, (d) Sales minus fixed costs, 5. Contribution is equal to, (a) Fixed cost + profit, (b) Sales - variable cost, (c) Fixed cost - loss, (d) All the above, 6. Which of the following costs is not deducted from sales revenue in computation of contribution?, (a) Direct materials, (b) Direct labour, (c) Fixed factory overheads, (d) Variable selling overheads, 7. The selling price per unit less the variable cost per unit is the :, (a) Fixed cost per unit, (b) Gross profit per unit, (c) Operating profit per unit, (d) Contribution per unit, 8. If contribution margin increases by ` 2 per unit, then operating profits will, (a) also increase by ` 2 per unit, (b) increase by less than ` 2 per unit, (c) decrease by ` 2 per unit, (d) cannot say, 9. P/V ratio is equal to, (a) Profit/volume, (b) Contribution/sales, (c) Profit/contribution, (d) Profit/sales, 10. Profit - volume ratio is improved by reducing, (a) Variable cost, (b) Fixed cost, (c) Both of them, (d) None of them, 11. At the break-even point, which equation will be true., (a) Variable cost - fixed cost = contribution (b) Sales = variable cost + fixed cost, (c) Sales - fixed cost = contribution, (d) Sales - contribution = variable cost, 12. The break even points in units is equal to, (a) Fixed cost/PV ratio, (b) Fixed cost x sales/total contribution, (c) Fixed cost/contribution per unit, (d) Fixed cost/total contribution, 13. When fixed cost increases, the break even point, (a) Increases, (b) Decreases, (c) No effect, (d) Can’t say, 14. When variable cost decreases, then break even point, (a) Increases, (b) Decreases, (c) No effect, (d) Can’t say

Page 19 :

Manan Prakashan, , 19, , 15. When selling price decreases, then break even point, (a) Increases, (b) Decreases, (c) No effect, (d) Can’t say, 16. When sales increases then break even point, (a) Increases, (b) Decreases, (c) Remains constant, (d) None of these, 17. Which of the following can improve break-even point?, (a) Increase in variable cost, (b) Increase in fixed cost, (c) Increase in sale price, (d) Increase in sales volume, (e) Increase in production volume, 18. Which of the following describes the margin of safety?, (a) actual contribution margin achieved compared with that required to break-even, (b) actual sales compared with sales required to break-even, (c) actual versus budgeted net profit margin, (d) actual versus budgeted sales, 19. Margin of safety is expressed as, (a) Profit / P/V ratio, (b) (Actual sales - sales at BEP ) / Actual sales, (c) Actual sales - Sales at BEP, (d) All of the above, 20. Under which of the following cases the margin of safety decreases?, (a) Reduction in fixed cost, (b) Increase in variable cost, (c) Increase in the level of production or selling price or both, (d) Change in the sales mix in order to increase the contribution, (e) Substitute the existing unprofitable product with the profitable ones, 21. In the break-even chart, the margin of safety point lies, (a) To the left of break even point, (b) To the right of break even point, (c) On break even point, (d) Can’t say, 22. Fixed cost is equal to, (a) Break-even sales x Margin of safety, (b) Sales x Margin of safety, (c) Sales x Profit-volume ratio, (d) Profit-volume ratio x Break even sales, 23. Which of the following factors is to be multiplied with contribution margin ratio to calculate profit?, (a) Unit contribution margin, (b) Margin of safety, (c) Variable costs per unit, (d) Unit sales price, (e) Change in sales volume, 24. In cost-volume-profit analysis, profit is equal to, (a) Sales Revenue x P/V ratio - Fixed Cost (b) Sales units x contribution per unit - fixed costs, (c) Total contribution - Fixed cost, (d) All the above, 25. The sales volume in value required to earn the target profit, the formula is, (a) Target profit / Contribution per unit, (b) (Fixed cost + Target profit) x P/V ratio, (c) (Fixed cost + Target profit) / Contribution on per unit, (d) (Fixed cost + Target profit) / PV ratio, 26. There is a reduction in the selling price. This will, other factors remaining same (a) increase contribution margin, (b) reduce fixed costs, (c) increase variable costs, (d) reduce operating income, 27. There is an increase in advertising expenses. This will, other factors remaining same (a) reduce operating income, (b) reduce contribution, (c) decrease selling price, (d) increase variable costs, 28. Cost-volume-profit analysis is used PRIMARILY by management :, (a) as a planning tool, (b) for control purposes, (c) to prepare external financial statements (d) for correct financial results

Page 20 :

20, B., , Cost Accounting (T.Y.B.Com.: SEM-VI), Numerical, , 29. The contribution to sales ratio of a company is 20% and profit is ` 64,500. If the total sales of the, company are ` 7,80,000, the fixed cost is, (a) ` 1,56,000, (b) ` 1,21,500, (c) ` 1,05,600, (d) ` 91,500, (e) ` 90,000, 30. The total cost of manufacturing 4,000 units of a product is ` 4,50,000 which includes fixed costs, of ` 2,50,000. If the company desires to produce 5,000 units, then the total cost will be(a) ` 5,27,778, (b) ` 5,20,000, (c) ` 5,00,000, (d) ` 4,95,000, (e) ` 4,83,500, 31. The total cost of manufacturing 3,600 units of Product X is ` 81,000 which includes variable cost, per unit of ` 15.00. If the company desires to produce 3,850 units, then the total cost would be, (a) ` 86,625, (b) ` 84,750, (c) ` 57,750, (d) ` 52,250, (e) ` 50,700, 32. P Limited incurs fixed costs of ` 1,00,000 per annum. The company manufactures a single, product and sells it for ` 50 per unit. If the contribution to sales ratio is 40%, the break-even, sales in units are, (a) 5,000, (b) 6,000, (c) 6,500, (d) 7,000, (e) 7,500.00, 33. A company manufactures a single product with a variable cost per unit of ` 22. The contribution, to sales ratio is 45%. Monthly fixed costs are ` 1,98,000. What is the breakeven point in units?, (a) 4,950, (b) 9,000, (c) 11,000, (d) 20,000, 34. A Ltd. manufactures and sells product ‘B’. The sale price per unit of the product is ` 35. The, company will incur a loss of ` 5.00 per unit if it sells 4,000 units; but if the volume is raised to, 12,000 units, the company will make a profit of ` 4.50 per unit. The break-even point in units is, (a) 5,700, (b) 6,612, (c) 5,250, (d) 6,162, 35. The profit-volume ratio and margin of safety ratio are 30% and 40% respectively. If the total, sales is ` 3,00,000, the profit of the firm is, (a) ` 54,000, (b) ` 48,000, (c) ` 36,000, (d) ` 30,000, (e) ` 25,000, 36. A company manufactures a single product which it sells for ` 15 per unit. The product has a, contribution to sales ratio of 40%. The company’s weekly break-even point is sales of ` 18,000., What would be the profit in a week when 1,500 units are sold?, (a) ` 900, (b) ` 1,800, (c) ` 2,700, (d) ` 4,500, 37. An organisation manufactures a single product. The total cost of making 4,000 units is ` 20,000, and the total cost of making 20,000 units is ` 40,000. Within this range of activity the total fixed, costs remain unchanged. What is the variable cost per unit of the product?, (a) ` 0.80, (b) ` 1.20, (c) ` 1.25, (d) ` 2.00, 38. 5,400 units of a company’s single product were sold for a total revenue of ` 1,40,400. Fixed, costs in the period were ` 39,420 and net profit was ` 11,880. What was the contribution per, unit?, (a) ` 7.30, (b) ` 9.50, (c) ` 16.50, (d) ` 18.70, 39. Sales are ` 3,20,000, fixed costs are ` 80,000 and variable costs are ` 1,20,000. What is the, safety margin?, (a) ` 18,900, (b) ` 20,000, (c) ` 1,92,000, (d) ` 1,28,000, (e) ` 1,31,000

Page 21 :

Manan Prakashan, , 21, , 40. An organisation manufactures a single product which has a variable cost of ` 36 per unit. The, organisation’s total weekly fixed costs are ` 81,000 and it has a contribution to sales ratio of, 40%. This week it plans to manufacture and sell 5,000 units. What is the organisation’s margin, of safety in units?, (a) 1,625, (b) 2,750, (c) 3,375, (d) 3,500, 41. An organization’s break-even point is 4,000 units at a sales price of ` 50 per unit, variable cost, of ` 30 per unit, and total fixed costs of ` 80,000. If the company sells 500 additional units, by, how much will its profit increase ?, (a) ` 25,000, (b) ` 15,000, (c) ` 12,000, (d) ` 37,000, (e) ` 10,000, 42. Banta Ltd. manufactures product KDM for last ten years. The company maintains a margin of, safety of 36% with an overall contribution to sales ratio of 35%. If fixed cost is ` 8.4 lakh, the, profit of the company is, (a) ` 11.400 lakh, (b) ` 24.000 lakh, (c) ` 4.725 lakh, (d) ` 37.500 lakh, (e) ` 8.644 lakh, 43. A company wishes to make a profit of ` 1,50,000. It has fixed costs of ` 75,000 with a C/S ratio, of 0.75 and a selling price of ` 10 per unit. How many units would the company need to sell in, order to achieve the required level of profit?, (a) 10,000 units, (b) 15,000 units, (c) 22,500 units, (d) 30,000 units, 44. A company has a profit-volume ratio of 20%. To maintain the same contribution, by what, percentage (%) must sales be increased to offset 10% reduction in selling price?, (a) 10, (b) 20, (c) 100, (d) 50, (e) 80, 45. The following data is obtained from the records of the Plum Ltd.:, Particulars, First year (`), Second year (`), Sales, 1,28,000, 1,44,000, Profit, 16,000, 22,400, The break-even sales of the company in rupees is, (a) ` 1,36,000, (b) ` 1,30,000, (c) ` 1,00,000, (d) ` 88,000, (e) ` 90,000, , ANSWERS, 1., 2., 3., 4., 5., 6., 7., , (c), (d), (a), (c), (d), (c), (d), , 8., 9., 10., 11., 12., 13., 14., , (a), (b), (a), (b), (c), (a), (b), , 15., 16., 17., 18., 19., 20., 21., , (a), (c), (c), (b), (d), (b), (c), , Hints :, 29. [(7,80,000 x 20%) – 64,500], 30. [2,50,000 + (5,000 x 50)], 31. [(3,850 x ` 15) + ` 27,000], 32. [1,00,000 / (50 x 40%)], 33. [1,98,000 / ( 22 ÷ 0.55 x 0.45)], 34. [` 57,000 / (` 35 - ` 25.75)], 35. [40% x 3,00,000 x 30%], 36. {(1,500 - [18,000 / 15)] x (15 x 40%)}, , 22., 23., 24., 25., 26., 27., 28., , (d), (b), (d), (d), (d), (a), (a), , 29., 30., 31., 32., 33., 34., 35., , (d), (c), (b), (a), (c), (d), (c), , 36., 37., 38., 39., 40., 41., 42., , (b), (c), (b), (c), (a), (e), (c), , 43., 44., 45., , (d), (e), (d)

Page 22 :

22, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 37. [` (40,000 - 20,000) ÷ (20,000 - 4,000) units = ` 1.25 per unit], 38. [(` 39,420 + ` 11,880) ÷ 5,400 units], 39. [` 3,20,000 - ` 1,28,000], 40. [(CPU) = (36 ÷ 0.60) x 0.40 = ` 24; BEP (81,000 ÷ 24) = 3,375 units; MOS (5,000 - 3,375) = 1,625, units], 41. [500 x (50 - 30)], 42. [36% x (24 / 64%) x 35%], 43. {[(1,50,000 + 75,000) / 0.75] / 10}, 44. [(` 20 ÷ ` 0.10) x ` 0.90 Less 100], 45. [35,200 / 0.40]

Page 23 :

Manan Prakashan, , 23, , CHAPTER - 5 : INTRODUCTION TO STANDARD COSTING, MULTIPLE CHOICE QUESTIONS, A., , Conceptual, , 1. The objective of standard costing is to, (a) Determine profitability of a product, (b) Determine break-even production level, (c) Control costs, (d) Allocate costs with more accuracy, 2. A standard cost system may be used in, (a) job order costing, but not process costing (b) process costing, but not job order costing, (c) either job order costing or process costing (d) neither job order costing nor process costing, 3. An estimate of what cost should be is known as, (a) Actual cost, (b) Ideal cost, (c) Standard cost, (d) Forecast cost, 4. A standard cost is, (a) the total amount that appears on the budget for product costs, (b) a pre-determined cost which is calculated from management’s standards of efficient operation, (c) the total number of units x the cost expected, (d) any amount that appears on a budget, 5. Which of the following best describes a basic standard?, (a) A standard set at an ideal level, which makes no allowance for normal losses, waste and, machine downtime, (b) A standard which assumes an efficient level of operation, but which includes allowances for, factors such as normal loss, waste and machine downtime, (c) A standard which is kept unchanged over a long period of time, (d) A standard which is based on current price levels, 6. A standard which assumes efficient level of operations, but which includes allowance for factors, such as waste and machine downtime is known as an, (a) Ideal standard, (b) Normal standard, (c) Attainable standard, (d) Neither (a) nor (b) nor (c), 7. What standard is based on the assumption of most favourable conditions possible ?, (a) Ideal Standard, (b) Normal Standard, (c) Expected Standard, (d) Attainable Standard, 8. The standard cost card contains quantities and costs for, (a) direct material only, (b) direct labour only, (c) direct material and direct labour only, (d) direct material, direct labour, and overhead, 9. Which one of the following does NOT accurately describe one of the ways in which standards, are developed?, (a) Standard material quantities may be determined by engineering studies, (b) Supplier price lists may be used to determine standard prices of materials, (c) Time and motion studies are sometimes used to determine labour efficiency standards, (d) Employee time cards are often used to determine standard labour wage rates, 10. What term can be defined as a means of assessing the difference between a predetermined, amount and the actual amount?, (a) Variance analysis, (b) Differential costing, (c) Incremental costing, (d) Marginal Costing, 11. A total cost variance is best defined as the difference between, (a) total standard cost for the last year and total standard cost in the current year, (b) total standard cost for the last year and total actual cost in the current year, (c) the standard cost value of output budgeted in a period and the total actual cost incurred, (d) the standard cost value of output achieved in a period and the total actual cost incurred

Page 24 :

24, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 12. If standard cost is lower than the actual cost, the difference is known as, (a) Favourable, (b) Adverse, (c) Positive, (d) Negative, 13. A favourable variance occurs when, (a) actual costs are less than marginal costs (b) standard costs are less than actual costs, (c) actual costs are less than the selling price(d) actual costs are less than standard costs, 14. The “standard quantity allowed” is computed by multiplying the :, (a) actual input in units by the standard output allowed, (b) actual output in units by the standard input allowed, (c) actual output in units by the standard output allowed, (d) standard output in units by the standard input allowed, 15. The difference between the actual price and the standard price, multiplied by the actual quantity, of materials purchased is the, (a) materials cost variance, (b) materials usage variance, (c) materials price variance, (d) materials efficiency variance, 16. The difference between the actual quantity and the standard quantity, multiplied by the standard, price is the, (a) materials efficiency variance, (b) materials volume variance, (c) materials price variance, (d) materials usage variance, 17. Which of the following is correct with regard to using the standard quantity to compute materials, variances?, Standard quantity is used (a) Materials Price Variance: Yes; Materials Usage Variance: No, (b) Materials Price Variance: Yes; Materials Usage Variance: Yes, (c) Materials Price Variance: No; Materials Usage Variance: No, (d) Materials Price Variance: No; Materials Usage Variance: Yes, 18. Which of the following is correct with regard to using the standard unit price to compute materials, variances?, Standard unit price used:, (a) Materials Price Variance: Yes; Materials Usage Variance: No, (b) Materials Price Variance: Yes; Materials Usage Variance: Yes, (c) Materials Price Variance: No; Materials Usage Variance: No, (d) Materials Price Variance: No; Materials Usage Variance: Yes, 19. The term “standard hours allowed” measures, (a) budgeted output at actual hours, (b) budgeted output at standard hours, (c) actual output at standard hours, (d) actual output at actual hours, 20. The labour rate variance is computed as :, (a) (Actual labour hours worked – Standard labour hours allowed) x Actual labour rate, (b) (Actual labour hours worked – Standard labour hours allowed) x Standard labour rate, (c) (Actual labour rate – Standard labour rate) x Standard hours allowed, (d) (Actual labour rate – Standard labour rate) x Actual hours worked, 21. If the actual number of labour hours worked is less than the standard labour hours allowed for, equivalent units produced, this indicates :, (a) An unfavourable labour rate variance, (b) A favourable total labour variance, (c) An unfavourable labour efficiency variance, (d) A favourable labour efficiency variance, 22. Which of the following is correct with regard to the standard labour hours being used to compute, labour variances ?, Standard labour hours used :, (a) Labour Rate Variance: Yes; Labour Efficiency Variance: No, (b) Labour Rate Variance: Yes; Labour Efficiency Variance: Yes, (c) Labour Rate Variance: No; Labour Efficiency Variance: No, (d) Labour Rate Variance: No; Labour Efficiency Variance: Yes

Page 25 :

Manan Prakashan, , 25, , 23. Which of the following is correct with regard to using the standard labour rate to compute labour, variances?, Standard labour rate used:, (a) Labour Rate Variance: Yes; Labour Efficiency Variance: No, (b) Labour Rate Variance: Yes; Labour Efficiency Variance: Yes, (c) Labour Rate Variance: No; Labour Efficiency Variance: No, (d) Labour Rate Variance: No; Labour Efficiency Variance: Yes, 24. What is the primary benefit of a standard costing system?, (a) It records costs at what should have been incurred, (b) It allows for a comparison of differences between actual and standard costs, (c) It is easy to implement, (d) It is inexpensive and easy to use, 25. The standard which can be attained under the most favourable conditions possible, (a) Ideal Standard, (b) Expected Standard, (c) Current Standard, (d) Normal Standard, 26. A standard which is established for use unaltered for an indefinite period is called, (a) Current standard, (b) Ideal standard, (c) Basic standard, (d) Expected standards, 27. Which of the following is not a type of standard, conceptually speaking ?, (a) Ideal standards, (b) Negative standards, (c) Expected standards, (d) Current standards, 28. Which of the following statements about ideal standards is false ?, (a) It is called theoretical or maximum efficiency standard, (b) These are standard costs that are set for production under optimal condition, (c) It makes no allowance for wastage, spoilage and machine breakdowns, (d) It can be used for cash budgeting or product costing, 29. The cost of product as determined under standard cost system is, (a) Fixed cost, (b) Historical cost, (c) Direct cost, (d) Predetermined cost, 30. The amount of work achievable in an hour, at standard efficiency levels, is, (a) an ideal standard, (b) the direct labour usage per hour, (c) a standard hour, (d) the direct labour efficiency variance, 31. While computing variances from standard costs, the difference between the actual and the, standard prices multiplied by the actual quantity yields a, (a) Yield variance, (b) Volume variance, (c) Mix variance, (d) Price variance, 32. While evaluating deviations of actual cost from standard cost, the technique used is, (a) Regression analysis, (b) Variance analysis, (c) Linear progression, (d) Trend analysis, 33. Which of the following statements is / are true ?, (i) The standard cost per unit of materials is used to calculate a materials price variance, (ii) The standard cost per unit of materials is used to calculate a materials usage variance, (iii) The standard cost per unit of materials cannot be determined until the end of the period, (a) Only (i) above, (b) Only (ii) above, (c) Only (iii) above, (d) Both (i) and (ii) above, 34. The labour cost variance may be expressed as, (a) Budgeted labour cost – Actual labour cost, (b) (Standard wage rage x Output achieved) – Actual wage cost, (c) (Standard hours – Actual hours) x Actual wage rate, (d) (Standard hours – Actual hours) x Standard wage rate

Page 26 :

26, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 35. Which of the following statements is / are true ?, (i) The standard direct labour hours per unit of output is used to calculate a labour rate variance, (ii) The standard direct labour hours per unit of output is used to calculate a labour efficiency, variance, (iii) The standard direct labour hours per unit of output cannot be determined until the end of the, period, (a) Only (i) above, (b) Only (ii) above, (c) Only (iii) above, (d) Both (i) and (ii) above, 36. Which of the following is a purpose of standard costing ?, (a) To determine profit at different levels, (b) To determine break even production level, (c) To control costs, (d) To allocate cost with more accuracy, 37. Which of the following best describes a basic standard?, (a) A standard set at an ideal level, which makes no allowance for normal losses, waste and, machine downtime., (b) A standard which assumes an efficient level of operation, but which includes allowances for, factors such as normal loss, waste and machine downtime., (c) A standard which is kept unchanged over a period of time., (d) A standard which is based on current price levels., , B., , Numerical MCQs / Short Practical Problems / Case Studies, , 38. Actual units of direct materials used were 20,000 at an actual cost of ` 40,000. Standard unit, cost is ` 2.10. Assuming the materials price variance is recognized when the materials are used,, the materials price variance (MPV) is:, (a) ` 1,000 favourable, (b) ` 1,000 unfavourable, (c) ` 2,000 favourable, (d) ` 2,000 unfavourable, 39. If material cost variance is ` 9,400 (favourable) and material usage variance is ` 8,200 (adverse),, then material price variance (MPV) is, (a) ` 5,600 (favourable), (b) ` 5,600 (adverse), (c) ` 6,400 (favourable), (d) ` 17,600 (adverse), (e) ` 17,600 (favourable), 40. The actual materials price (AP) was ` 3.50, the actual quantity (AQ) of material was 5,100 units,, and the materials price variance (MPV) was ` 1,275 unfavourable. The standard materials price, (SP) was :, (a) ` 3.75, (b) ` 3.30, (c) ` 3.00, (d) ` 3.25, 41. During the month of December 2013, XLNT Ltd. used 5,000 kgs of materials at a total standard, cost of ` 20,000. The material usage variance was ` 360 (adverse). The standard usage of, material (SQ) for the period is, (a) 4,000 kgs, (b) 4,910 kgs, (c) 5,000 kgs, (d) 5,850 kgs, (e) 6,340 kgs, 42. The standard units (SQ) were 5,200, the standard price (SP) was ` 3.25, and the materials, quantity variance (MQV) was ` 325 favourable. The actual units (AQ) were:, (a) 5,300, (b) 5,000, (c) 5,100, (d) 5,200, 43. Last month 27,000 direct labour hours were worked at an actual cost of ` 2,36,385 and the, standard direct labour hours of production were 29,880. The standard direct labour cost per, hour was ` 8.50. What was the labour efficiency variance (LEV) ?, (a) ` 17,595 Adverse, (b) ` 17,595 Favourable, (c) ` 24,480 Adverse, (d) ` 24,480 Favourable, 44. Consider the following data pertaining to Roy Ltd. for the month of June 2014 :, Actual direct labour hours - 27,600, Standard direct labour hours - 28,000, Total direct labour cost (`) - 1,93,200

Page 27 :

Manan Prakashan, , 27, , If direct labour efficiency variance is ` 2,560 (favourable), the direct labour rate variance (LRV), is, (a) ` 12,252 (adverse), (b) ` 15,560 (adverse), (c) ` 15,560 (favourable), (d) ` 16,560 (adverse), (e) ` 16,560 (favourable), 45. The standard hourly rate was ` 1.40. The actual rate was ` 1.30. The labour rate variance was, ` 600, favourable. The actual labour hours (AH) were:, (a) 6,000, (b) 6,400, (c) 1,000, (d) 1,500, 46. A Ltd. used 4,538 kgs of material at a standard cost of ` 2.50 per kg. The material usage variance, was ` 280 (Favourable). The standard usage of material for the period is, (a) 4,700 kgs, (b) 4,650 kgs, (c) 4,600 kgs, (d) 4,588 kgs, 47. R Ltd. a manufacturer of portable radios, purchases the components from subcontractors and, assembles them into a complete radio. Each radio requires three units each of part X which has, standard cost of ` 145 per unit., Following is the result pertaining to part X for the month of December 2010 :, Particulars, Units, Purchases (` 18,00,000), 12,000, Consumed in manufacturing, 10,000, Radios manufactured, 3,000, The material usage variance for the month of December 2010 is, (a) `1,45,000 unfavourable, (b) ` 1,45,000 favourable, (c) ` 4,35,000 unfavourable, (d) ` 4,35,000 favourable, 48. X Ltd. has furnished the following data for the month of March 2010 :, Particulars, Standard, Actual, Material cost per kg (`), 70, 72, Material used (Kgs), 3,500, 3,420, The material price variance is, (a) ` 7,000 (Adverse), (b) ` 7,000 (Favourable), (c) ` 6,840 (Adverse), (d) ` 6,840 (Favourable), 49. During the month of September 2010, 7,800 kg. of material was purchased at a total cost of, ` 16,380. The stocks of material increased by 440 kg. It is the company's policy to value the, stocks at standard purchase price. If the material price variance was ` 1,170 (Adverse), the, standard price per kg. of material is, (a) ` 1.95, (b) ` 2.10, (c) ` 2.23, (d) ` 2.25, 50. The standard and the actual requirements of material of a company are as under :, Standard - 2,400 units at the rate of ` 20 per unit, Actual - 2,600 units at the rate of ` 19 per unit, The material cost variance is, (a) ` 2,600 (Adverse), (b) ` 1,400 (Favourable), (c) ` 2,400 (Adverse), (d) ` 1,400 (Adverse), 51. Last month 27,000 direct labour hours were worked at an actual cost of ` 2,36,385 and the, standard direct labour hours of production were 29,880. The standard direct labour cost per, hour was ` 8.50., What was the labour efficiency variance?, (a) ` 17,595 Adverse, (b) ` 17,595 Favourable, (c) ` 24,480 Adverse, (d) ` 24,480 Favourable, 52. In the four week production period just completed, B Ltd. produced 570 units. The standard, labour cost for each unit was ` 13.50, based on budgeted production of 550 units. The actual, labour cost for the period was ` 8,238., What was the labour rate variance for the period?, (a) ` 543 adverse, (b) ` 543 favourable, (c) ` 813 adverse, (d) ` 813 favourable

Page 28 :

28, , Cost Accounting (T.Y.B.Com.: SEM-VI), , 53. During a period, 17,500 labour hours were worked at a standard cost of ` 6.50 per hour. If the, labour efficiency variance is ` 7,800 (favourable), the standard direct labour hours are, (a) 20,000, (b) 19,200, (c) 18,700, (d) 18,500, , ANSWERS, 1., 2., 3., 4., 5., 6., 7., 8., , (a), (c), (b), (d), (d), (c), (a), (d), , 9., 10., 11., 12., 13., 14., 15., 16., , (d), (a), (d), (b), (d), (b), (c), (d), , 17., 18., 19., 20., 21., 22., 23., 24., , (d), (b), (c), (d), (d), (d), (b), (b), , 25., 26., 27., 28., 29., 30., 31., 32., , (a), (c), (b), (d), (d), (c), (d), (b), , 33., 34., 35., 36., 37., 38., 39., 40., , (d), (b), (b), (c), (c), (c), (e), (d), , 41., 42., 43., 44., 45., 46., 47., 48., , (b), (c), (d), (d), (a), (b), (a), (c), , Hints :, 17. SQ is not used for computing MPV, 18. SP is used in computing both MPV and MQV, 22. SH is used in computing LEV but not in LRV, 23. SR is used in computing both LRV and LEV, 38. [20,000 x (2.00 – 2.10)], 39. [` 9,400 + ` 8,200], 40. [3.50 - (1,275 / 5,100)], 41. [5,000 - (360/4)], 42. [5,200 - (325 / 3.25)], 43. [2,53,980 - (27,000 x 8.50) F], 44. [(` 7.00 - ` 6.40) x 27,600 hours], 45. [600 / 0.10], ⎛ 280 ⎞, ⎟ = 4,650, 46. 4,538 + ⎜, ⎝ 2.50 ⎠, 47. 145 x [10,000 – (3,000 x 3)] = 1,45,000 (A), , 48. 3,420 x (72 – 70) = 6,840 (A), , 16,380 − 1,170, = 1.95, 7,800, 50. (2,600 x 19) – (2,400 x 20) = 1,400 (A), 51. Actual hours at standard rate (27,000 x 8.50), Standard hours of production at standard rate, ∴ Labour efficiency variance is (Favourable), 53. 7,800 (F) = 6.50 x (17,500 – SH), 49., , ∴ SH = 17,500 +, , 7,800, = 18,700, 6.50, , 2,29,500, 2,53,980, 24,480, , 49., 50., 51., 52., 53., , (a), (d), (d), (a), (c)

Page 29 :

Manan Prakashan, , 29, , CHAPTER - 6 : SOME EMERGING CONCEPTS, OF COST ACCOUNTING, MULTIPLE CHOICE QUESTIONS, A., , Target Costing, , 1. Place the following steps for the implementation of target costing in order :, A = Derive a target cost, B = Develop a target price, C = Perform value engineering, D = Determine target profit, (a) B, D, A, C, (b) B, A, D, C, (c) A, D, B, C, (d) A, B, C, D, 2. In target costing, (a) the target cost is established first, then the target price., (b) the target cost is the estimated long-run cost that enables a product or service to achieve a, desired profit, (c) the focus of target costing is to undercut the competition, (d) target costs are generally higher than current costs, 3. The product strategy in which companies first determine the price at which they can sell a new, product and then design a product that can be produced at a low enough cost to provide adequate, operating income is referred to as, (a) Cost-plus pricing, (b) Target costing, (c) Benchmark costing, (d) Full costing, 4. The costing technique that produces a stipulated profit when a product is sold at its estimated, market-driven price is termed:, (a) Life cycle costing, (b) Product costing, (c) Target costing, (d) Standard costing, 5. The four tasks that follow take place in the concept known as target costing:, (1) Value engineering, (2) Establish a target selling price, (3) Establish a target cost, (4) Establish a target profit, Which is the correct sequence of these tasks?, (a) 1, 3, 4, 2, (b) 3, 1, 4, 2, (c) 2, 4, 3, 1, (d) 2, 3, 1, 4, 6. R uses target costing and sells a product for ` 36 per unit. The company seeks a profit margin, equal to 25% of sales. If the current manufacturing cost is ` 29 per unit, the firm will need to, implement a cost reduction of, (a) ` 0, (b) ` 2, (d) ` 20, (c) ` 9, 7. S Corporation uses target costing and sells a product for ` 40 per unit. The company seeks a, profit margin equal to 30% of sales. If target-costing calculations revealed a need for a ` 4 cost, reduction, the firm’s current manufacturing cost must be:, (a) ` 12, (b) ` 24, (d) ` 32, (c) ` 28, 8. Which of the following denotes a target cost?, (a) Market price - Desired profit margin, (b) Standard selling price - Standard profit margin, (c) Standard selling price - Target profit margin

Page 30 :

30, , Cost Accounting (T.Y.B.Com.: SEM-VI), , (d) Desired selling price - Desired profit margin, (e) Market price - Return on Investment (ROI), 9. Which of the following is true with respect to target costing?, (a) It is a method of price determination, (b) It is used to develop a short run price, (c) It is a process where the cost of the product is determined and then an appropriate price is, chosen, (d) It is the maximum manufacturing cost for a product which is arrived at by subtracting the, acceptable profit margin from the expected market price, , B., , Life Cycle Costing, , 10. Which of the following is usually the longest stage in the product life cycle?, (a) Introduction phase, (b) Growth phase, (c) Maturity phase, (d) Saturation phase, (e) Decline Phase, 11. Which of the following is not a characteristic or assumption of Product Life Cycle Costing?, (a) Product cost, revenue and profit patterns tend to follow predictable courses through the, product life cycle, (b) Each phase of the product life cycle poses different threats and opportunities, (c) The products have infinite life period, (d) Profit per unit varies as product move through their life cycle, (e) Products require different functional emphasis in each phase, 12. Most of a product’s life-cycle costs are locked in by decisions made during the, business, function of the value chain., (a) Design, (b) Manufacturing, (c) Customer-service, (d) Marketing, 13. Life-cycle costing is particularly important when, (a) the development period for R&D is short and inexpensive, (b) there are significant non-production costs, (c) most costs are locked in during production, (d) a low percentage of costs are incurred before any revenues are received, 14. Life-cycle costing, (a) has little in common with target costing, (b) is most useful to companies that manufacture small items such as household plastics, (c) helps companies estimate revenues over a multiyear horizon, (d) gives companies more insight into total costs when manufacturing costs consume the majority, of the resources, , C., , Benchmarking, , 15. The comparison of a company’s practices and performance levels against those of other, organizations is most commonly known as, (a) Benchmarking, (b) Continuous improvement, (c) Re-engineering, (d) Comparative analysis, 16. Comparing the way a "best-in-class" company performs a specific activity (such as distribution), is called, (a) Competitive Benchmarking, (b) Internal Benchmarking, (c) Analogus Benchmarking, (d) Operational Benchmarking, 17. Benchmarking allows a company to, (a) identify its strengths and weaknesses, (b) imitate those ideas that are readily transferable, (c) improve on methods in use by others, (d) all of the above, 18. Benchmarking, identifies "best-in-class" companies, analyzes the "performance gap", (a) Yes, No, (b) No, Yes, (c) Yes, Yes, (d) No, No

Page 31 :