Page 2 :

2

Page 4 :

,, , 4, , ,

Page 5 :

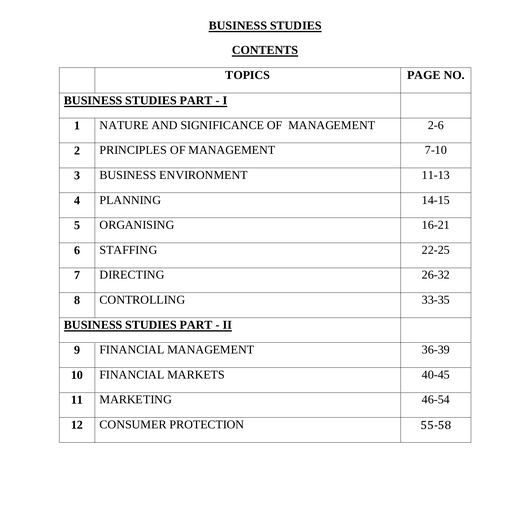

INDEX, Unit No., , Name of Units, 01, , ACCOUNTING FOR NOT-FOR-PROFIT, , Page, No., 6-10, , ORGANISATIONS, 02, THEORY, PART, , ACCOUNTING FOR PARTNERSHIP, , 11-16, , BASIC CONCEPTS, 03, , BOOK-I, , RECONSTITUTION OF A PARTNERSHIP FIRM, , 17-22, , ADMISSION OF A PARTNER, , 04, , RECONSTITUTION OF A PARTNERSHIP FIRM, , 23-27, , RETIREMENT / DEATH OF A PARTNER, , THEORY, PART, BOOK-II, , 05, , DISSOLUTION OF PARTNERSHIP FIRM, , 28-30, , 01, , ACCOUNTING FOR SHARE CAPITAL, , 31-34, , 02, , ISSUE AND REDEMPTION OF DEBENTURES, , 35-38, , 03, , FINANCIAL STATEMENTS OF A COMPANY, , 39-42, , 04, , FINANCIAL STATEMENT ANLYSIS, , 43-47, , 05, , ACCOUNTING RATIOS, , 48-51, , 06, , CASH FLOW STATEMENT, , 52-55, , PRACTICAL ORIENTED QUESTIONS WITH, , 56-60, , ANSWERS, QUESTION, PAPERS, , 01, , SOLVED QUESTION PAPERS MARCH-2019, & JUNE-2019, , 5, , 61-93

Page 6 :

BOOK-I CHAPTER – 01, ACCOUNTING FOR NOT-FOR-PROFIT ORGANISATIONS, Sec-A, (01 Marks), 01, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), -, , Sec-D, (12 Marks), 01, , SECTION – A : ONE MARK QUESTIONS, Fill in the blanks., 1) Not for Profit Organisations are used for the welfare of the ……………………, Ans : Society, 2) Not for Profit Organisations are not engaged in ……………. or ..……………., Ans : Trading or Business, 3) Receipts & Payments A/c is the summary of ………… & ……….. transactions, Ans : Cash & Bank, 4) Income & Expenditure A/c is just like a ……………… A/c of a trading concern, Ans : Profit & Loss, 5) Income & Expenditure A/c is prepared on ………………… basis, Ans : Accrual, 6) Subscription is a fee paid by the ………… Ans : Members, 7) …………….. are the amounts received as per the will of the deceased person, Ans : Legacies, 8) Opening balance of Receipts & Payments A/c represents …………….., Ans : Opening cash & bank balance, 9) Government Grant for maintenance is treated as ……. Receipts Ans : Revenue, (March - 2019), 10) Donations for specific purpose are always ….. Ans: Capital Receipts, Multiple Choice Questions :, 1. Not for Profit Organisations are formed for, a) Profit, b) Service, c) Profit & Service, d) None of these, Ans : b) Service, 2. Most of transactions of Not for Profit Organisations are., a) Cash, b) Credit, c) Cash & Credit, d) Barter, Ans : a) Cash, 3. Receipts & Payments A/c includes items of, a) Capital Nature, b) Revenue Nature, c) Both a & b, d) None of these, Ans : c) Both a & b, 4. Income & Expenditure A/c includes the amount of ;, a) Current year, b) Previous year, c) Next year, d) Both a & b, 6

Page 7 :

Ans : a) Current year, 5. Capital fund does not includes, a) Entrance fees, b) Legacies, c) Building fund, d) Life membership fees, Ans : c) Building fund, 6. Legacies are treated as, a) Revenue Receipts, b) Capital Receipts, c) Revenue Expenditure, d) Capital Expenditure, Ans : b) Capital Receipts, 7. Purchase of a Computer by a College is treated as, a) Capital Receipts, b) Capital Expenditure, c) Revenue Receipts, d) Revenue Expenditure, Ans : b) Capital Expenditure, 8. In the absence of any specific instruction, where do you show the entrance fee ?, a) Debit side of Income & Expenditure A/c, b) Credit side of Income & Expenditure A/c, c) Liabilities side of the B/S, d) Added to capital fund on the liabilities side of B/S, Ans : b) Credit side of Income & Expenditure A/c, 9. Special Funds are shown in :, a) Income side, b) Expenditure side, c) Liabilities side, d) Assets side, Ans : c) Liabilities side, 10. Life membership fees are treated as:, a) Capital Receipts, b) Capital Expenditure, c) Revenue Receipts, d) Revenue Expenditure, Ans : a) Capital Receipts, 11. Loss on sale of fixed asset is treated as :, a) Capital Receipts, b) Revenue Receipts, c) Capital Expenditure, d) Revenue Expenditure, Ans : d) Revenue Expenditure, True or False, 1., 2., , 3., , Receipts & Payments A/c is a summary of all Capital Receipts and all Capital, Payments. Ans : False, If the Sports Fund is maintained, Sports expense will be shown on the debit side, of Income & Expenditure A/c, Ans : False, The balancing figure on credit side of I & E A/c denotes excess of expenses over, incomes., Ans : True, 7

Page 8 :

4., , Scholarship granted to students out of funds provided by Government will be, debited to I & E A/c, Ans : False, 5. Donations for specific purpose are always capitalized., Ans : True, 6. Opening Balance Sheet is prepared when the opening balance of capital fund is, not given., Ans : True, 7. Surplus of I & E A/c is added to Capital Fund, Ans : True, 8. I & E A/c is equivalent to P & L A/c of a trading concern., Ans : True, 9. Receipts & Payments A/c does not differentiate between capital & revenue, receipts., Ans : True, 10. Capital & Revenue items are recorded in Receipts & Payments A/c., Ans : True, Very Short Answer Questions :, 1. Give an example for Not-For-Profit Organisation, Ans : Sports Club, 2. What is the motive of Not-For-Profit Organisation, Ans : Service, 3. Where do you show opening bank overdraft in Receipts & Payments A/c?, Ans : Credit side of Receipts & Payments A/c, 4. Name any One final A/c of a Not-For-Profit Organisation., Ans : Income & Expenditure A/c, 5. State any one major source of Income of Not-For-Profit Organisation., Ans : Subscriptions, 6. State any one books of A/cs maintained by an NPO., Ans : Cash book, 7. State any one feature of Receipts & Payments A/c, Ans : Summary of Cash or Bank Transactions, 8. How do you treat the prizes paid, when the prize fund is not maintained?, Ans : Prizes paid are debited to Income & Expenditure A/c, 9. What is Capital Fund ?, Ans : Capital Fund is the difference between assets & liabilities of a Not for, Profit Organisation., 10. Give an example for specific donation., Ans : Donation for Building, (June-2019), , 8

Page 9 :

11. How do you treat the tournament expenses, when the tournament fund is, maintained ?, Ans : Tournament expenses are deducted from Tournament Fund on the, liabilities side of the Balance Sheet., 12. How do you treat the life membership fees ?, Ans : Life membership fees are treated as capital receipts, 13. State the meaning of Not-For-Profit Organisation., Ans : Not-For-Profit Organisations refer to the Organisations that are, formed for the welfare of the society without any intention of profit., 14. State the meaning of Receipts & Payments A/c?, Ans : Receipts & Payments A/c is a summary of cash & bank transactions, prepared at the end of accounting year., 15. State the meaning of Income & Expenditure A/c?, Ans : Income & Expenditure A/c is a summary of incomes & expenditures of, Not for Profit Organisation for the accounting year., 16. What is Subscription ?, Ans : Subscription is a membership fee paid by the member on annual basis., , TWO MARKS QUESTIONS, 1. What are Not-For-Profit Organisations ?, (June – 2019), Ans : Not-for-Profit Organisations refer to those which are formed to render, social services and are set up as charitable institution which function without, any motive of profit., 2. Give any two examples of Not-For-Profit Organisation., Ans : a) Sports Club, b) Schools & Colleges, 3. State any two features of Not-For-Profit Organisation., Ans : a) Formed for providing service, b) Organized as societies & charitable trusts., 4. Name any two books of accounts maintained by Not-For-Profit Organisation., Ans : a) Cash Book, b) Stock Register, 5. Give the meaning of Receipts & Payments A/c., Ans : Receipts & Payments A/c is a summary of cash & bank transactions, which is prepared at the end of accounting year., 6. State any two features of Receipts & Payments A/c., (March 2019), Ans : a) Summary of cash or bank transactions, b) Includes both capital & revenue items., 7. What do you mean by Income & Expenditure A/c ?, Ans : Income & Expenditure A/c is a summary of incomes & expenditures of, a Not for Profit Organisation for the accounting year., 9

Page 10 :

8., , 9., 10., 11., 12., , 13., , 14., , 15., , 16., , 17., , 18., , 19., , State any two features of Income & Expenditure A/c., Ans : a) Includes only revenue items of current year, b) It includes non-cash items also, Give any two examples for revenue expenditure., Ans : a) Salary paid, b) Printing Charges, Give any two examples for capital expenditure, Ans : a) Sports materials purchased b) Computers bought, Give any two examples for revenue receipts., Ans : a) Subscriptions received, b) Interest received, Give any two examples for capital receipts., Ans : a) Life membership fees received, b) Special donations received, State two differences between Receipts & Payments A/c & Income &, Expenditure A/c., Receipts & Payments A/c, Income & Expenditure A/c, a) Summary of cash book, a) Summary of Incomes &, Expenditures, b) It includes both capital &, b) It includes only revenue items, revenue items, What is capital fund ?, Ans : Capital fund is the difference between assets & liabilities of Not for, Profit Organisation as on a particular date., What are Legacies ?, Ans : Legacies are the gifts received by Not for Profit Organisation under a, will, on the death of a donor., What is Honorarium ?, Ans : Honorarium is the amount paid to the person who is not the regular, employee of the organisation, for his services., Give the meaning of endowment fund ?, Ans : Endowment fund is a fund arising from a bequest or gift, the income of, which is devoted for a specific purpose., How do you treat tournament expenses, when separate tournament fund is not, maintained?, Ans : When separate tournament fund is not maintained, then tournament, expenses are debited to Income & Expenditure A/c., How do you treat prizes awarded, when prize fund is maintained ?, Ans : When prize fund is maintained, prizes awarded are deducted from the, prize fund on the liabilities side of the Balance Sheet., , 10

Page 11 :

CHAPTER – 02, ACCOUNTING FOR PARTNERSHIP : BASIC CONCEPTS, Sec-A, (01 Marks), 01, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), 01, , Sec-D, (12 Marks), -, , SECTION – A : ONE MARK QUESTIONS, I) Fill in the blanks questions :, 1) Section ……………… of Indian Partnership Act, 1932 defines Partnership., Ans : 4, 2) A Partnership has no separate …………………… entity Ans : Legal, 3) In order to form a Partnership, there should be at least ………………… persons., Ans : 2 (Two), 4) Partnership is the result of ………………… between two or more persons to, carry on business and share its profits and losses. Ans : Agreement, 5) It is preferred that the Partners have a …………………… agreement., Ans : written, 6) The agreement should be to carry on some ……………. Business Ans : Lawful, 7) Each partner carrying on the business is the principal as well as the………… of, all other Partners. Ans : Agent, 8) The liability of a partner for his acts is ………………….. Ans : Unlimited, 9) In the absence of Partnership deed Interest on advance from partner will be, charged at ………………. Ans : 6% p.a., 10) Under …………….. method, the capitals of the Partners shall remain fixed., Ans : Fixed capital, 11) Under fluctuating capital method, the Partner’s Capital Account balances, …………. from time to time. Ans : Fluctuate, 12) P & L Appropriation A/c is merely an extension of ……… Account of a firm., Ans : Profit and Loss, 13) Profit and Loss Appropriation Account ……………… Dr, To ………….. Accounts, (Being Transfer of interest on capital to P & L Appropriation A/c), Ans : Interest on Partners’ Capital, 14) ……………….. …….. A/c, Dr., To salary to Partner’s account, (Being Transfer of Partner’s salary to P & L Appropriation A/c), Ans : Profit and Loss Appropriation, 15) P & L Appropriation A/c .., Dr., To Partners Capital / Current A/cs., (………………………………………………………), 11

Page 12 :

16), , 17), 18), 19), , 20), , Ans : Being Profit transferred to Partners Capital or Current A/cs, When fixed amounts are withdrawn at the end of every month, interest on the, total amount for the year ending is calculated for ………….. months., Ans : 5.5 (5 ½ ), Under fluctuating capital method, all the transactions relating to Partners are, directly recorded in the ………….. Accounts. Ans : Partners Capital, Under Fixed Capital Method, the amount of capital remains …………………, Ans : Fixed, Under Fixed Capital Method, all the transactions relating to a partner are recorded, in a separate account called ……………… Account., Ans : Partner’s Current, There is not much difference in the final accounts of a sole proprietary concern, and that of a ……………………. Ans : Partnership Firm, , II) Multiple Choice Questions., 1) The agreement between the partners should be in,, a) Oral, b) Written, c) Oral / written, d) None of the above, Ans : c) Oral / Written, 2) Partnership deed contains :, a) Name of firm, b) Name and address of the Partners, c) Profit sharing ratio, d) All of the above, Ans : d) All of the above, 3) If any partner has advanced money to the firm beyond the amount of his capital,, he shall be entitled to get interest on the amount at the rate of, a) 5% p.a., b) 6% p.a., c) 8 % p.a., d) None of the above, Ans : b) 6% p.a., 4) Interest on capital is generally provided for, in that situations when, a) The Partners contribute unequal amounts of capital but share profits equally., b) The capital contribution is same but profit sharing is unequal., c) Both the situations above, d) None of the above, Ans : c) Both the situations above, 5) When fixed amount is withdrawn on the first day of every month, interest on total, amount of the year ending will be calculated for :, a) 2 & ½ months, b) 4 & ½ months, c) 6 & ½ months, d) None of the above, Ans : c) 6 & ½ months, 6) When varying amounts are withdrawn at different intervals, the interest is, calculated using,, a) Simple method, b) Average method, c) Product method, d) None of the above, 12

Page 13 :

7), , 8), , 9), , 10), , 11), , 12), , 13), , Ans : c) Product method, Adjustment for correction of omission & commission can be made,, a) In Profit & Loss Adjustment Account, b) Directly in the Capital Accounts of concerned Partners, c) Both the situations above, d) None of the above, Ans : c) Both the situations above, In order to form a Partnership there should be at least :, (June 2019), a) One person, b) Two persons, c) Seven persons, d) None of the above, Ans : b) Two persons, The business of a Partnership concern may be carried on by :, a) All the Partners, b) Any of the them acting for all, c) All Partners or any of them acting for all, d) None of the above, Ans : c) All Partners or any of them acting for all, The agreement between Partners must be to share :, a) Profits, b) Losses, c) Profits & Losses, d) None of the above, Ans : c) Profits & Losses, The liability of a partner for acts of the firm is :, a) Limited, b) Unlimited, c) Both the above, d) None of the above, Ans : b) Unlimited, The Partnership Deed should be properly drafted and prepared as per the, provisions of the, a) Partnership Act, b) Stamp Act, c) Companies Act, d) None of the above, Ans : a) Partnership Act, The clauses of Partnership Deed can be altered with the consent of :, a) Two Partners, b) Ten Partners c) Twenty Partners d) All the Partners, Ans : d) All the Partners, , III) True or False questions., 1) The agreement between Partners must be in writing. Ans : False, 2) The clauses of Partnership deed can be altered with the consent of all the Partners., Ans : True, 3) If the Partnership deed is silent about the profit sharing ratio, the profit or loss of, the firm is to be shared equally. Ans : True, 4) In the absence of an agreement, a partner is entitled to claim interest at the rate of, 10% p.a. on the amount of capital contributed by him. Ans : False, 5) In the absence of Partnership Deed, no partner is entitled to get salary., Ans : True, 13

Page 14 :

6) Under Fixed Capital Method, the Partners Capital Accounts will always show a, credit balance. Ans : True, 7) Under Fixed Capital Method, the Partners’ Capital Accounts will always show a, debit balance., Ans : False, 8) P & L Appropriation A/c shows how the profits are appropriated among the, Partners. Ans : True, 9) When fixed amount is withdrawn during the middle of every month, interest on, total amount is calculated for 6 months., Ans : True, 10) If there is a loss, no interest on capital is to be paid to Partners, even if there is a, provision in the Partnership deed. Ans : True, 11) Accounting treatment for Partnership is similar to that of a sole proprietorship, business. Ans : True, 12) There are two methods by which the capital accounts of Partners can be, maintained. Ans : True, 13) Profit and Loss Appropriation Account is merely an extension of the Profit and, Loss Account of a firm. Ans : True, 14) Interest on Partners capital is debited to Partners Capital Accounts. Ans : False, 15) In case of Guarantee of profit to a partner, assurance may be given by one partner., Ans : True, IV) Very short answer questions., 1) Who is a partner ?, Ans : Partner is a person who had entered into Partnership with one another, is individually called partner., 2) What do you mean by Partnership Firm ?, Ans : It is an association of two or more persons who carry a joint business, and share the profits., 3) State any one feature of Partnership, Ans :Agreement, 4) What is the minimum number of Partners in a Firm ? Ans : Two, 5) Name any one content of Partnership Deed., Ans : Name and Address of all the Partners, 6) Name any one method of maintaining capital accounts of Partners., i) Fixed Capital Method, 7) Name any one final account of Partnership firm. Ans : Profit and Loss Account, 8) How do you distribute profit or loss among the Partners in the absence, Partnership deed ? Ans : Equally, 9) Why the Profit and Loss Appropriation account is prepared ?, Ans : It is prepared how the Profit are appropriated among the Partners, after making necessary adjustments., 10) At what rate interest on advances by Partners is to be paid as per Partnership act?, Ans : 6% p.a., 14

Page 15 :

11) When interest is charged on Partners drawings ?, Ans : Interest is charged on Partners drawings when there is a provision in, the agreement among the Partners about it., 12) When Partners’ Current Accounts are prepared in Partnership firms? (March2019), Ans : Partners Current Accounts are prepared in Partnership firms, when, Partners’ Capital Accounts are maintained under Fixed Capital Method., 13) State any one special aspect of Partnership accounts., Ans : Maintenance of Partners Capital A/cs., 14) When the Current Accounts of Partners are opened ?, Ans : Current A/cs of Partners are opened in Fixed Capital Method, 15) Under fluctuating capital method, how many accounts are maintained for each, partner ?, Ans : One, 16) State any one feature of fluctuating capital method, Ans : Capital balance of each partner changes year after year., 17) State any one situation in which provision of payment of interest on partners, capital is made., Ans : If there is an agreement and there is a profit., 18) Find out interest at 8% p.a. on capital of Rs. 50,000 for 9 months., Ans : Rs. 3,000, 19) Which is the suitable method of calculation of interest on drawings, when fixed, amount is withdrawn every month?, Ans : Average period method, 20) Give one example for past adjustment ?, Ans : Commission or interest on capital, , SECTION – B : TWO MARKS QUESTIONS, 1) What is Partnership ?, Ans : Partnership is a relation between two or more persons who join hands, to set up a business and share its profits and losses., 2) Define Partnership, Ans : According to sec 4 of the Indian Partnership Act – 1932 “Partnership is, the relation between persons who have agreed to share the profits of a, business carried on by all are any of them acting for all”, 3) State any two features of Partnership (June 2019), Ans : a) Two or more persons b) Agreement between Partners, 4) What is Partnership Deed ?, Ans : Partnership Deed is the written agreement on stamp paper containing, terms of Partnership, duly signed by all Partners., 5) What are the methods of maintaining capital accounts of Partners ?, Ans : a) Fixed Capital Method, b) Fluctuating Capital Method, 15

Page 16 :

6) What is Fixed Capital Method ?, Ans : Fixed Capital Method is a method of maintaining Partners capital a/cs,, in which the capital balances of the Partners shall remain fixed. All, adjustments relating to Partners are recorded in a separate account called, Partners Current Accounts., 7) What is fluctuating capital method ?, Ans : Fluctuating capital method is a method of maintaining Partners capital, a/cs, in which all adjustments relating to partners are recorded in their, Capital A/cs., 8) State any two differences between fixed and fluctuating capital methods., Fixed Capital Method, Fluctuating Capital Method, 1) Adjustments are made 1) Adjustments are made in Partners capital A/cs., in Current A/c, 2) Capital balance, 2) Capital balance fluctuates year by year., remains unchanged, 9) What do you mean by Profit and Loss Appropriation Account ?, Ans : Profit and Loss Appropriation A/c is the extension of P & L A/c which, shows the appropriation of profits among the Partners after making, necessary adjustments., 10) What is guarantee of profit to a Partner ?, Ans : Guarantee of profit to a partner means giving assurance of certain, minimum amount by way of his share of profits of the firm., 11) What do you mean by past Adjustments?, Ans : Past Adjustments refer to, making necessary rectifications for, commissions or omissions noticed after preparation of final accounts., 12) State any two final accounts of a Partnership firm., Ans : a) Profit and Loss A/c and, b) Balance Sheet, 13) In the absence of Partnership deed, specify the rules relating to the followings:, a) Sharing of profits & losses b) Interest on partners capital, Ans : a) Equally, b) Not to be allowed, 14) State the rules relating to the followings in the absence of Partnership Deed., a) Interest on drawings, b) Interest on advances from Partners, Ans : a) Not to be charged b) 6% p.a., 15) Name any two methods for calculation of Interest on drawings., Ans : a) Product Method, b) Average Period Method, 16) When the interest on drawings is generally provided to Partners ?, Ans : Interest on drawings is generally charged on partners when it is, specifically expressed in an agreement., 17) How do you close Profit and Loss Appropriation Account in Partnership ?, Ans: Profit and Loss Appropriation A/c in Partnership is closed by transferring, its balance to Partners Capital or Current A/cs, as the case may be., 18) State any two special aspects of Partnership A/cs., Ans : a) Maintenance of Partners Capital A/cs., b) Distribution of P & L among Partners., 19) Name any two contents of Partnership Deed., (March 2019), Ans : a) Profit Sharing Ratio, b) Capitals of Partners, 16

Page 17 :

CHAPTER – 03, RECONSTITUTION OF A PARTNERSHIP FIRM, ADMISSION OF A PARTNER, Sec-A, (01 Mark), 01, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), 01, , Sec-D, (12 Marks), 01, , SECTION – A ONE MARK QUESTIONS, I) Fill in the blanks questions :, 1), , ……………… Ratio is used to distribute accumulated profits and losses at the, time of admission of a new partner. Ans : Old, , 2), , Profit or loss on revaluation is shared among the old Partners in ………………, ratio. Ans : Old, , 3), , Old Ratio - New ratio = …………………. Ans : Sacrificing Ratio, , 4), , Accumulated losses are transferred to the capital accounts of the old Partners at, the time of admission in their …………….. ratio. Ans : Old, , 5), , General reserve is to be transferred to …………… accounts at the time of, admission of a new partner. Ans : Partners Capital, , 6), , Goodwill brought in by new partner in cash is to be distributed among old, Partners in …………….. ratio. Ans : Sacrificing, , 7), , If the amount brought by new partner is more than his share in capital, the excess, is known as …………………, , (March 2019), , Ans : Hidden Goodwill, 8), , …………….. Account is debited for increase in the value of an asset. Ans : Asset, , 9), , Unrecorded asset is to be credited to ………….. account. Ans : Revaluation, , 10) A and B are partners sharing profits and losses equally with capitals of Rs. 45000, each. C is admitted for 1/3rd share and he brings in Rs. 60000 as his capital, Hidden Goodwill is ………………Ans : 30000, 11) Due to change in profit sharing ratio, some Partners will gain in future profits, while others will ……………… Ans : Lose, 12) Goodwill is an …………………. asset. Ans : Intangible, 13) ………….. account is credited for cash brought in by new partner for his share of, Goodwill. Ans : Goodwill, 14) ……….. ratio is required for sharing future profits and also for adjustment of, capitals. Ans : New Profit Sharing Ratio, 17

Page 18 :

II) Multiple choice questions :, 1) At the time of admission of a new partner general reserve appearing in the old, balance sheet is transferred to., a) All Partners Capital Accounts, b) New Partners Capital Account, c) Old Partners Capital Accounts, d) None of the above, Ans : c) Old Partners Capital Accounts, 2) A,B and C are Partners in a firm. If D is admitted as a new partner., a) Old firm is dissolved, b) Old firm & old Partnership are dissolved, c) Old Partnership is reconstituted d) None of the above, Ans : c) Old Partnership is reconstituted, 3) On the admission of a new partner, increase in the value of asset is credited to :, a) Profit and loss Adjustment (Revaluation) A/c, b) Asset Account, c) Old Partner’s Capital Accounts, d) None of the above, Ans : a) Profit and loss Adjustment (Revaluation) A/c, 4) At the time of admission of a partner, undistributed profits appeared in the, balance sheet of the old firm is transferred to the capital accounts of …………., a) Old Partners in old profit sharing ratio, b) Old Partners in new profit sharing ratio, c) All the Partners in new profit sharing ratio, d) None of the above, Ans : a) Old Partners in old profit sharing ratio, 5) If new partner brings cash for his share of Goodwill. Goodwill is transferred to, old Partners Capital accounts in, a) Sacrificing ratio, b) Old profit sharing ratio, c) New profit sharing ratio, d) None of the above, Ans : a) Sacrificing ratio, 6) Which of the following are treated as reconstitution of a Partnership firm., a) Admission of a partner, b) Change in profit sharing ratio, c) Retirement of a partner, d) All the above, Ans : d) All the above, 7) Profit or loss on revaluation is shared among the Partners in the., a) Old profit sharing ratio, b) New profit sharing ratio, c) Capital ratio, c) Equal ratio, Ans : a) Old profit sharing ratio, 8) Assets and Liabilities are recorded in Balance sheet after the admission of a, partner at, a) Original Value, b) Revalued Value, c) Realizable Value, d) None of the above, Ans : b) Revalued Value, 9) On the admission of a new partner,the increase in the value of an asset is credited to :, a) Revaluation Account, b) Asset Account, c) Old Partners capital Accouunt, d) None of the above all account, Ans : a) Revaluation Account, 18

Page 19 :

10) Old profit sharing Ratio - New Profit sharing Ratio is = ……………….., a) Sacrificing ratio, b) Gaining ratio, c) Both the above, d) None of the above, Ans : a) Sacrificing ratio, 11) In the absence of an agreement to the contrary it is implied that old Partners will, contribute to new Partner’s share of profit in the ratio of ;, a) Capital, b) Old profit sharing ratio, c) Sacrificing ratio, d) Equally, Ans : b) Old profit sharing ratio, 12) The balance of reserves and other accumulated profits at the time of admission of, a new partner are transferred to, a) All Partners in the new ratio, b) Old Partners in the new ratio, c) Old Partners in the old ratio, d) Old Partners in the sacrificing ratio, Ans : c) Old Partners in the old ratio, 13) Goodwill raised in books at the time of admission of partner will be written off in, a) Old profit sharing ratio, b) New profit sharing ratio, c) Sacrificing ratio, d) None of the above, Ans : b) New profit sharing ratio, 14) Revaluation Account is debited for the, a) Increase in provision for doubtful debts, b) Increase in the value of building, c) Decrease in the value of creditors, d) Transfer of loss on revaluation, Ans : a) Increase in provision for doubtful debts, 15) A and B are Partners sharing profits in the ratio of 3:1. C is admitted into, Partnership for 1/4th share the sacrificing ratio of A and B will be ;, a) Equal, b) 3:1, c) 2:1, d) 3:2, Ans : b) 3:1, III) True or false type Questions :, 1) Goodwill brought in cash by new partner is distributed among old partners in their, sacrificing ratio. Ans : True, 2) In case of admission of a partner profit or loss on revaluation is transferred to Old, Partners Capital accounts. Ans :True, 3) Accumulated profit is transferred to all Partners Capital accounts including new, partner. Ans : False, 4) The debit balance of profit and loss account shown in the assets side of the Balance, sheet will be debited to Old Partners capital accounts. Ans : True, 5) Increase in the value of an asset is credited to Revaluation account. Ans : True, 6) The traditional name of Revaluation A/c is profit and loss Adjustment A/c, Ans : True, 7) Decrease in the value of liability is debited to Revaluation Account. Ans : False, 8) Goodwill is an intangible asset. Ans : True, 9) Sacrificing ratio is required to distribute the cash brought in by new partner among, old Partners for his share of Goodwill. Ans :True, 10) Share Sacrificing = Old share – New share. Ans : True, 19

Page 20 :

IV) Very short Answer Questions :, 1) What is Partnership ?, Ans : Partnership is an agreement between two or more persons (called, Partners for sharing the profits of a business carried on by all or any of them, acting for all., 2) What do you mean by reconstitution of a Partnership firm ?, Ans : Any change in the existing agreement amounts to reconstitution of the, Partnership firm., 3) State any one reason for admission of a new partner. Ans : To Increase the Capital, 4) State any one right acquired by a newly admitted partner., Ans : The right to acquired share in the assets and profits of the Partnership, firm., 5) Why the NPSR is required at the time of admission of a partner ?, Ans : NPSR is required to share the future profit or losses., 6) What is Goodwill ?, Ans : Over a period of time, a well established business develops an advantage, of good name, reputation and wide business connections, and it is termed as, Goodwill., 7) State any one factor affecting the value of Goodwill., Ans : Nature of Business, 8) What is Normal profit ?, Ans : Normal profit means normal return on capital employed., 9) State any one method of valuation of Goodwill., (June 2019), Ans : Average profit Method, 10) Give the formula for Sacrificing ratio., Ans : Sacrificing Ratio = Old Ratio – New Ratio, 11) Which Account is to be debited to record the Increase in the value of an asset ., Ans : Assets Account, 12) What is revaluation Account ?, Ans : Revaluation A/c is an a/c prepared in connection with recording of, increase or decrease in value of Assets and liabilities and find out the P & L of, Revaluation., 13) Which Account will be credited when there is a loss on revaluation ?, Ans : Revaluation A/c, 14) Which account will be debited, when the cash is brought in by a new partner for his, share of Goodwill ? Ans : Cash / Bank A/c, 15) What is hidden Goodwill ?, Ans : Hidden Goodwill refers to the difference between total required capital &, actual capital of all Partners., , SECTION – B TWO MARKS QUESTIONS, 1) When the Goodwill is distributed among old Partners in the Sacrificing Ratio ?, Ans : When the Goodwill is brought in cash by new partner, it is distributed in, sacrificing ratio., 20

Page 21 :

2), 3), , 4), , 5), , 6), , 7), , 8), , 9), , 10), , 11), , 12), , 13), , State any two method of valuation of Goodwill., Ans : a) Average profits method, b) Super profits method, State any two rights acquired by a new partner., Ans : a) Right to share the assets of the Partnership firm., b) Right to share the profits of the Partnership firm., What do you mean by hidden Goodwill ?, Ans : Hidden goodwill refers to Goodwill which value is not given at the time of, admission but has to be inferred from arrangement of capitals and profit, sharing ratio., Pass the Journal entry to write off the Goodwill raised to the extent of full value., Ans : All Partners Capital A/cs ….. Dr., xxx …, To Goodwill A/c (New ratio), … xxx, (Being writing off of full value of Goodwill), State any two matters which need adjustments in the books of the firm at the time of, admission of a new partner., Ans : a) Revaluation of assets & liabilities, b) Valuation and adjustment of Goodwill, What is Sacrificing ratio ?, Ans : It is the Ratio in which the old Partners Sacrifice or surrender a part of, their share of profits to the new partner on account of admission. Sacrifice, Ratio is the excess of old share over the new share., Why the Sacrifice ratio is calculated ?, Ans: Sacrificing Ratio is calculated in order to distribute the Goodwill brought, in cash, by the new partner on account of admission., What is the need for the revaluation of assets and liabilities on the admission of a, partner ?, Ans : The need for the revaluation of assets and liabilities is to ascertain true, financial position of the business., State any two reasons of admitting a new partner, Ans : a) To increase the capital, b) To improve the managerial ability, How do you close Revaluation Account when there is a profit ?, Ans : If there is profit, revaluation A/c is closed by debiting revaluation A/c and, crediting old Partners capital A/cs., State any two factors which determine the Goodwill of the firm ?, Ans : a) Efficiency of management, b) Market situation, What is Average profit method of valuation of Goodwill ?, Ans : Under this method, the Goodwill is valued at agreed number of years, purchase of the average profits of the past few years., , 21

Page 22 :

14) Goodwill of the firm valued at two years purchase of the average profit of last four, years. The total profits for last four year is Rs. 40000 Calculate the Goodwill of the, firm., Ans : a) Average profit, , = Total profits, No.of Years, , (March 2019), , = Rs.40000, 4, = Rs. 10000, b) Goodwill = average profit x No. of years purchase, = 10000 x 2, = Rs. 20000/15) Pass the Journal entry for increase in the value of building on the admission of a, partner., Ans : Building A/c…….. Dr, xxx ………, To Revaluation A/c, …… xxx, (Being increase in the value of Building), 16) Pass the Journal entry for the decrease in the value of a liability., Ans : Liability A/c …………. Dr., , xxx, , …….., , To Revaluation A/c, (Being decrease in the value of liability), , ……, , xxx, , 22

Page 23 :

CHAPTER – 04, RECONSTITUTION OF A PARTNERSHIP FIRM, RETIREMENT / DEATH OF A PARTNER, Sec-A, (01 Marks), 01, , Sec-B, (02 Marks), -, , Sec-C, (06 Marks), 02, , Sec-D, (12 Marks), 01, , SECTION – A : ONE MARK QUESTIONS, I) Fill in the blanks., 1) ………….. ratio is used to distribute accumulated profits and losses at the time of, retirement of a partner. Ans : Old, 2) Profit or loss in revaluation is shared among the Partners in ………….. ratio on, retirement of a partner. Ans : Old, 3) New ratio – old ratio = Ans : Gain Ratio, 4) Accumulated losses are transferred to the capital Accounts of the Partners at the time, of retirement in their …………. Ratio. Ans : Old, 5) General reserve is to be transferred to ……………. Accounts at the time of, retirement of a partner. Ans : All the Partners capital, 6) Goodwill raised to the extent of retiring Partner’s share only is to be debited to, continuing Partners Capital Accounts in ………… ratio. Ans : Gain, 7) In the absence of any instruction retiring Partners capital A/c is closed by, transferring its balance to …………….. A/c. Ans : Retiring Partner’s loan, 8) ………………. Ratio is used for adjustment of continuing Partners capitals, Ans : New, 9) X, Y and Z are the Partners sharing profits and losses in the ratio of 3:2:1. If Y, retires, the new ratio of X and Z will be ……………. Ans : 3: 1, 10) Share gained is calculated by deducting ……………… share from the new share., Ans : Old, 11) The ratio in which the remaining Partners will share future profits after retirement is, called ………….. ratio. Ans : New, 12) The balance in the retiring Partner’s loan A/c is shown on the ………. Side of the, B/S till the last installment is paid. Ans : Liabilities, 13) The amount paid to the retiring partner in excess of what is due to him is called, …………… Goodwill. Ans : Hidden, 14) In the absence of any agreement as the disposal of amount due to retiring partner Sec, ………. of the Indian Partnership Act 1932 is applicable. Ans : 37, 15) If Goodwill already appears in the books it will be written off by debiting, ………….. Accounts in their OPSR. Ans : All Partners capital, , 23

Page 24 :

II) Multiple choice Questions., 1) Abhishek, Rajat and Vivek are Partners sharing profits in the ratio of 5:3:2. If Vivek, retires the new profit sharing Ratio between Abhishek and Rajat will be., a) 3:2, b) 5:2, c) 5:3, d) None of the above, Ans : c) 5:3, 2) The old profit sharing ratio among Rajender, Satish and Tejpal were 2:2:1. The New, profit sharing Ratio after Satish’s retirement is 3:2. The gaining ratio is., a) 3:2, b) 1:1, c) 2:1, d) 2:2, Ans : c) 1:1, 3) Anand, Bahadhur and Chandru are Partners sharing profit equally. On Chandru’s, retirement his share is acquired by Anand and Bahadhur in the ratio of 3:2. The New, profit sharing Ratio between Anand and Bahadhur will be., a) 8:7, b) 3:2, c) 4:5, d) 2:3, Ans : a) 8:7, 4) In the absence of any information regarding the acquisition of share in the profit of, the retiring / deceased partner by the remaining Partner’s it is assumed that they will, acquire his / her share in, a) Old profit sharing ratio, b) Equal Ratio, c) New Profit sharing ratio, d) None of the above, Ans : a) Old profit sharing ratio, 5) On retirement / death of a partner the Retiring / Deceased Partner’s Capital Account, will be credited with., a) his / her share of Goodwill, b) Goodwill of the firm, c) Shares of Goodwill of remaining Partner’s, d) none of the above, Ans : a) his/her share of Goodwill, 6) Govind, Hari and Pratap are Partners. On retirement of Govind the goodwill already, appears in the Balance sheet at Rs. 24000. The Goodwill will be written off by debiting., a) All Partners Capital Accounts in their old profit sharing ratio, b) Remaining Partners Capital Accounts in their New profit sharing ratio, c) Retiring Partner’s Capital Accounts from his share of Goodwill., d) None of the above, Ans : a) All Partners Capital Accounts in their old profit sharing ratio, 7) Chaman, Raman and Suman are Partners sharing profits in the ratio of 5:3:2. Raman, retires, the new profit sharing ratio between Chaman and Suman will be 1:1. The, Goodwill of the firm is valued at Rs. 1,00,000. Ramans share of goodwill will be, adjusted by., a) Debiting Chaman’s capital Account and Suman’s Capital Account with Rs. 15000, each., b) Debting Chaman’s capital Account and Suman’s Capital Account with Rs. 21429, and 8571 respectively., c) Debiting only Suman’s Capital Account with Rs. 30000, d) Debiting Raman’s Capital Account with Rs. 30000, Ans : c) Debiting only Suman’s Capital Account with Rs. 30000, 24

Page 25 :

8) On retirement / death of a partner the remaining partners who have gained due to, change in profit sharing ratio should compensate the., a) Retiring Partner’s only, b) Remaining Partners as well as retiring Partners., c) Remaining Partners only (who have Sacrificed), d) None of the above, Ans : b) Remaining Partners as well as retiring Partner’s., , III) True or False Type Questions., 1) Profit or loss on revaluation is transferred to all Partners Capital Accounts in case of, retirement of a partner. Ans : True, 2) Accumulated profit is transferred to continuing Partners Capital Accounts., Ans : False, (June 2019), 3) Adjustment of Partners capitals of the remaining Partners is to be made in the New, Ratio. Ans : True, 4) New share = Old share + Share Sacrificing. Ans : False, 5) Share gained is computed by deducting old share from New Share. Ans : True, 6) Increase in the value of asset is debited to Revaluation Account. Ans : False, 7) Gain ratio is used to adjust the goodwill raised to the extent of retiring partner share, only. Ans : True, 8) Full value of goodwill raised on retirement, is credited to all Partners Capital, Accounts including retiring partner in their old ratio. Ans : True, 9) Sec 37 of the Indian Partnership Act 1932 states that the outgoing partner has an, option to receive either interest @ 6% p.a. till the date of payment or such share of, profits which has been earned with his money. Ans : True, IV) Very Short Answer Questions., 1) What do you mean by retirement of a partner ?, Ans : A partner is said to be retired from a firm when his relation with the firm, as a partner comes to an end., 2) Give the formula for calculating Gain ratio., Ans : Gaining Ratio = New Ratio – Old share, 3) Why the Gain Ratio is required on retirement of a partner ?, Ans : It is required for the purpose of writing off Goodwill created to the extent, of Retiring Partner’s Share., 4) Why the New Ratio is required on retirement of a partner ?, Ans : It is required to share future P/L between continuing Partners., 5) When do you prepare Executors Account ?, Ans : Executors A/c is prepared at the time of death of a Partner, 6) Give the formula for calculation of new profit sharing ratio on retirement of a, partner., (March 2019), Ans : New share = Old share + Share gained, , 25

Page 26 :

7) What do you mean by Hidden Goodwill ?, Ans : It refers to the amount paid to Retiring Partner in excess of actual, amount due to him., 8) Portion gained = New Share - …………… Ans : Old Share, 9) What are the different ways in which a partner can retire from the firm., Ans : a) Due to old age. B) Insolvent, 10) Distinguish between sacrificing ratio and gaining ratio., Sacrificing Ratio, Gaining Ratio, 1. It is calculated at the time of 1) It is calculated at the time of, admission of partner, retirement of a partner, 11) Why a retiring / deceased partner is entitled to share of goodwill of the firm., Ans : Because he is also contributed for the development and reputation of the, firm., 12) Who is an Executor ?, Ans : Executors is a legal representative of a deceased partner. He is entitled to, receive claims of deceased partner., , SECTION – B DEATH OF PARTNER, I) Fill in the blanks., 1) Executors account is generally prepared at the time of ……………. of a partner., Ans : Death, 2) Accounting treatment at the time of retirement and death is ……………., Ans : Uniform, 3) The period from date of the last Balance sheet and the date of the Partner’s death is, called ……………. Period. Ans : Intervening, 4) ……………. Account is debited for the transfer of share of accrued profit of a, deceased partner. Ans : P & L suspense, 5) Accrued profit is calculated on the basis of …………………, Ans : Previous years profit / Average profit / Sales, 6) Amount payable to the executors of the deceased partner is transferred to ………, account. Ans : Executors Loan, II) Multiple choice Questions :, 1) Accrued profit is ascertained on the following ways., a) Average Profit, b) On Sales c) Pervious years profits, d) All of the above, Ans : d) All of the above, 2) Amount due to deceased partner is settled in the following manner :, a) Immediate full payment, b) Transferred to loan Account, c) Partly paid in cash and the balance transferred to loan A/c., d) All of the above, Ans : d) All of the above, 3) Deceased Partner’s share of profit in the accrued profit may be calculated on the, basis of., a) Last year profit, b) Average profit of past few years, 26

Page 27 :

4), , 5), , c) Sales, d) All of the above, Ans : d) All of the above, Amount payable to the executors of the deceased partner is transferred to., a) Executors loan Account, b) Executors Account, c) Remaining Partners capital A/cs, d) None of the above, Ans : a) Executors loan Account, Items to be considered while calculating the amount payable to the deceased partner, is., a) His share of capital, b) His share in accrued profit, c) His share in reserve, d) All the above, Ans : d) All the above, , III) True or False, 1) Deceased Partner’s claim is transferred to his Executors Account. Ans : True, 2) Deceased Partners share of profit for the year intervening period may be calculated, on the basis of last year profit / average profits of past few years or on the basis of, sales., Ans : True, 3) Deceased partner may be paid in one lump sum or installments with interest., Ans : True, 4) Retirement normally takes place at the end of an accounting period, where as death, of a partner may occur any time. Ans : True, 5) Amount payable to be the executors of the deceased partner is transferred to, executors loan account. Ans : True, IV) Very Short Answer Questions., 1) Who is an ‘Executor’ ?, Ans : Executor is the legal representative of a decased partner in a partnership, firm., 2) When do you prepare Executor’s A/c?, Ans : Executor’s A/c is prepared at the time of death of a partner., 3) Which account is credited for the share of accrued profit of a deceased partner ?, Ans : Deceased Partner’s capital / Executor’s A/c, 4) What is intervening period ?, Ans : The period from date of last balance sheet to date of death of a partner is, called intervening period., 5) How do you close the executors Account ?, Ans : Executors A/c is closed by transferring its balance to Executors Loan A/c., , 27

Page 28 :

CHAPTER – 05, DISSOLUTION OF PARTNERSHIP FIRM, Sec-A, (01 Marks), -, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), -, , Sec-D, (12 Marks), 01, , TWO MARKS QUESTIONS, 1), , 2), , 3), , 4), , 5), , 6), , What is Dissolution of Partnership?, Ans : Dissolution of Partnership means changes in the existing relationship, between Partners but the firm may continue its business as before., Give the meaning of Dissolution of a Partnership Firm., Ans : Dissolution of Partnership between all the Partners of a firm is called, Dissolution of a Partnership firm., State any two circumstances under which a Partnership firm dissolved., Ans : a) With the consent of all the Partners, b) In accordance with a contract between the Partners., State any two differences between Dissolution of Partnership and Dissolution of, Partnership firm., Ans :, Sl., Basis, Dissolution of, Dissolution of, No., Partnership, Partnership firm, 1), Termination of, The business is, The business of the firm, business, terminated, is closed, 2), Settlement of, Assets and liabilities are Assets are sold and, assets and, revalued and new, liabilities are paid off., liabilities, balance sheet is drawn, 3), Other Dissolution It may or may not, It necessarily involves, involve dissolution of, dissolution of, the firm, Partnership, What is Realisation Account ?, Ans : Realisation account is an account which is prepared at the time of, dissolution of a Partnership firm to ascertain the profit or loss on realisation of, assets and payment of liabilities., Why is Realisation Account prepared ?, Ans : The Realisation account is prepared to find out the profit or loss on, realization of assets and settlement of liabilities., , 28

Page 29 :

7), , 8), , 9), 10), , 11), , 12), , 13), , 14), , 15), , 16), , 17), , What is the accounting treatment for unrecorded Asset Realised on dissolution of a, firm ?, Ans : Unrecorded asset realised is debited to cash (bank) Account and credited, to realisation account., What is accounting treatment for unrecorded liability paid on dissolution of a firm ?, Ans : Unrecorded liability paid is debited to realization account and credited, to cash (bank) account., How do you treat PBD on dissolution of a firm ?, Ans : P.B.D. is closed by transferring it to credit side of realisation account., Give the Journal entry for an asset taken over by a partner on Dissolution of a firm., (March & June 2019), Ans : Partner’s Capital A/c ……………. Dr, xxx ……, To Realisation A/c, …, xxx, (Being Assets taken over by partner), Give the journal entry for a liability taken over by a partner on dissolution of a firm., Ans : Realisation A/c ……………, Dr, xxx …., To Partner’s Capital A/c, ….. xxx, (Being liability taken over by partner), Give the Journal entry for transferring an asset to Realisation Account., Ans : Realisation A/c, Dr, xxx …, To Asset A/c, ….. xxx, (Being transfer of asset), Write the Journal entry for the transfer of an outside liability to Realisation Account., Ans : Liability A/c …………, Dr., xxx …., To Realisation A/c, ….. xxx, (Being transfer of liability), Give the Journal entry for the payment of Partner’s loan on Dissolution of a firm., Ans : Partner’s Loan a/c., Dr, xxx …., To Cash / Bank A/c, …, xxx, (Being Partner’s loan paid), Give the Journal entry for sale of an asset on Dissolution of a firm., Ans : Cash / Bank A/c ………… Dr, xxx ……, To Realisation A/c, ….. xxx, (Being Sale of asset), Give the Journal entry for payment of a liability on Dissolution of a firm., Ans : Realisation A/c, Dr, xxx …., To Cash / Bank A/c, ….. xxx, (Being payment of liability), Give the journal entry for the transfer of profit on realization., Ans : Realisation A/c ……., Dr, xxx …., To Partners Capital A/c, ….. xxx, (Being Profit transferred), 29

Page 30 :

18) Give the Journal entry for the transfer of loss on realization., Ans : Partner’s capital A/c, To Realiation A/c, , Dr, , xxx, …., , ….., xxx, , (Being transfer for loss), 19) Give the journal entry for realization expenses paid by the firm., Ans : Realisation A/c. ………. Dr, xxx …., To Cash / Bank A/c, ….. xxx, (Being realization expenses paid), 20) How do you close realization A/c on dissolution of a firm ?, Ans : Realisation account is closed by transferring its balance to partner, capital accounts., 21) Give the journal entry for realization expenses paid by the partner on behalf of the, firm., Ans : Realisation A/c, ….. Dr, xxx, To Partner’s capital A/c, …., (Being realization expenses paid by partner), , 30, , …., xxx

Page 31 :

BOOK-2, UNIT – 1, ACCOUNTING FOR SHARE CAPITAL, Sec-A, (01 Marks), 01, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), -, , Sec-D, (12 Marks), 01, , SECTION – A ONE MARK QUESTIONS, I) Fill in the blanks., 1) A company is an …………….. person. Ans : Artificial, 2) …………….. is the part of the issued capital. Ans : Subscribed capital, 3) Call money received in advance is called. Ans : Calls in advance, 4) …………….. is the minimum paid up capital of a public company, Ans : 5 Lakhs Rupees, 5) ……….. months must elapse between two calls. Ans : One, 6) …….. is minimum number of members in a public company. Ans : 7, 7) …………….. is minimum number of members in a private company. Ans : 2, 8) The amount of buy back of shares in any financial year should not exceed, …………….. % of the paid up capital. Ans : 25%, 9) Minimum paid up capital of a private company is ………….. Ans : 1 Lakh Rupees, 10) Profit on forfeiture of shares is transferred to ………… Account, Ans : Capital Reserve, II) Multiple choice Questions., 1) Equity shareholders are, (June 2019), a) Creditors, b) Owners, c) Customers of the company, d) None of the above, Ans : b) Owners, 2) Interest on calls in arrears is charged according to table F at the rate of, a) 10%, b) 6%, c) 8%, d) 11%, Ans : a) 10%, 3) Shares can be forfeited for :, a) Non-payment of calls money, b) Failure to attend meeting, c) Failure to repay the loan to the bank d) The pledging of shares as a security, Ans : a) Non-payment of calls money, 4) Balance of share Forfeiture Account is shown in the Balance sheet under the head., a) Current liabilities and provisions, b) Reserve and surplus, c) Share capital, d) Unsecured loans, Ans : c) Share capital, 31

Page 32 :

5), , Issued capital is part of, a) Reserve Capital, b) Unissued Capital, c) Authorised Capital, d) None of the above, Ans : c) Authorised Capital, 6) Maximum number of members in a private company is, a) 40, b) 200, c) 70, d) No limits, Ans : b) 200, 7) More applications are received than offered to public is called., a) Less offers, b) Under subscription, c) Over subscription, d) More offers, Ans : c) Over Subscription, 8) Paid up Capital is part of, a) Authorised capital, b) Reserve capital, c) Called up capital, d) Subscribed capital, Ans : c) Called up capital, 9) If a shareholder fails to pay call money, it is called as,, a) calls unpaid, b) calls in advance, c) calls in arrears, d) None of the above, Ans : c) Calls in arrears, 10) Minimum number of members in a public company is, a) 20, b) 50, c) No limit, d) 7, Ans : d) 7, III) True or False, 1) A company is an artificial person Ans : True, 2) Shares of a company are generally transferable Ans : True, 3) Share application account is a liability account Ans : True, 4) Paid up capital may exceed called up capital Ans : False, 5) Capital Reserves are created out of a capital profits. Ans : True, 6) The part of capital which is called up only on winding up is called reserved capital, Ans : True, 7) Private companies invite the public to subscribe for its shares Ans : False, 8) Forfeiture of shares is cancellation of the rights of shareholders. Ans : True, 9) All the shares of buy – back should be fully paid – up. Ans : True, 10) The Articles of the Association must authorize the company for the buy-back of, shares. Ans : True, IV) Very short answer Questions., 1) State any one kind of a company. Ans : Companies limited by shares, 2) What is issued capital ?, Ans : It is a part of Authorised capital which is actually issued to the public for, subscription., 32

Page 33 :

What is buy – back of shares ?, (March 2019), Ans : Purchase of its own shares by a company, 4) What is minimum paid up capital of a private company ? Ans : 1 lakh Rupees, 5) When the Reserved capital is used ?, Ans : In the event of winding up of the company, 6) What is over subscription ?, Ans : When the public apply for more shares than those offered to them, there, is said to be over subscription., 7) What is under subscription ?, Ans : When the number of shares applied for is less than the number of shares, for which applications have been invited for subscription, there is said to be, under subscription., 8) What is issue of shares at far ?, Ans :It means issue of shares at a price equal to face value of share of, company., 9) What is issue of shares at premium ?, Ans: It means the issue of shares at a price higher than the face value of, shares., 10) When the shares are forfeited ?, Ans : For Nonpayment of allotment and / call money due on shares., 3), , SECTION - B, V) Short answer Questions for Two marks, 1) What is a company ?, Ans : A company incorporated or registered under the companies Act 2013 or, under any other earlier Companies Act., 2) State any two features of a company ?, (June 2019), Ans :a) Body coporate, b) Separate legal entity, 3) What is prospectus ?, Ans : An open invitation to the public to take up the shares of company., 4) What do you mean by over subscription ?, Ans : When the public apply for more shares than those offered to them there, is said to be over subscription., 5) What is calls in arrears ?, Ans : The amount remaining unpaid on allotment or on call is called calls in, arrears., 6) Sate any two methods of issue of shares ?, Ans : a) Issue of shares at par, b) Issue of shares at a premium, , 33

Page 34 :

7), , 8), , What is issue of shares for consideration other than cash ?, Ans : Issuing of shares for purchasing of assets without receiving money in, cash., What is forfeiture of shares ?, (March 2019), , 9), , Ans : Cancellation of the right of a shareholder on shares held by him due to, non-payment of money due on such shares., Give the Journal entry for transfer of profit on re-issue of forfeited shares., Ans : Share Forfeiture A/c. …………. Dr., , To Capital Reserve A/c, (Profit on reissue of forfeited shares), 10) State any two categories of share capital, , xxx, , …., , …., , xxx, , Ans : a) Authorised capital, b) Issued capital, 11) What is public company ?, Ans : A company which is not a private company or not a subsidiary of a, private company., , 34

Page 35 :

UNIT – 2, ISSUE AND REDEMPTION OF DEBENTURES, Sec-A, (01 Mark), 01, , Sec-B, (02 Marks), -, , Sec-C, (06 Marks), 01, , Sec-D, (12 Marks), 01, , SECTION –A ONE MARK QUESTIONS, I) Fill in the blanks., 1) Debentureholders are the …………….. of the company. Ans : Creditors, 2) Debentures issued as collateral security will be debited to …………. A/c, Ans : Debenture Suspense A/c, 3) Discount on issue of Debenture is a …………. Asset. Ans : Fictitious, 4) Coupon rate is …………… at which the amount is paid by the company on its, debentures. Ans : Rate of interest, 5) Premium on issue of debentures is a …………….. Ans : Capital profit, 6) When all the debentures are redeemed, Debenture Redemption Reserve A/c is, Credited to ……………. A/c. Ans : General reserve, 7) NBFC registered with the RBI create redemption reserve equivalent to at least, ………….. of the value of outstanding debentures issued through public issue., Ans : 25%, 8) Withdrawal from Debenture Redemption Reserve is permissible only after, ………… of Debentures have been redmeed. Ans : 10%, 9) In case of conversion of the debentures into shares, debenture holders A/c is debited, and …………… a/c credited. Ans : Share Capital, 10) If own debentures are purchased by the company for the ……….. purpose. Own, debentures will be shown as an asset in the Balance sheet. Ans : Investment, 11) Debentures which are transferable by mere delivery are called ……… debentures., Ans : Bearer, 12) Debentures A/c is shown under the head ………… in the Balance sheet., Ans : Non-current liabilities / Long – term Borrowings, 13) 1000, 10% debentures issued at par, 10% means ………….. Ans : Rate of Interest, 14) The balance of Sinking Fund, Investment A/c after realization of investments is, transferred to ……………. A/c. Ans : Sinking Fund, 15) When the debentures are redeemed out of profits, an equal amount is transferred to, ………… A/c. Ans : Debenture Redemption Reserve (DRR), II) Multiple choice Questions., 1) Premium on Redemption of debentures A/c is ………….. A/c., a) Asset, b) Income, c) Liability, d) Expense, Ans : c) Liability, 35

Page 36 :

2), , 3), , 4), , 5), , 6), , 7), , 8), , 9), , Debenture premium cannot be used to, a) Write off the discount on issue of debentures or shares, b) Write off the premium on redemption of shares or debentures, c) Pay dividends, d) Write off the capital loss, Ans : c) Pay dividends, Loss on issue of debentures is treated as :, a) Intangible asset, b) Current asset, c) Current Liability, d) Miscellaneous expenses, Ans : d) Miscellaneous expenses, In the event of liquidation of the company the debenture holders have priority for, a) Interest, b) Principal amount, c) Both a & b, d) None of the above, Ans : c) Both a & b, Debentures cannot be redeemed at, (March 2019), a) Premium, b) Discount, c) Par, d) More than 10% premium, Ans : b) Discount, Debentures cannot be redeemed out of, a) Profits, b) Provisions, c) Capital, d) All the above, Ans : b) Provisions, A company issued 2000, 8% debentures of 100 each at par value redeemable at, 10% premium, 8% stands for, a) Rate of dividend, b) Rate of tax, c) Rate of Interest, d) Rate of TDS, Ans : Rate of Interest, Debentureholders are, a) Owners of the company, b) Lenders of the company, c) Debtors of the company, d) Trustees of the company, Ans : b) Lenders of the company, “X” company ltd, purchased machinery for Rs. 20000, payable Rs. 6500 in cash, and the balance by issue of 12% debentures of Rs. 100 each at a discount of 10%, How many debentures would be required to issue to the vendor ?, a) 155 Debentures of 100 Rs. each, b) 150 Debentures of 100 Rs. each, c) 135 Debentures of 100 Rs. each, d) 145 Debentures of 100 Rs. each, Ans : b) 150 Debentures of 100 Rs. each, , 36

Page 37 :

10) XYZ company ltd, issued 5000, 6% debentures of 100 each at par and redeemable, at 10% premium, Premium on redemption will be debited at the time of issue of, debentures to., a) Loss on issue of debentures A/c., b) Share discount A/c, c) Security premium A/c, d) General reserve A/c, Ans : a) Loss on issue of debentures A/c., 11) Methods of Redemption of debentures are, a) By annual drawings, b) By conversion of shares or new debentures, c) By purchasing own debentures in open market, d) All of the above, Ans : d) All of the above, 12) A company cannot redeem its debentures fully, a) Out of capital, b) Out of profits, c) Both a & b above, d) None of the above, Ans : a) Out of Capital, 13) If the market price of the debentures is more than the face value, at the time of, redemption this will be a capital loss and is transferred to …………, a) Capital Reserve, b) General Reserve, c) Profit on Redemption of debentures, d) Loss on Redemption of debentures, Ans : d) Loss on Redemption of Debentures, 14) The following journal entry appears in the books of company., Bank A/c, ……Dr, 9,50,000, xxx, Loss on Issue of Debenture A/c, …….Dr, 1,50,000, xxx, To 8% debentures A/c, xxx, 10,00,000, To Premium on Redemption on debenture A/c, xxx, 1,00,000, In this case debentures are issued at discount of …………, a) 15%, b) 5%, c) 10%, d) 8%, Ans : b) 5%, 15) Raj company ltd, purchased assets worth Rs. 14,40,000. It issued debentures of Rs., 100 each at a discount of 4% in full settlement of the purchase consideration. The, number of debentures issued to vendors is :, a) 15000, b) 14400, c) 16000, d) 15600, Ans : a) 15000, III) True or False Type Questions :, 1) Debenture is a part of loaned capital. Ans : True, 2) Debentureholders have voting rights. Ans : False, 3) Debentures bear fixed interest. Ans : True, 4) Debentures cannot be issued for consideration other than cash. Ans : False, 5) Company can buy – back its debentures. Ans : True, 6) Interest on debentures is not shown in P & L Statement. Ans : False, 37

Page 38 :

7), 8), 9), 10), 11), 12), 13), 14), 15), , Debentureholders are not the members of the company. Ans : True, Premium on redemption of debentures is a liability A/c. Ans : True, Debenture cannot be issued as a collateral security. Ans : False, A company can issue irredeemable debentures. Ans : True, Redemption of debentures is made by the company in accordance with the terms of, issue. Ans : True, A company cannot purchase its own debentures in the open market. Ans : False, Profit on redemption of debentures is in the nature of a capital profit. Ans : True, Debentures cannot be issued at discount for more than 10% of the face value, Ans : False, Loss on issue of debentures is a revenue loss. Ans : False, , IV) Very short answer Questions :, 1) What is meant by debentures ?, Ans : Debentures are the written instruments acknowledging debt under the, common seal of the company., 2) What is Bond ? Ans : Bond is an instrument of acknowledgement of debt., 3) What is coupon rate ?, Ans : Coupon rate refers to a specified rate of interest on debentures., 4) What do you mean by zero coupon rate debentures ?, Ans : Zero coupon rate debentures refer to the debentures those do not carry a, specific rate of interest., 5) What is meant by issue of debentures for consideration other than cash ?, Ans : Issue of debentures for consideration other than cash means issuing, debentures to vendors for purchasing of assets., 6) What do you mean by the issue of debentures as a collateral security ?, Ans : Issue debentures as a collateral security mean issuing debentures to the, lenders in addition to some other assets already pledged., 7) Name of any one method of redemption of debentures., Ans : Payment in Lump sum, 8) What do you mean by redemption of debentures ?, Ans : Redemption of debentures refers to repayment of the amount of, debentures by the company., 9) Expand D R R, (June 2019) Ans : Debenture Redemption Reserve, 10) Expand D R F I Ans : Debenture Redemption Fund Investment, 11) Expand AIFIs Ans : All India Financial Institutions, 12) State any one type / kind of debentures. Ans : Secured Debentures., 13) Can the company purchase its own debentures ? Ans : Yes, 14) Debenture Redemption Reserve is shown under which head in the balance sheet ?, Ans : Reserve & Surplus, 15) Name the head under which discount on issue of debentures appears in the balance, sheet of a company ?, Ans : Other Non-current Assets, 38

Page 39 :

UNIT – 3, FINANCIAL STATEMENTS OF A COMPANY, Sec-A, (01 Marks), 01, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), 01, , Sec-D, (12 Marks), -, , SECTION – A : ONE MARK QUESTIONS, I) Fill in the blanks., 1) …………….. statements are the basic and formal annual report. Ans : Financial, 2) Financial statements include …………….. and Balance sheet., Ans : Statement of Profit and Loss, 3) Income statement and …………….. are the financial statements., Ans : Position Statement (Balance Sheet), 4) The object of preparation of balance sheet is to ascertain the …………….., Ans : Financial position of the Enterprise, 5) Income Statement is prepared to ascertain …… .Ans : Surplus of the Enterprise, 6) Share Capital appears under the head …………….. Ans : Shareholders Fund, 7) Capital reserve is shown under …………….. head in the balance sheet of the, company Ans : Reserves and Surplus, (June 2019), 8) Debit balance of statement of profit and loss shall be shown as …………….. figure, under surplus head. Ans : Negative, 9) Loans which are repayable within …………….. months are called as short term, borrowings. Ans : 12, 10) Fixed assets are classified as tangible and …………….. assets Ans : Intangible, II) Multiple choice Questions :, 1) Financial statements generally include, (March 2019), a) Comparative statement, b) Fund Flow Statement, c) Income Statement and Balance sheet d) None of the above, Ans : c) Income Statement and Balance sheet, 2) The prescribed form of Balance sheet of the companies has been given in the, schedule., a) VI part I, b) VI part II, c) VI part IV, d) III Schedule, Ans : d) III Schedule, 3) Which of the following is shown under the head “fixed assets”, a) Goodwill, b) Patents, c) Trademarks, d) All of the above, Ans : d) All of the above, 4) Current Assets does not include, a) Short Term Investments, b) Buildings, c) Inventories, d) Cash and Cash Equivalents, Ans : b) Buildings, 39

Page 40 :

5), , Current liabilities are to be paid within……………… months, a) 3 months, , 6), , 7), , 8), , b) 6 months, , c) 9 months, , Ans : d) 12 months, External users of financial statements does not include., a) Banks, b) Shareholders, c) Creditors, d) Government, Ans : b) Shareholders, Share Capital is shown as ……………., a) Authorised Capital, , b) Issued Capital, , c) Subscribed Capital, , d) All the above, , Ans : d) All the above, Financial statements are prepared based on., a) Accounting postulate, b) Accounting conventions, c) Recorded Facts, , 9), , d) 12 months, , d) All the above, , Ans : d) All the above, Non-Current assets are :, a) Expected to use in the business for long period., b) Involved in entities operating cycle, c) Primarily held of trading, d) Cash and Cash Equivalents, Ans : a) Expected to use in the business for long period., , III) True or False type Questions., 1) The original cost is the basis of recording transactions. Ans : True, 2) Going concern postulate assumes that the enterprise exists for a longer period of, time. Ans : True, 3) The financial statements do not show current financial condition of a business., 4), 5), 6), 7), 8), 9), , Ans : False, The stationery is valued at cost. Ans : True, Provisions are maintained for known liabilities. Ans : True, While preparing financial statements, inventories valued at market price or cost, price whichever is less. Ans : True, Cash and cash equivalents are to be disclosed in accordance to IAS – 3. Ans : True, Rounding off of figures in financial statements is not mandatory. Ans : False, In the Balance sheet of a company goodwill is shown under the heading of “Fixed, Assets”. Ans : True, , 10) Proposed dividend is shown under the head Provisions. Ans : True, , 40

Page 41 :

IV) Very short Answer Questions :, 1) Name any one type of financial statements. Ans : Balance sheet, 2) State any one feature of financial statements. Ans : Recorded Facts, 3), 4), , Name any one internal user of financial statements. Ans : Shareholders, Write any one objective of financial statements, , 5), , Ans : To provide information about profitability and financial position, State any one type of reserve. Ans : Capital Reserve, , 6), , Give an example for non-current asset. Ans : Building, , 7), , Where do you record the money received against share warrants ?, , 8), , Ans : Shareholder’s Fund, How do you treat credit balance of Income statement under the head surplus ?, , Ans : It is shown in surplus under ‘Reserves and Surplus head, 9) Write any one feature of current assets. Ans : Involved in entity’s operating cycle, 10) How do you treat preliminary expenses ?, Ans : Preliminary expenses are to be written off completely in the year in, which, such expenses are incurred first from securities premium reserve, next, from surplus., SECTION - B, V) Two marks Questions :, 1) Give the meaning of financial statements., , (March 2019), , Ans : Financial statements are the basic and formal annual reports through, , 2), , which the corporate management communicates financial information to its, owners and various other external parties, Mention two types of financial statement, , 3), , Ans : a) Statement of profit and loss, b) Balance Sheet, State any two features of financial statements., , 4), , Ans : a) Recorded Facts, b) Accounting conventions followed, Write any two objectives of financial statements., , 5), , Ans : a) To provide information about earning capacity of the business., b) To provide information about economic resources., State any two benefits of financial statements., Ans : a) Basis for prospective investors, b) Report on the performance of the management, , 41

Page 42 :

6), , Give any two limitations of financial statements., , 7), , Ans : a) Do not reflect current situations, b) Assets may not realized at stated values, State any two postulates, , (June 2019), , Ans : a) Money measurement postulate, 8), , b) Realisation postulate, How will you disclose the following items in the Balance sheet of a comp1any ?, a) Loose tools, , 9), , b) Proposed dividends, , Ans : A) Loose Tools : Inventories (Current Assets), B) Proposed Dividends : Short Term Provisions (Current Liabilities), State any two differences between Current Liabilities and Non-current liabilities., Ans :, Current liabilities, , Non Current liabilities, , a) Expected to be settled within 12, months, , a) Expected to be settled after 12, months, , b) Held primarily for the purpose of, , b) Held as source for long term, , being traded, , finance, , 10) Mention any two items which are shown under the head “Reserves and Surplus”, Ans : a) Capital Reserve, , b) Securities Premium Reserve, , 42

Page 43 :

UNIT – 4, FINANCIAL STATEMENT ANLYSIS, Sec-A, (01 Marks), 01, , Sec-B, (02 Marks), 01, , Sec-C, (06 Marks), -, , Sec-D, (12 Marks), 01, , SECTION A : ONE MARK QUESTIONS, I) Fill in the blanks., 1) The term analysis means simplification of …………….. Ans : Financial data, 2) Interpretation means explaining the …………….. and a significance of the data, Ans : meaning, 3) Comparative analysis is also known as …………….. analysis. Ans : Horizontal, 4) Common size analysis is also known as …………….. analysis. Ans : Vertical, 5) Common size statement is also known as …………….., Ans : Component percentage statement, 6) The term financial analysis includes both analysis and …………….., Ans : Interpretation, 7) Analysis is useless without …………….. Ans : Interpretation, 8) Interpretation without analysis is …………….. Ans : Difficult, 9) The statement showing the profitability and financial position for different periods, of time in a comparative form is known as …………….., Ans : Comparative Statement, 10) The statement which indicates the relationship of different items of financial, statement with a common item is called …………….., Ans : Common Size Statement, 11) It is possible to assess the profitability, solvency and efficiency through the, technique of …………….. Analysis. Ans : Ratio, 12) Analysis of actual movement of cash into and out of an organization is called, …………….. Ans : Cash flow Analysis, 13) Inter-firm comparison or comparison of the company’s position with the related, industry as whole is possible with the help of …………….., Ans : Common size statement analysis, 14) Percentage of each asset to the total assets is show in …………… Balance sheet., Ans : Common Size, 15) Analysis and interpretation are …………… to each other Ans : Complimentary, II) Multiple choice Questions., 1) The financial statements of a business enterprise include :, a) Balance sheet, b) Statement of profit and loss, c) Cash flow statement, d) All the above, Ans : d) All the above, 43

Page 44 :

2), , The most commonly used tools for financial analysis are, a) Horizontal Analysis, b) Vertical Analysis, c) Ratio Analysis, d) All the above, Ans : d) All the above, 3) An annual report is issued by a company to its, a) Directors, b) Auditors, c) Shareholders, d) None of the above, Ans : c) Shareholders, 4) Comparative statements are also known as, a) Dynamic Analysis, b) Horizontal Analysis, c) Vertical Analysis, d) External Analysis, Ans : b) Horizontal Analysis, 5) Common size statements are also known as, a) Dynamic Analysis, b) Vertical Analysis, c) Horizontal Analysis, d) External Analysis, Ans : Vertical Analysis, 6) Percentage of each liability to the total liabilities is shown in, a) Common size Balance Sheet b) Comparative Balance sheet, c) Both the above, d) None of the above, Ans : a) Common size Balance Sheet, 7) Balance sheet provides information about financial position of the enterprise., a) At a point of time, b) Over a period time, c) For a period of time, d) None of the above, Ans : c) For a period of time, 8) Comparative statement shows the changes during the year., a) In absolute terms, b) In relative terms, c) Both the above, d) None of the above, Ans : a) In absolute terms, 9) Common size statements are useful in comparison of, a) Intra firm for the same or several years, b) Inter firm over different years, c) Both (a) & (b) above, d) None of the above, Ans : c) Both (a) & (b) above, 10) Financial analysis can be undertaken by, a) Management, b) Parties outside the firm, c) Both the above, d) None of the above, Ans : c) Both the above, III) True or False type Questions :, 1) The financial statements of business enterprise include cash flow statement, Ans : False, 44

Page 45 :

2), 3), 4), 5), 6), 7), 8), 9), 10), 11), 12), 13), , Comparative statements are the form of Horizontal Analysis. Ans : True, Common size statements and Financial Ratios are the two tools employed in, Vertical Analysis. Ans : True, Financial Analysis is used only by the creditors. Ans : False, (March 2019)., Financial Analysis helps an analyst to arrive at a decision. Ans : True, In a common size statement, each item is expressed as a percentage of same, common base. Ans : True, The difference between the inflow and outflow of cash is the net cash flow., Ans : True, The flow of cash into the business is called positive cash flow of financial, statement. Ans : True, Financial Analysis can be undertaken by management or by parties outside firm., Ans : True, Financial data will be comparative only when same accounting principles are used., Ans : True, Non-monetary aspects are ignored in financial analysis. Ans : True, Financial Analysis does not consider price level changes. Ans : True, Items of expenditure are shows as a percentage of the net revenue from operations, in common size income statements. Ans : True, , IV) Very short answer type Questions :, 1) What do you mean by Financial Statements Analysis ?, Ans Financial Statement Analysis means simplification of financial data by, methodical classification given in financial statement., 2) State any one object of financial statement analysis., (June 2019), Ans : To identify the reasons for change in the profitability / financial position, of the firm., 3) State any one technique of Financial Statement Analysis., Ans : Comparative Statement, 4) State any one user of Financial Analysis. Ans : Investors, 5) What is Vertical Analysis ?, Ans : It is a tool of financial analysis, in which data or figures are converted, into percentages of a common base item., 6) What is Horizontal Analysis ?, Ans : It is a technique of financial Analysis, in which data / figures are shown, in a comparative form of two / more years., 7) State any one importance of Financial Analysis. Ans : Helpful to finance manager, 8) State any one limitation of Financial Analysis., Ans : It does not consider price level changes, 9) Give the meaning of analysis., Ans : Analysis means simplification of financial data by methodical, classification., 45

Page 46 :

10) Give the meaning of Interpretation, Ans : Interpretation means explaining the meaning and significance of data., , SECTION B : TWO MARK QUESTIONS, 1), , 2), , 3), , 4), , 5), , 6), , 7), , 8), , 9), , What do you mean Financial Statement Analysis ?, Ans : The process of critical evaluation of the financial information contained, in the financial statements in order to understand and make decisions, regarding the operations of the firm is called Financial Statement Analysis., Give the meaning of Analysis and Interpretation of Financial statements., Ans : Analysis and Interpretation of financial statements means implication of, data and explaining the meaning and significance of data., List any two techniques of Financial Statement Analysis. (March/June 2019), Ans : 1) Comparative statements, 2) Common size statements, Distinguish between Vertical Analysis and Horizontal Analysis of finance data., Vertical Analysis, Horizontal Analysis, 1) Figures are converted in to % of 1) Figures are shown in comparative, common base item., form., 2) Figures of same year are 2) Figures of two years are compared, converted in to %, What are comparative financial statements ?, Ans : These are the statements showing the profitability and financial position, of a firm for different periods of time in a comparative form to give an idea, about the position of two or more periods., What do you mean by common size statements?, Ans : These are the statements which indicate the relationship of different, items of a financial statements with a common item by expressing each item as, a percentage of that common item., State any two importances of financial statements analysis., Ans : 1) Helpful to financial manager, 2) Helpful to investors, State any two objectives of Financial statement analysis., Ans : 1) To ascertain the relative importance of different components of the, financial position of the firm., 2) To identify the reasons for change in the profitability / financial position of, the firm., State any two users of financial statement analysis., Ans : a) Finance manager, b) Top management, , 46

Page 47 :