Page 1 :

9., Final Accounts of a Proprietary concern, Contents, 9.1 Meaning, Objectives and Importance of Final Accounts., 9.2 Preparation of Trading Account., 9.3 Preparation of Profit and Loss Account, 9.4 Preparation of Balance Sheet, 9.5 Effects of following adjustments., Closing stock, Outstanding Expenses, Prepaid Expenses, Depreciation on assets, Bad debts and R.D.D., Discount on Debtors and Creditors, Income received in advance, Accrued Income, Goods distributed as free sample, Goods withdrawn by proprietor for Personal use., Interest on capital, Interest on Drawings, Competency Statements, Students are able to understand Meaning, Objective and Importance of Final Accounts., Students are able to Prepare Trading A/c, Profit and Loss A/c and Balance sheet with, competency., Students are able to understand effects of adjustments., Re, Introduction :, Accounting is considered as a scientific approach in maintaining record of business transactions., It provides a systematic accounting record to all on the financial status of the enterprise. No sooner, a business transaction takes place, the accounting process starts. The process is completed by the, drafting the final accounts., 271, 1

Page 2 :

9.1 A) Meaning of Final Accounts:, The primary aim of accounting is assessment of business performance for the benefit of all, stakeholders (such as owners, employees, suppliers, customers, financiers etc.) which will also help, them to form their opinions on the financial position of their business concerns. For this purpose,, various accounting reports are prepared in the form of Final Accounts at the end of every financial, year. In brief, Final Accounts are financial statements that valiadate and explain working results and, financial status for a specific period of time on a particular date. It is a set of Trading Account, Profit, and Loss Account and Balance Sheet. Balancing figure of Trading Account is Gross Profit, Loss. In case of Profit and Loss Account the balancing figure is Net Profit or Net Le, Balance Sheet shows financial position of assets and liabilities at a given period of tim, and Net Profit, The basic objectives of Final Accounts is to determine Gross Profit /Gross, or Net Loss of the business during the financial year., I Final Accounts shows the true and correct financial position of business, I It informs the operating results and exact financial position of the busimess to the stake holders, to take financial decisions., I It enables to control financial activities of business effectively., C) Importance of Final Accounts :, Final Accounts are the basis on which management, 9703609970, 1), businessmen decides business policies, and take financial decisions., 2), Final Accounts gives a true picture of the fina, Lstatus of business for the financial year., 3), Final Accounts are useful for accurate acc, tìng records., Transparency in business dealings are possible due to financial statemetns., Final Accounts help to get a clear break-up of amounts payable to government as various taxes,, 4), 5), e.g. Income tax, GST etc., 6) It is a mandatory requirement to maintain records of financial state of any business establishment., How to Prepare Final accounts ?-, Every time a business transaction takes place, the details of it is made in Primary books. These, entries are then posted to the ledger. At the end of a financial year the ledger accounts are balanced, and closing balance of each ledger account is determined. There many be a debit or credit balance., With the help of all these balances, a Trial Balance is prepared. This in turn helps in preparing, Trading Account, Profit and Loss Account and Balance Sheet, which is known as Final Accounts., ounting process can be represented as follows :, 272, 2, RAJU YADAV Mobile

Page 3 :

Business Transactions, Journal Entries, Ledger Posting, Balancing the ledger, Trial balance, Final Accounts at the, end of every year, Final accounts include, 1), Manufacturing Accounts, 2), Trading Account, 3), Profit and Loss Accounts, 4), Profit & Loss Appropriation Account, 5), Balance sheet, Note : Manufacturing Account and profit and Loss Appropriation account are not included, in the syllabus of XI commerce. So for XI commerce Final Accounts consist only of Trading, Account, Profit and Loss Account and Balance Sheet., Trading Account, Trading Account is an account which gives the overall preview of all trading activities. The, expenses and losses relating to trading activities are debited to this account and all outward movements, of goods and stock of goods at the end of the year are recorded to the credit side of this account., Debit side of Trading Account includes activities such as opening stock, purchases and all direct, expenses - e.g. Wages Freight, Carriage Inward, Coal, Gas, Fuel, Water, Manufacturing or Direct, expenses. Similaly credit side of trading includes Closing Stock, Sales, less returns (sales returns), any kind of goods that is used for promotions as Free Samples, goods withdrawn by proprietor for, personal reasons etc. Therefore it is said Trading Account is prepared to ascertain gross profit or loss, for a given period of time. When there is credit balance. It is referred to as Gross Profit and when, there is debit balance it refered to a Gross Loss which is transferred to profit and loss account. Trading, Account is a Nominal Account., RAIUYADA, 273, abile 9703609970

Page 4 :

Important terms of Trading Account :, 1), Stock : Goods that are unsold are called Stock., Stocks are of two types:, O Opening stock : It refers to unsold goods at the beginning of the year., Closing Stock : The unsold goods on the last day of accounting period is referred to as, Closing Stock. This is always valued at cost or market price, whichever is less. Closing, Stock is credited to the Trading Account. It is also recorded on the asset side of Balance, Sheet., (ii), Purchases : This includes the purchases of goods and not purchases of assets. Purch, may be on the basis of cash or credit. Purchase Returns are deducted from fota, thereafter net purchases are recorded on the debit side of Trading Account., 3) Sales : Sales includes the sales of goods and not sale of Assets. Sale of, basis of cash or credit. Sales returns are deducted from total sales and thereafter net sales are, recorded on the credit side of Trading Account., 2), chases and, ds may be on the, 4) Direct Expenses : Direct expenses are those expenses whichare incurred for purchase of goods,, production of goods and purchase expenses. All nominal, expenses, Factory lighting, Coal, Gas, Fuel, Water, Dook dues/Carriage inward etc., ounts e.g. Wages, Manufacturing, Specimen of Trading Account, Trading Account for the, Dr., Cr., Amount, Amount, Amount, Amount, Particulars, Particulars, (), (), (), (), To Opening Stock, XXXX | Ву Sales, XXXX, To Purchases, XXXX, Less : Sales Return, XXXX, XXXX, Less : Purchase Return, XXXX (Return Inward), XXXX, (Return outwards), By Goods distributed as, XXxx free sample, XXXX, To Direct Expenses, To Freight & Carriage, By Goods taken by, XXxx proprietor for personal, XXXX, Inward, To Custom Duty, use, XXXX, To Wages, XXxx By Closing Stock, XXXX, To Coal, Gas, Fuel etc., XXXX By Gross Loss c/d, XXXX, To Royalties, XXXX, To Factory expenses, XXXX, To Gross Profit c/d, XXXX, XXXX, XXXX, 274, 4

Page 5 :

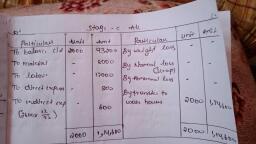

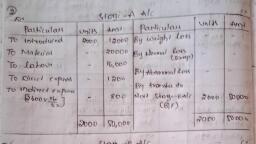

Illustration 1, From the following information prepare Trading Account of Sangita Traders for 31st March, 2019., Amt (), Amt (), Particulars, Wages, Particulars, 16,000, Stock (1.04.2018), 22,000, Royalties, 11,000, Sales, 3,80,000, Sales Returns, 24,000, Purchases, 1,90,000, Goods withdrawn by Sangita, for Personal use, Purchases Returns, 6,400, 16,000, Manufacturing Expenses, 8,400, Factory Rent, 4,200, Motive Power, 16,000, Stock (31.03.2019), 36,000, Freight, Trading Account of Sangita Traders for the year ended 31st March 2019, 7,400, Solution :, Dr., Cr., Amount, Amount, Amount Amount, Particulars, Particulars, (), (), 22,000 By Sales, (), (), To Opening stock, 3,80,000, To Purchases, 1,90,000, Less : Sales Return, 24,000 3,56,000, Less : Purchase Return, 1,83,600, 16,000 By Drawings, 11,000 By Closing stock, 6,400, To Wages, 16000, To Royalties, 36,000, To Factory Rent, 4,200, 8,400, To Manufacturing, Expenses, To Motive Power, 16,000, To Freight, 7,400, To Gross Profit c/d, 1,39,400, (Balancing figure), 4,08,000, 4,08,000, Journal Entries for preparing Trading Account, All ace, Direct expenses are closed and their balances are transferred to Trading A/c. For this, "elosing entries" are passed as under :, Transferring of Opening Stock, Purchases, Direct expenses, Transfer of Purchase Returns, Purchase Returns A/c, .Dr., XXXX, ....., To Purchases A/c, XXXX, (Being Purchase returns transferred to Purchases A/c), 275, RAN