Page 1 :

Type, INTERNAL RECONSTRUCTION, ACCOUNTING ENTRIES AT A GLANCE, Sr.No, Particulars, Amount Dr., Amount Cr., If share capital reduced, Share Capital A/c, 1., Dr., XXX, To Capital Reduction A/c, XXX, OR, Old Share Capital A/c-, -Dr., XXX, To Capital Reduction A/c, To New Share Capital A/c, XXX, XXX, For Example :-, Old Share of Rs 50 each, 50, Reduced 14 Rs each, 14, 36, The New share value is, %3D, If Share capital is two types, then, Old Preference Share Capital A/c--, Old Ordinary Share Capital A/c--, To Capital Reduction A/c, To New Share Capital A/c, 2., Dr., XXX, -Dr., XXX, XXX, XXX, If amount of capital reduction is used to write off the, losses, Fictitious intangible assets or writing down other, 3., assets., XXX, Capital Reduction A/c-----, To Profit & loss A/c, -Dr., XXX, XXX, To Intangible Assets A/c, To other assets A/c, XXX, For example :- All the balance of intangible assets are o be, written - off., If balance of capital Reduction A/c transferred to, capital Reserve, Capital Reduction A/c-, 4., -Dr., XXX, XXX, To Capital Reserve A/c

Page 2 :

SCHEME OF REORGANISATION, Rs, Application, Written off Intangible Assets, Rs, Contribution, Preference Share capital, (Reduction Amount), (Ex:- 1000 Share reduced by 25 Rs.), (1000@25 ), XXX For example -, XXX, Preliminary Exp, Profit & loss, XXX, 25000, Equity Share Capital, (Reduction Amount), (Ex:- 1000 Share reduced by Rs.40) XXX, 1000@40, Written down Other assets, For exampie -, Machinery, Stock, Free hold property, Reserve for doubtful debts, XXX, XXX, 40000, XXX, XXX, XXX, Balance transfer to capital, Reserve, XXX, XXX, XXX, Contribution is Rs, For example, Ápplication is Rs., Transfers to Capital Reserve, 4,00,000, 3.50.000, 50,000

Page 3 :

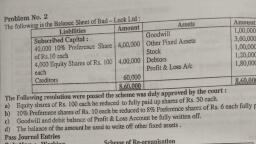

Probiem No. 1, Balance sheet of Priyanka Ltd. as on 31 march 2019 was given as under., Amount, Liabilities, Amount, Assets, Share capital issued and paid, up capital 1000 share of Rs., 100 each Rs.50 Paid up, Sundry creditors, 50,000, 25,000, 75.000, Goodwill A/c, Preliminary exp, Profit & loss A/c, 5,000, 1,000, 4,000, 65,000, 75.000, Sundry Assets A/c, The Following scheme of reconstruction is passed., Value of each share must be reduced by Rs. 12.50 each., a), All the balance of intangible assets are to be written-off., b), c), Debit balance of profit & loss A/c is also to be written off., Sundry assets are reduced for Rs. 62,500., d), Pass Journal Entries and make out balance sheet after reconstruction is made.

Page 4 :

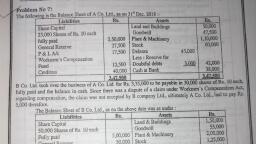

Problem No.2 The balance sheet of Sanjay company Ltd. as on 31 December 2018. Was as Follows, Balance SheetAs on 31" Dec, 2018, Liabilities, Amt, Assets, Amt, Authorized capital, 10,000 ordinary share, of Rs. 100 each, 6% of 10000 Pref. share, Of Rs. 100 each, Issue and Subscribe, 10,00,000 Freehold Property, Machinery, Stocks, 2,30,000, 5,00,000, 2,15,000, 1,40,000, 10,000, 5,000, 15,000, 1,85,000, 10.00.000 Sundry Debtors, Bills Receivable, share capital, 6000 ordinary share of Rs., 100 each Fully paid up, 6000 Pref. Share of Rs.100, each fully paid up., Sundry creditors, Bills payable, Cash & Bank A/c, Preliminary exp, Profit & loss A/c, 6,00,000, 6,00,000, 80,000, 20,000, 13.00.000, 13.00.000, The Following scheme was finally accepted and sectioned by the court., a) Pref. share were to be reduced by Rs.25 each, the rate of dividend being raised to 8%, b) The paid- up value of ordinary share was reduced to Rs.60 each the Face value remaining the same., c) The amounts made available by reduction were utilized to write of Rs.40000 From Machinery Rs.35000, From Stock and to create a reserve of Rs. 25,000 against debtors., Make journal entries recording the above transaction and draw up the balance sheet thereafter.

Page 5 :

vuraict siicel as show as above., Problem No.3, The Shareholders having agreed upon following scheme of reorganisation of Rohan Co. Ltd. and it was accepted, ky the Court. The Balance Sheet at the date recorgnisation (31" March, 2019) was as under:, Liabilities, 10,000, 8% Preference Share, of Rs. 100 each fully paid, Rs., Assets, Rs., Building, 10,00,000 Machinery, 60,00,000, 5,00,000, 4,00,000, 5,50,000, 2,00,000, 3,00,000, 50,000, 50,000, 54,000, 46,000, 2,50,000, 30.00.000, Stock, 1,00,000 Equity Share of Rs., 10 each fully paid, Sundry Debtors, 10,00,000 Bills receivable, Investments, Sundry Creditors, Bills payable, Bank Overdraft, 5,00,000 Furniture, 3,00,000 Bank, 2,00,000 Discount on Issue of Shares, Preliminary Expenses, Profit & Loss A/c, 30,00.000, The following scheme of re-organisation was adopted :-, a) The Preference Shares be reduced to an equal number of fully paid. Preference Shares of Rs. 60 each and, rate of dividend be increased to 12%., b) The Equity Shares be reduced up to Rs. 4.50 paid up., c) The amount available be utilized as under :-, To Write off Machinery by 50%., To Create Reserve for doubtful debts Rs. 40,000, To Write off the loss as per P & L A/c, Preliminary expenses and Discount on issue of Shares in full., Write off the Stock by 30%., Valued of Investments to be considered Rs. 1,50,000., Carry the balance if any to the Capital Reserve., Give necessary Journal entries and Balance Sheets after implementation of the Scheme.